Expertise in power electronics is required. So it’s not a commodity product. That’s why everyone cant do it.

Other 2W OEMs don’t manufacture it for the same reason they outsource the engines of the ICE Vehicles.

Yes, in 2W EV market is open for all. There are no entry barriers but where as in 4W and above electric drive technology is required and it seems to be o e of the good opportunity in EV space.

Product localisation is also a very important parameter to consider and Sonacomstar is master in it but it’s valuation is a concern.

HBL power is also a wonderful stock to study in this regard. They are developing electric train drive technolgy and once it comes reality then it will rerate for sure.

Disc: Having positions.

1 Like

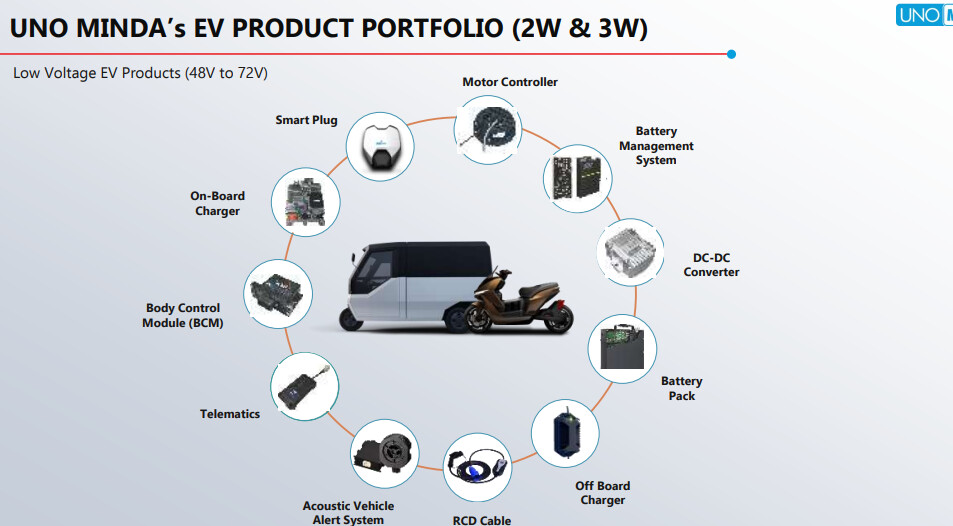

One interesting aspect of SGEM is that the MCU is used in EV powertrain

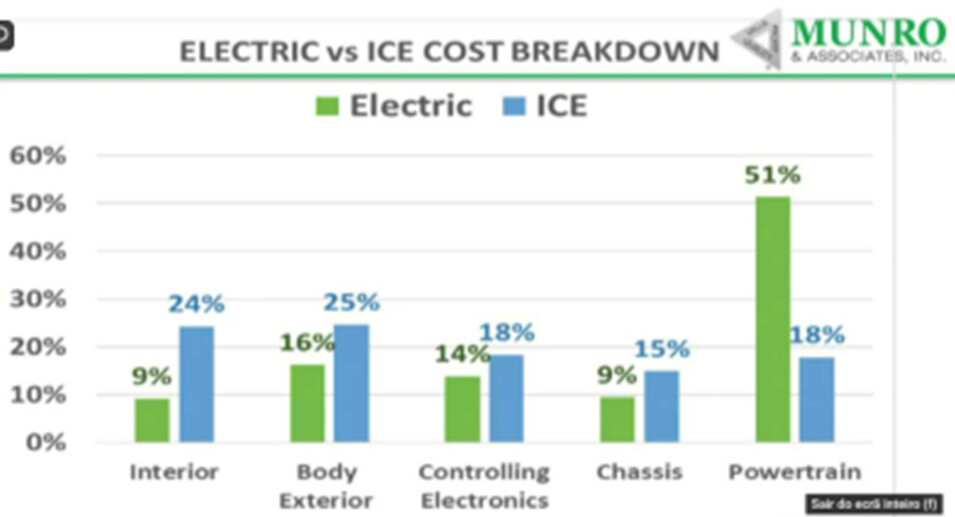

Interesting data point on EV powertrain:

