Thanks @zygo23554 for your detailed answer and comments, very helpful.

I agree with your observations regarding liquidity in the system and banks flush with money. From debt investment point of view, and equity investment in banking stocks one major variable to track will be credit growth with NPA situation over next couple of quarters. Its a tricky situation for lenders, as well as investors!

Are you looking to invest in junk bonds or bond funds? Did you find any? Couple of high interest funds I looked at have the same past returns as the regular high duration funds so not sure if they actually have a high YTM or just call themselves so.

Bond funds with a high YTM of 9.5%+

Do look at the Templeton funds pack (short term, corporate bond opps funds), they are currently running a YTM of 10%+ pre expense ratio at a mod duration of less than 2 years, lot of play in the A category. Other options being the corporate bond funds from Reliance, ICICI and Kotak, these are at a YTM of approx 8.75 - 9% since they play into the AA category

Given that the repo is at 6.25%, anything in excess of 8.75% fits into high YTM in my book.

Disclaimer: I am not a SEBI registered advisor, please due your due diligence on the funds ![]()

1 Like

These are all high expense ratio and high exit load funds. I am not planning to keep them for that long and will mostly incur the exit loads. Their YTMs are near 52 week highs so clean price must have dropped recently. That’s something to worry about. High exit load indicate that these are illiquid securities indicating low demand.

Moreover, being an active investor, I can’t imagine buying a fund ![]() I am looking at NCDs that trade like a stock. Generally the ones with annual coupons and high maturity trade with some volume. Ones with monthly coupons have poor liquidity. Also large issues have higher liquidity.

I am looking at NCDs that trade like a stock. Generally the ones with annual coupons and high maturity trade with some volume. Ones with monthly coupons have poor liquidity. Also large issues have higher liquidity.

Here are a few I am looking at

These have relatively better liquidity but still not enough to build a large portfolio. Spread is also high.

2 Likes

An interesting perspective on the thread topic.

http://morningstar.in/posts/40627/do-stocks-really-outperform-debt.aspx

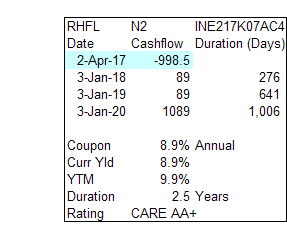

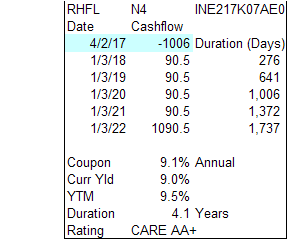

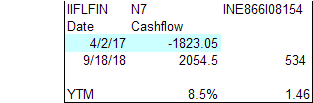

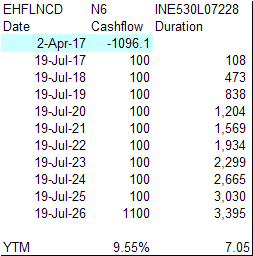

YTMs have improved for some, here are the latest numbers (NSE prices as of 30/06/17):

RHFL N2 (10.13%), N4 (9.82%)

IIFL N7 (9.46%)

EHFL N6 (9.08% - YTM reduced here ), another one with liquidity is N3 (9.68%)

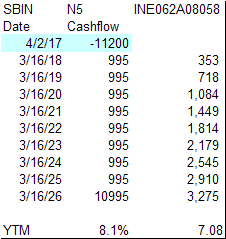

SBIN N5 (7.79% - YTM reduced here).

I was looking for few funds where we get some decent YTM and low duration, and following twins from Franklin look good: Ultra Short Bond Fund - Super IP and Low Duration. For both, issue is lower credit quality, but I reckon they should be able to manage it better due to shorter durations.

Two other safer bets (at lower YTM) are Invesco Med term bond and Principal credit opp.

Let me know your comments @zygo23554 and @Yogesh_s. Cheers!

Hi , I am looking for Junk Bonds.

Mostly of the companies which are in the bankruptcy list of the RBI.

Is anyone investing in Junk bonds here ? please help from where to go find more information about it.

Which ones are the most liquid and i would be great if you could share some ideas too

Dear All,

I also want to build a Portfolio of NCD’s/Debt instruments, currently, I am basically 50%, 50% invested in both Equity and Debt (Mostly Liquid funds), so for debt PF, I think liquid funds are not optimal since these are very short-term and a bit low yield.

Purpose: I want to build Fixed Income PF, so I have peace of mind and I can invest back income form debt PF back to equity on a regular interval, let’s say I want the monthly income of around 1lc from debt PF, what would you suggest the best way to go about it…?

In current scenario’s is 9% yield is achievable(without compromising on the safety of capital), appreciate if any of you guide on this and suggest some names to invest.

Currently, I see SREI EQUIPMENT FINANCE LTD NCD, which is giving 9.6% yield, but I think its a bit risky NCD, shall I consider distributing 5-10lc on each such NCD.

Thank you!

