Most of the stock investors on this forum never think about investing in bonds. Investigating companies and looking for next 100 bagger is much more exciting than parking your money in a bond fund and watch it crawl like a snail. But does this efforts good for your wallet? The data does not think so.

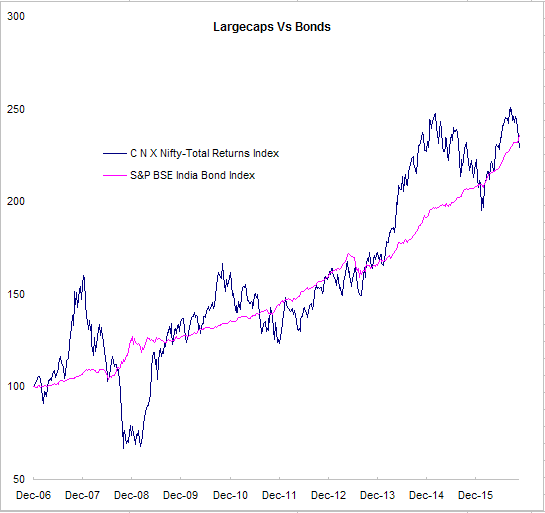

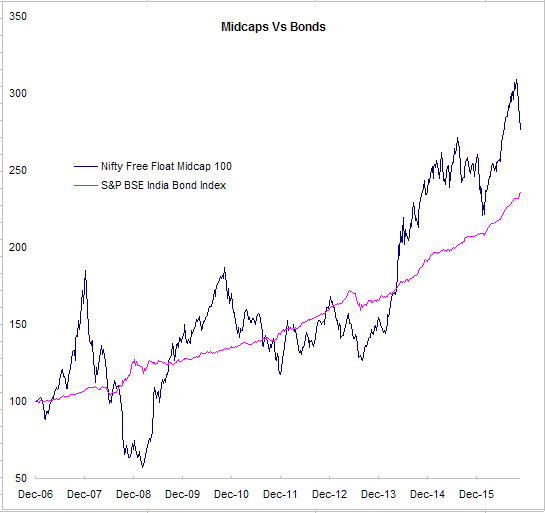

Here is a chart I prepared using the 10 year returns on Nifty 50 and S&P BSE India Bond Index as proxies for stocks and bonds respectively.

Both indices are total return indices. i.e. Nifty index includes dividends & bond index includes coupon payments. Both are a good proxy of what a passive investor would receive. As the chart above shows, over last 10 years, stocks have returned as much as bonds (actually little bit less after recent sell-off) with plenty of volatility. Risk adjusted returns on stocks would be much lower. Unless you re someone who can benefit from volatility or beat the indices by a wide margin, investing in stocks hasn’t been rewarding even when average GDP growth during this period was more than 6% per year.

How can we invest in Bond Index in Indian Market…Yogesh please suggest good Bond ETF or other instruments through which retail investors can invest in Bonds

Hi

I was investing in Dynamic Bond fund in past 2years. Which gave good return (on avg 12%) past 2 years. Using Dynamic Bond fund , fund house has flexiblity to move between short term/long term tenure bonds, depends on the fund manager view on how bond yield will pan out in near future.

Investors also had a good opportunity to invest in tax free bonds in March 2016 when two companies (NABARD and HUDCO) issued bonds with maximum coupon rate of 7.69% - this translates into a return of 10%+ if the same had been an FD.

The capital gain on these bonds has also been quite excellent - the bonds were issued at 1000 and are noe trading around 1180 and 1200 , that’s a return of 18% and 20% respectively in around 9 months. Sure, the capital gain will fall once the interest is paid out, but will still be around 10-11% + 7.7% interest.

If I remember correctly (I am sure, since I invested a lot into these bonds), the subscription for the retail portion was quite subdued, maybe 1.3/1.5% times. The long tenure of the bonds maybe put retailers off, or maybe enough people did not know about it. I find the latter hard to believe since the advertisements were splashed all across the newspapers for many days.

These are the kind of investments that just require very basic knowledge of bond prices vs interest rate movements. Our interest rates since the days of RRR have been intrinsically linked to inflation and our inflation target is around 4%. With such easily available information, it is a no brainer that a 7.7% tax free bond with a tenure of 20 years plus will make excellent capital gains at least in the next 5 years.

I can say all this since I picked up a big chunk of these bonds (almost as big as my equity portfolio at the time). Maybe hindsight is 20/20 but I am not complaining.

Sorry for Naive questions. Dont have much experience with bond markets.

How do we know when bonds are being issued?

How to we buy bonds? Through existing trading platform or any other means?

Can I see currently list of all bonds which I can buy?

Looks like there is some confusion over the term bonds.

Bonds is a generic term for all securities that pay a fixed rate of return. The term bonds means all debt mutual funds, listed and unlisted debentures (NCDs), bank fixed deposits, company fixed deposits, govt treasury bonds, etc or any other security that pays a defined interest rate paid at regular intervals and has a maturity date and maturity value.

