India’s second largest fasteners manufacturing company entered in to mammoth EV space:

Its collaboration with the leading Japanese fastener manufacturer, Meidoh (acquired 5% stake in the company in FY2018), has helped the company to improve its product development capabilities for specialised fasteners.

The company entered into a joint venture agreement with China’s Jiangsu GTAKE Electric Co. to design, manufacture and supply motor control units in India for EV in FY20.

The joint venture company will be a subsidiary of Sterling Tools and will commence production by Q1 of 2021. The agreement calls for the companies to manufacture motor control units (MCUs) domestically to cater to the Indian automotive market as well as to develop local design engineering, application support and after sales service capabilities as per the requirements of the Indian industry.

In the proposed joint venture company (JVC), STL will hold 51% stake while the remainder 44% stake will be held by GTAKE.

GTAKE is an R&D led organization and 40% of its workforce is engaged in the function. The company was incorporated in 2009 and has a dominant market share for MCUs in China. The company has developed several unique products that integrate additional powertrain functionality. GTAKE controllers optimize torque characteristics and efficiencies of electric motors over wide operating conditions.

Valuations:

Market Cap ₹ 775 Cr.

Sales ₹ 353 Cr.

High / Low ₹ 233 / 160

Stock P/E 32.9

Dividend Yield 0.93 %

ROCE 9.45 %

ROE 7.37 %

Debt to equity 0.27

Equity capital ₹ 7.20 Cr.

OPM 16.7 %

Promoter holding 65.8 %

Recent events:

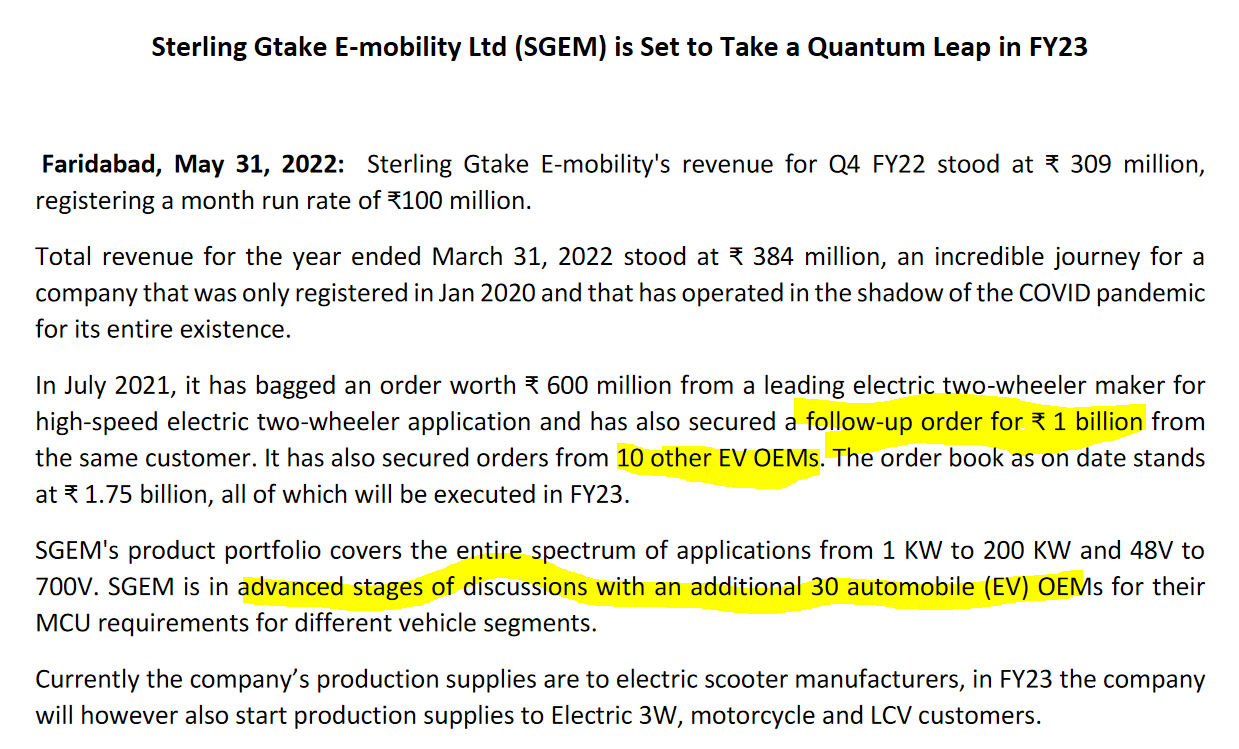

Sterling Gtake E-mobility Ltd (SGEM), a manufacturer of motor control units for electric vehicles has bagged an order worth Rs 60 crore from a leading electric two-wheeler maker.

The company said it is also in advanced stages of discussions with over 20 electric vehicle (EV) manufacturers for supply of motor control units (MCUs) for different vehicle types, including two-wheelers, three-wheelers, passenger vehicles and commercial vehicles.

“With the contracted business commencing from next month, SGEM aims to emerge as the largest domestic supplier of MCUs by the end of 2021,” the statement said.

Cons:

- Each unit cost of MCU for 2W/3w is not known.

- Exact Margins for this product

- Technical support from China based company.

Ola, Hero electric, Ampere of Greaves, Revolt, Ward wizard like OEMs are planning for huge production of EVs. This small cap auto ancillary is well placed to capture the gigantic EV market.

Disc: Invested

With thanks

Be and Make

Hi

Through recent management interaction answers to few questions.

- what would be selling price per unit of MCU. ?