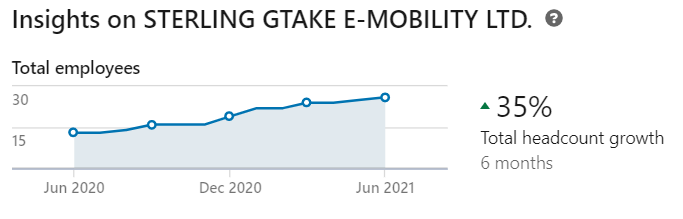

Seems like they are hiring aggressively. Gives comfort on growth guidance

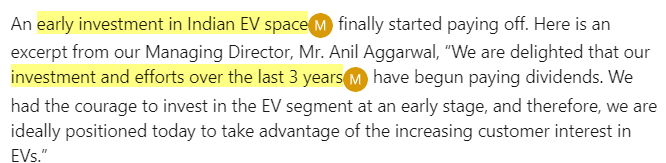

Seems like they were quite early in EVs

Will need to verify through channel checks whether they are truly sole suppliers

Good resources to understand technical details of MCU:

Disc-have a small tracking position

7 Likes

This is a key monitorable risk and break the investment thesis. No one is clear about this and no one has clear answers. If govt don’t give them permission to setup a JV , and if they pull out of these JV and ask for unreasonable compensation (which they can given they are in absolute control of technology) it will be disaster. Investor should give more than enough of discount for this scenario. It is question of when not if…

5 Likes

4 Likes

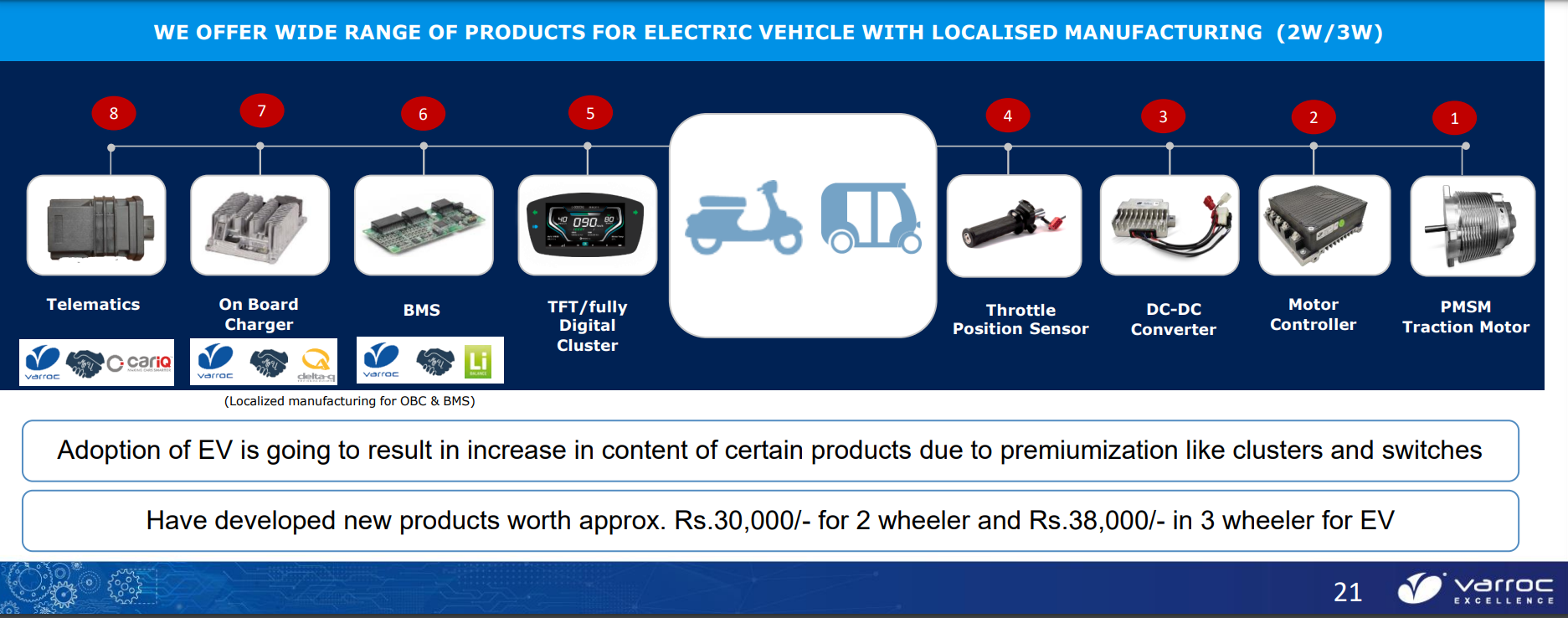

It seems like lot of players are targeting MCUs. Here is a screenshot from Q3FY22 Presentation of Sandhar

3 Likes

High debt levels and chip shortages are key set back for varroc…

@Worldlywiseinvestors would like to have your views on the following:

The biggest risk and deal breaker for the opportunity at this point is the FDI plan not going through.