You can buy bonds by buying them directly from issuers (bank FDs, Company FDs) or from a distributor or buy it on an exchange (there are NCDs that trade on NSE and BSE just like stocks) through your broker or you can also buy debt mutual funds.

Large issues are advertised just like IPOs so you can buy them just like IPOs but easiest way to buy bonds is to buy debt mutual funds.

There is only one ETF that I know and that is LIQUIDBEE. This ETF invests in overnight call money instruments and returns on this instrument is close to call money rates typically 4-5% each year post tax. I think there is one other ETF but with very little liquidity last time I checked.

Best way to invest in bonds is to buy debt mutual funds. The index I used in my charts is a broad bond index. Debt mutual funds have their own benchmark index and they will generally try to match the performance of the index after fees. A debt mutual fund with low expense ratio purchased directly from mutual fund house will give you return closest to the benchmark.

Since interest rates are dropping in India, debt mutual funds will have tough time beating their benchmark unless they they cut their fees also proportionately.

Nice topic, Yogesh. Adding my two cents here, we also need to consider whether to invest in listed company equity shares, or in their listed unsecured NCDs(non convertible debuntures). In both cases, capital is at risk and the question is whether to assume credit risk for relatively low compensation.

I am studying this subject and hope to add to this thread soon

I go by the following rules for fixed income investments -

Generate your out performance through equities, bonds/fixed income is to beat inflation and preserve capital. Never go into a bond investment with the mindset of generating alpha

When in doubt be conservative. The risk/reward is tremendously against you in fixed income space, you get an alpha of 1-1.5% if you do a great job but can lose your capital if you get things wrong especially on the credit side. On a bond portfolio of say 1 Cr, the alpha hardly makes a difference to your life

Credit is a 0 or 1 event, fixed income means your income is fixed; does not mean income is assured

Vol in longer dated bonds (say 10 Gr) is as high as what you see in stocks, especially since 2013. No newspaper will ever say this out loud, swings of 5 bps+ in YTM in a single session are common these days. Since Nov 9, the 10 yr G-Sec has moved by 30+ bps - this is not a minor move by any yardstick

Herding happens in bonds as well, institutional investors get it wrong quite often. It’s not just retail investors who are suckers for momentum and front running

Always look for signals across all three markets - equity, FX and bonds. When all three resonate with the same message, the market is usually about to either peak out or bottom out

Here on my incremental fixed income allocation will go towards the shorter end of the yield curve. I am not yet exiting my duration play but will start moving out in 2017

I have invested in 2014-NHB BONDS of facevalue 5000 each giving 9% taxfree. The bonds are quoting at 7000 today and I am getting my 9% tax free without any tension

Debt markets have surged because of the excess liquidity in the banking system and debt appears to be overvalued now. Yield curve is still sloping upwards so people are not expecting a recession or a slowdown yet.

The purpose of the thread is to highlight debt as an asset class that has beaten stock indexes hands down even without adjusting for volatility risks. On the other hand, the chart shows stocks were expensive in 2007 (in hindsight it is easy to say that) and bonds could be expensive now. Avid stock pickers will focus on alpha rather than beta returns on indexes but if stocks as an asset class does not do well, there is only so much alpha one can generate.

Do you use any analytical model like Markowitz Portfolio Theory to decide your asset allocation? If yes, how do you derive expected returns on asset classes as I think expected returns are the most important inputs to this model.

You are correct, it is my mistake. I would point out though, that post-issuance, the bonds were trading at very small premium for a few weeks - giving ample time for accumulation.

My generic rule has been to look at range of outcomes and see which outcome the market appears to be discounting the most. By that definition duration makes most sense when the yield curve is inverted or flattish. Most of my duration was built during 2014 which I’ve kept steady through the period. Current YTM’s on offer for a 2-3 tenure do not look very attractive to me, neither do credit spreads which seem to be below historical averages

Hence a combination of logical indicators is what I rely on, never considered myself a fixed income guru anyway. Will focus more on avoiding mistakes than on doing something fancy here.

To summarize I look at -

Yield curve - upward sloping/flat/inverted

Term Spreads

Credit Spreads

Near term momentum & range of outcomes from here

Bond yields are inversely proportional to bond prices. When prices rise yields fall and when prices drop yields rise. Prices of bonds (much like anything else) is a function of demand and supply.

Demand for bonds goes up for following reasons:

Liquidity - When RBI lowers rates, it pumps more money into banking system by buying bonds which lowers interest rates.

Risk Aversion - When investors become risk averse they switch form risky assets like stocks and real estate and buy relatively safe assets like treasuries.

Low Inflation or lower inflation expectation. - When investors expect inflation to drop in future, they generally bid bonds higher.

Economic Outlook - When investors expect economy to slow down they sell risky assets and buy bonds.

Supply of govt bonds goes up in following cases

Budget Deficit - Govt funds its deficit primarily though borrowing by issuing bonds.

Liquidity - When RBI raises policy rates, it does so by selling bonds from its balance sheet in order to suck liquidity from the financial system which leads to higher rates.

