It will be difficult to any country even for US. These loans are through Exim bank which are G2G.

Cancellation will have impact on bilateral cooperation. Generally such things dont happen in diplomacy.

Secondly US want to re-enter Africa after China’s domination.

That’s my take. I may be right or wrong.

2 Likes

++

Also in recent results

Statements mention Sterling has given a loan of 2733 crores to a subsidiary.

Although when analyst asked they said it is usual business loan to Middle east subsidiary but the loan amount is colossal. That could be reason for derating.

1 Like

In the last concall, SWSOLAR management mentioned that they are testing some technology combinations with reliance. Glancing over Reliance’s annual report, I see that they have not mentioned any near-term targets. The current focus seems to be on Solar Module/Cell Manufacturing. The first line may be ready sometime this FY.

Even if SW meets its sales target of 8000 Cr, which they mentioned they would, it would do well, in my view.

Disc: Invested and biassed

4 Likes

Wondering if there is any impact on SW Solar because of Adani fiasco. Are there any projects from Adani group?

Disc: invested

1 Like

No, negative impact in longterm.

2 Likes

I had the exact same thought when investing in SW.

I ignored Nigeria and took into account only two aspects.

Without RIL SW solar can still grow order book by 10% annually for 1-2 year as there are heavy tailwinds in the sector and they are one of the biggest players.

With RIL the order book and revenue should go significantly up.

So unless they loose any big amount in arbitrations or courts stock should do good for next 3 years.

Disclaimer :Invested

3 Likes

Director for international projects resigned just before the biggest international project was about to be confirmed.

I can not restrict myself to not connect Nigeria progress with this one.

Do you mean to say that he resigned as the Nigeria project is not yet confirmed and he resigned due to the same?

When Solar is bigger theme across the world, It is quite possible folks with relevant experience might be sought after across the Globe which i personally experienced in IT during covid times, I would Keep a watch on Q3 guidance delivery of 2500-3000 Cr Rev and news on Nigeria order

7 Likes

I am new to this thread, can someone explain why swsolar gross margins are very low compared to kpi green?

One of the reason can be SWSolar does not do IPP that means they are not Independant Power Producer and are only concentrating on EPC projects vs KPI Green which has a mix of EPC and IPP projects.

3 Likes

One more question, the management has shied away from giving any EBIT guidance. Since their recurring revenue is declining very fast as %age of revenue, what are steady state EBIT margins one can assume?

They have given a ebitda guidance of 7% this fiscal.

Ebitda margins will increase in coming two quarters.

1 Like

Why do you feel so? Please elaborate?

Operating leverage will kick in once they do 3000 cr quarter.

1 Like

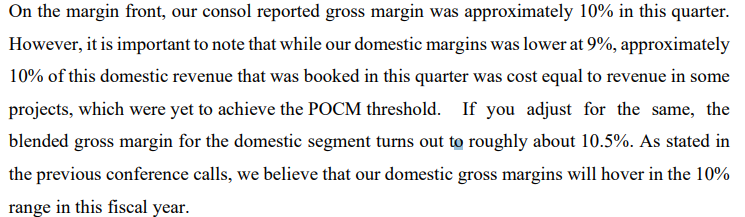

Hi Everyone, In the Q2 25 ConCall, they are saying margin approximately 10%. But when I check in Screener it is only 1.76%.

From ConCall:

Screener:

Can someone please explain this?

1 Like

10% is Gross margin whereas the figure in screener is Operating margin

2 Likes

10 % gross margin is for FY24 and what u are showing is only for sept2024 (Q2FY24)

both are 2 different things.