Best Regards,

Gagan

I liked edelweiss platform for initial screening of securities but not ventured into NCD investing as I was skeptical about liquidity and impact cost during exits. Let me know if you have invested and key aspects you need to be aware of

1 Like

Small financial banks are providing interest rates up to 9.25% for senior citizen. Which will be higher than any liquid fund at the moment in the period of 365-727 days. I was checking for my dad to park his funds from surrendering of large cap equity mutual fund.The interest will be paid quarterly.

2 Likes

It might be a Cumulative one where Interest and Principal are paid on maturity.

1 Like

I scraped all bonds, combined the info with Zerodha instrument which is listed on BSE. Please download excel from here if anyone is interested.

1 Like

Whats the best way to park funds for short term say 1-6 months in NCD’s (looking for better returns than Bees after transaction costs and taxes). What parameters should we look out for so we can get max returns for 1 to 6 months. Does buying NCDs with lesser residual maturity a better option here?

I am a beginner in bonds scene, went through this thread, @kb_snn - Portfolio Analysis - Shailesh and few others like where discussions are mostly around debt/fixed income instruments.

To summarise my learning, in theory I would park my fixed income part of capital allocation in tax free bonds when available and for such duration when it is not available, buy AAA bonds/papers from good corporates and may be government securities.

However, I could not make an investment decision because 1) no more tax free bonds could be found 2) Post IL&FS and Essel fiascos funds investing in corporate bonds/debt funds seem riskier but I think it may be better than before because of the heightened awareness but still don’t know new exposures has any effect on NAV value due to past realisation of credit risk 3) don’t know if I can sell the bonds if I need to sell before maturity in the secondary market (I assume I should be able to) and there would be sufficient liquidity to avoid capital loss 4) GILT funds appear to be a dumb decision at this point based on @Yogesh_s asia index chart of returns on government securities because they are hottest at this time and there may not be much returns from now on 5) Looked at data shared by @deepender I don’t believe I know enough (and don’t have time and would take the option if I can get a fund to do it for a fee) to trade bonds in secondary market yet.

I would really love some direction and appreciate if the learned and experienced folks here can reply and guide.

1 Like

Fixed income investment - how much to invest and where to invest depends upon what role you want Fixed income to play in overall portfolio / financial plan .

No one strategy works . Questions that are imp

- Current source of income - How stable & predictable they are …

- What is your saving % ( of your income )

- What is your immediate , short term ( 3-5 years ) and long term ( 10 -20 ) financial goals are

- What is your assessment on return expectation / risk profile for your investments

Thank you Shailesh for replying, let me answer your questions first.

-

Current source of income - How stable & predictable they are …

Income is 95% salary, I consider it to be stable 5% could be dividends and returns from equities. -

What is your saving % ( of your income )

about 40% -

What is your immediate , short term ( 3-5 years ) and long term ( 10 -20 ) financial goals are?

Short term ie 5 year goal is to get closer to completion of building a performing equity portfolio, no immediate need for funds . Medium term 5 - 10 years to fund child’s education expenses and remaining to a retirement corpus that will support a reasonable and comfortable lifestyle. -

What is your assessment on return expectation / risk profile for your investments

Equity I tend to expect about 10 - 15% CAGR and I do like to take calculated risk and debt side I think 7-10% pre tax returns are good, I would not want to lose capital due to credit risk here.

I predominantly invests in equities when I find companies at reasonable or slightly above comfortable valuations. I also tend to not pump more money when markets are super hot. I am trying to build a debt allocation that will help me to park funds when I don’t find opportunities. Although I did not make a capital allocation model as crystal clear as yours that is tied to Nifty valuation, the mental model is something like that but I got to write it down sometime. I have couple of RE investments from the past which I am trying exit at the most opportune time.

@zygo23554 had posted earlier in this thread highlighting differences and expected returns in this thread which is very handy in choosing the right kind of fund. However, I am not quite sure the defaults and realised credit risks affect new investments into any of these.

I also liked the quasi bonds idea you shared in your PF thread and am thinking at an appropriate time I should execute on it. I am not certain if this is right time due to the uncertainty.

I think I managed to write down and share the questions I have in mind but not sure how useful it is for others who are reading it. Also, I am concerned if I am shifting this discussion off the track.

thanks in advance

-binu

Great …

Since your 95% of income is stable and predictable + your have 40% saving rate + you have no immediate need for money that means you can choose risker option for investing which gives higher return

I would suggest

-

80% of Pf should be equity through SIP route in Good Equity Mutual funds or ETF ( this will give > 12% return on long term basis ) . I would advise against direct equity investing as it is more time consuming and since your return expectation are modest you can easily achieve it through MF / ETF route with less effort + get good night sleep .

-

For rest 20% : After exhausting PPF , EPF route … rest in liquid funds of HDFC / Kotak etc ( this can be converted to cash fast typically within 1 working day and also has much lower credit risk

2 Likes

Thank you Shailesh, appreciate your guidance here. However, I enjoy reading and researching businesses and investing into equities gives me the purpose. I agree a debt exposure of ~20% will bring more balance to my investments.

1 Like

Can you explain more from your experience on what signals to look. How are these yield curve and credit spreads help here.