Risk Aversion (of lack thereof). When investor become less risk averse, they sell bonds and switch to risky assets like stocks.

High Inflation or high inflation expectation- Inflation causes bond holders to sell bonds and/or demand higher rates and bond prices fall in response.

Economic Outlook - When investors expect economic growth to pick up they buy risky assets and sell safer bonds.

RBI has effectively put an end to the duration trade for now. The 10 yr yield spiked up almost 25 bps today - translation investors holding longer dated papers would’ve seen 1.5-2.5% knocked off their NAV’s in a single session.

Here on credit play looks interesting to me given where the banking system is. Banks are flush with funds with no lending avenues clearly visible over the next 6 months. Top rated corporates (AAA) are in no need for funds, banks will eventually need to seek out the A and BBB companies if they are serious about correcting their ALM over the next 6-12 months. Which means borrowing should get easier for organized players who are seeing a demand uptick in their favor post demonetization.

I am gonna look at deploying my money that was in duration all these days into funds that have a good track record of managing credit. At a YTM of 9.5% and above pre expense ratio, divided yield per month will be 6-6.5%+ which I am happy to take for the time being.

Am also starting to get worried that the moment 1 year returns of fixed income funds start dropping below 8%, the advisor community will start increasing their allocation towards equity. Whenever the TINA approach is taken it has always resulted in herding. Fund managers have a problem on their hands too, they are already sitting on 25K+ Cr of cash and with SIP inflows topping 4K Cr every month, they will be forced to deploy into equity markets even if they aren’t fully convinced. May be time to get a little cautious and be choosy about what to buy

After investing in equity for long, and having exposure to safer (?) instruments like tax-free bonds and NCDs offered by Dewan and Edelweiss, sometime back I took exposure to Long term / Gsec funds. I was looking at low interest rate cycle and hence thought of taking a medium exposure to duration play with LT funds of HDFC and ICICI MF. Though I’m in +ve area still, volatility here is more than equity mkt, as you or Yogesh mentioned in one of the post. Since the funds will take a beating today after “no change” by RBI, I’m also thinking of shifting part of my investment to better avenues. It would be helpful for investor like me if you can explain little bit more on what exactly you meant in above para? Thanks.

While RBI surprised the market with the rate decision and change of stance, I don’t think the bull market in govt securities is over yet. Credit growth to the industry is negative for the first time in recorded history (at least the one I have seen). There is no demand for credit from the industry so banks have no option but to park all the surging deposits into govt bonds irrespective of the yields. That will keep the bull market in treasuries going for some more time until credit demand picks up again. Even if it picks up, banks are repairing their balance sheets on their own with no hopes of bailout from the budget. That means they have to restrict lending for years. This will cause the credit spreads to widen further limiting the demand for credit.

The link above shows that Credit to industry contracted by 4.3 per cent in December 2016. I went as far back as 1970 and non-food credit (majority of which goes to Industry) has grown in double digits. This will be the first year in history non-food credit will grow in single digit with more recent months credit to industry actually declining. Services and personal loans (mainly housing) is driving credit growth.

Here’s what the underlying portfolio of various categories look like now

Short Term Debt Funds - Mod duration in the range of 1.5 - 2.5 years and a YTM (yield to maturity) of 7.2% post expense ratio. Effectively if interest rates stay where they are, you are likely to make an annual return of between 7 - 7.8% here on before taxation.

Duration Funds - exposure to longer dated securities, Mod duration in the range of 5-8 years and a YTM of around 7%. If interest rates go down by 25 bps, you are likely to make YTM + (change in interest rate) * mod duration. These funds are most sensitive to interest changes (or expectations of interest rate changes), hence over the past 1 year these funds had the highest return. Some funds gave return in excess of 15%, however when the expectations of interest rate cuts reverse, these funds will see most drop in NAV

Credit funds - These invest in shorter term papers with a mod duration of 1 - 2.5 years but hold sub AAA papers predominantly. Hence the YTM is way higher and in the range of 8.7 - 10.5% currently depending on where the max exposure is, logically lower the credit quality higher will be the YTM.

Given that banks are sitting on a lot of money which they will eventually need to deploy into lending business, my call is that the sub AA category of corporates is where banks will need to lend. Larger corporates with healthy cash position won’t really borrow unless the rate is very attractive. For the banker to make a healthy ROE on his loans, he needs to look at a healthy spread over his cost of funds, this spread can come only if the corporate isn’t highly rated. Also post demonetization, organized players are gaining business at the expense of unorganized guys. If banks want to expand their asset base, they will need to look at sub AA rated corporates since they will be most hungry for working capital and term loans.

Also higher the YTM of the fund, lower is the interest rate sensitivity since a higher YTM cushions any mark to market losses due to adverse interest rate swings. I do not think interest rate hikes are materializing any time soon, I also think the current bond market reaction is overdone. However at a gross YTM of 10% I see better chances of making a healthy return in credit oriented funds than in duration funds. I will restrict the exposure to 30% of my fixed income portfolio though