Gtake mobility is awaiting the FDI approval. If the approval does not come through, the company is lloking to convert their agreement into a technical licensing agreement with 100% exclusivity. So as on data the JV is funded by Sterling and termed as a subsidiary.

Further, the fund infusion by the Chinese partner Jiangsu Gtake Electric Company (GTAKE) in Sterling Gtake E-mobility is not received yet because of the changed FDI guidelines issued by Government of India requiring approval of DPIIT, New Delhi, for which an application has already been moved on by the Sterling Gtake E-mobility. Link

If the FD&I doesn’t go through it might disrupt the whole JV as Sterling has heavy dependence on Jiangsu and is largely a price taker in this case.

2 Likes

Sterling Tools

- [ ] MCU order book now at 200 crs vs 175 last quarter

- [ ] Total capacity of 300k units per year (one shift working)

- [ ] Client count 11 vs 10 last qtr

- [ ] 30 more client is pipeline, expected to close 3-4 in next few weeks

- [ ] Got one leading LCV maker for MCU business. LCV MCU business is expected to start in 4th qtr of the current year

- [ ] 10crs/month is the needed to breakeven in EV business

- [ ] 38crs revenue for EV business last qtr

- [ ] Current capacity utilisation of 50% in EV business

- [ ] Margins will be lower in MCU business vs Fastener business but, ROCE is expected to be higher in MCU business.

- [ ] EV business is less capex intensive but more open heavy.

- [ ] Sole supplier to every customer it is working with

- [ ] OLA is facing battery supply issue from LG causing slowdown in MCU business as OLA is company’s biggest client as of today

- [ ] Plan to launch 3 more EV products next year

- [ ] Expect 50% growth rate for next two years in EV business. Expected to close this year with sales of 175crs.

- [ ] Electric component availability better than before. Freight cost also coming down

- [ ] Expect fastener business to reach 80% capacity utilisation by end of the current FY. Expect to reach revenue of 700-800crs in faster business in two years time.

- [ ] Maintenance capes of 25-30crs/ year in fastener business

- [ ] G-Take has applied to JV approval. As of now the company only procures material from G-Take and no royalty has to be paid. Incase the JV approval doesn’t come through the company is expected to go a royalty route.

7 Likes

The stock fell because of OLA taking a unexpected shutdown. Company also said in the concall that OLA has issue securing battery packs from Panasonic. But recently OLA has restarted bookings for S1 and S1 pro. This will be good for the Sterling.

3 Likes

So ola is again coming back to no 1 slot , so hopefully this stock should start performing again

2 Likes

look at ola sales on the vaahan platform.

July 3863

Aug 3440

Sept 9649

Its clear that ola is back and this will reflect in the 3rd qtr.

3 Likes

this is a very good for companies like sterling tools.

1 Like

ola sells 20000 2w in the month of October.

Since they dont allow more than 3 consecutive replies. posting my 4 msg below:

Does anyone have the link to the investor call?

The call web-link in the company doc is not working. If you anyone has the correct link please share.

Thanks.

4 Likes

| Q3 | Q2 | |||||||

|---|---|---|---|---|---|---|---|---|

| Standalone | Consolidate | EV | Standalone | Consolidate | EV | |||

| Revenue from operation | 15,133 | 20,783 | 5,650 | 15,391 | 17,860 | 2,468 | ||

| Other Income | 48 | 62 | 14 | 78 | 53 | (24) | ||

| Total Income | 15,181 | 20,846 | 5,664 | 15,469 | 17,913 | 2,444 | ||

| Expenses | ||||||||

| Cost of Material Consumed | 6,957 | 10,919 | 3,961 | 6,743 | 9,028 | 2,285 | ||

| Changes in stock | (485) | 133 | 618 | (735) | (980) | (245) | ||

| Emp. Exp | 1,109 | 1,293 | 184 | 1,108 | 1,249 | 142 | ||

| Finance cost | 224 | 235 | 11 | 206 | 236 | 30 | ||

| Dep | 767 | 789 | 22 | 783 | 801 | 18 | ||

| Stores & Spares | 1,277 | 1,288 | 11 | 1,449 | 1,458 | 9 | ||

| Power & Fuel | 1,112 | 1,116 | 3 | 1,269 | 1,274 | 5 | ||

| Other Exp | 2,833 | 3,226 | 394 | 3,052 | 3,327 | 275 | ||

| Total Exp | 13,794 | 18,998 | 5,204 | 13,875 | 16,393 | 2,517 | ||

| Exceptional Items | - | - | - | - | - | - | ||

| PBT | 1,388 | 1,848 | 460 | 1,594 | 1,520 | (74) | ||

| Tax | 379 | 456 | 77 | 379 | 533 | 155 | ||

| PAT | 1,009 | 1,392 | 383 | 1,215 | 987 | (228) | ||

| EBITDA | 2,330 | 2,809 | 479 | 2,505 | 2,504 | (1) | ||

| EBITDA Margin | 15% | 14% | 8% | 16% | 14% | 0% |

Ive assumed that the 100% difference between Standalone and Consol is attributable to MCU (EV)

3 Likes

What has transpered in board meeting on 8 May 23?

If one compares standalone and consolidated P&L

Gross margin for MCU business is only 20%

For fastner it’s 60%

My query is how much value addition sterling is doing for Chinese MCU…

In one of the CONCALL they told value addition is almost 50%, but on looking at gross margin value addition looks much less…

Another Issue is management is not clear about the Arrangement with Chinese player…

7 Likes

Sterling tools -

Company overview and FY 24 result analysis -

India’s second largest manufacturer of Fasteners for

Auto OEMs. Makes fasteners for Chasis, Engine and other Standard applications. Company ( through its fully owned subsidiary - Sterling GTAKE mobility ltd ) manufactures and sells Motor Control Units ( MCUs ) for EVs in India

Company’s mkt share of MCUs in 2 wheeler EVs @ 30 pc

Manufacturing facilities - 04 for fasteners and 01 for MCUs

Q4 FY 24 results -

Revenues - 269 vs 212 cr

EBITDA - 31 vs 22 cr ( margins @ 11 vs 11 pc )

PAT - 16 vs 8 cr

Full FY 24 results -

Revenues - 932 vs 772 cr

EBITDA - 108 vs 98 cr ( margins @ 12 vs 13 pc )

PAT - 55 vs 48 cr

FY 24 Revenues breakup -

Fasteners segment - 608 cr

MCU segment - 323 cr

Company has announced setting up of Greenfield capacity in India to make magnetic and electronic auto components in a JV with Yangin Electronics. Yangin is a major supplier to Kia and Hyundai Motor companies. Aim to generate a 200 cr/ yr kind of business from this initiative ( inside next 5 yrs ). A partnership with Yangin is expected to help company have firm visibility on orders from the Korean OEMs in India. Beyond the Korean OEMs, company will also target the Indian OEMs for these Electro-Magnetic components

EBITDA margins for Fasteners segment @ 14 pc and 7 pc for MCU segment for FY 24

MCU segment is expected to keep expanding margins gradually and reach the targeted 10-12 pc margins in 2-3 yrs

MCU capacity now @ 6 lakh units / yr. Company sold aprox 4 lakh units in FY 24

Revenue potential from fasteners segment is 750-800 cr / yr without any further CAPEX

Subdued performance in fasteners business in FY 24 is due to 17 pc de-growth in the business from Farm-Equipment / tractors business. Other segments like - Cars, 2-Wheelers grew steadily

An avg MCU costs aprox 8-12 pc of the cost of a two wheeler - depending on model to model

Company is the single source supplier of MCUs for all the 2-wheeler models that the company is supplying to ( this is a big deal - IMO )

Aiming to grow by 30 pc in the MCU segment in FY 25 ( Apr month sales were however subdued due ending of FAME-II subsidy scheme for EVs on 31 Mar 24. Expect a reversal going fwd )

Have lined up a capex of 60 cr for the fasteners and MCU businesses in FY 25. Plus there will be additional capex on the new JV ( amount not yet finalised )

Disc: bought a tracking position recently, biased, not SEBI registered

2 Likes