The selling price per mcu for the current order is around11000/12000 per unit. However with four wheeler and higher capacity vehicles MCU price can go substantially up.

2)What’s the capacity of sterling gtake plant and what can be asset/ turnover. ?

It seems that this is an assembling unit and therefore in the current plant they can even go upto 200 cr of turnover.

3)Also any update on fund infusion from Gtake, which is getting delayed due to covid and changed fdi guidelines. ?

The situation is status quo but they are hopeful of getting the approval. If in the worst case if the approval does not come both parties are keen to continue their technical collaboration with some changed economics.

-

the contingent liability is towards export obligation and liability is sales amount and not duty amount. They said there was some misunderstanding by marcellus in this front. Also the export obligation is for next 5 yrs. One will be able to see this contingent liability coming off from current year.

-

The MCU order is for 1 year and the vision of management is to bring minimum 500 cr sales from this JV in five years. Also there is en devour to increase wallet share per client here.

-

Resignation of Mr Atul Agarwal as CFO and appointment of Mr Pankaj Gupta was mainly to bring professional cult in the company, while he continues as director.

Hi @Gandhi_Jayesh, @Stocks_To_Win - thank you so much for some great insights esp. with no con-calls, analyst coverage on this stock, and a totally lacklustre AR with the management not keen on putting any details (albeit the recent Credit Report from ICRA was far more exhaustive and covered a good amount of detail). Just wanted to ask you a couple of questions -

a) How much of an impact do you see on the revenues with the demise of ICE, think EVs would require a lot lesser amount of fasteners?

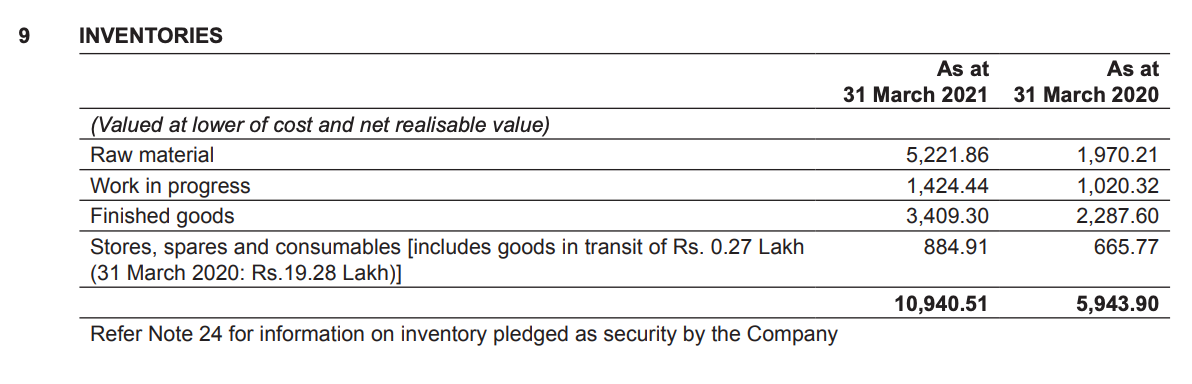

b) Why has the Working Capital cycle deteriorated so much in the last 2-3 years.

Snapshot from the AR below , looks like the increase in the inventory could be due to hoarding of raw materials by the company in anticipation of the increase in the commodity prices?

This should be Ola by the looks of it, and they have recorded bumper sales, hopefully we see something meaningful in the results of this quarter.

Ola says it sold Rs 1,100 crore of electric scooters in two-day sale

STL seems to have reinvented itself through Gtake JV.

Disc.: not invested currently

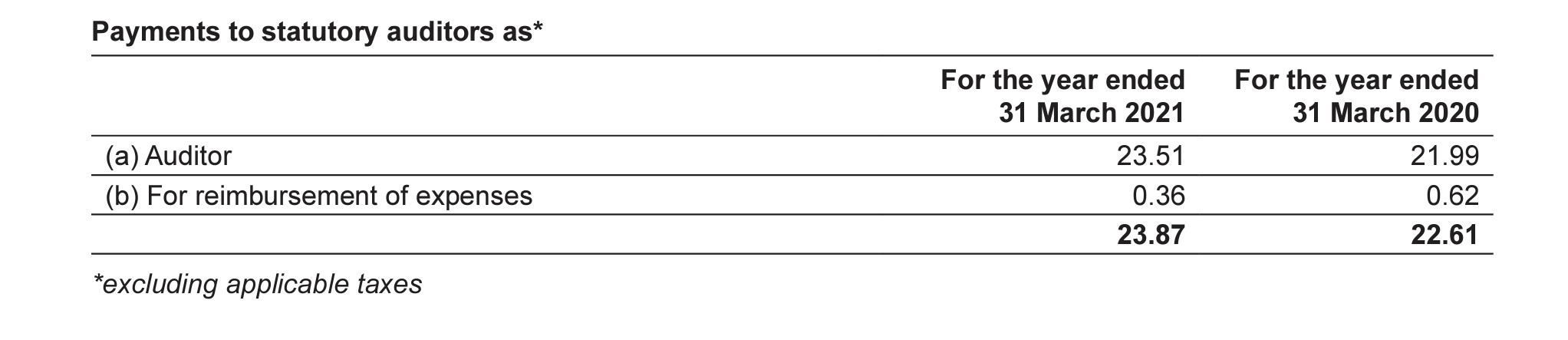

Marcellus comments: “The key reason for exit from Sterling Tools is deterioration in its accounting score under the Marcellus’ proprietary forensic accounting model triggered by below par scores on the following ratios: (i) growth in auditor’s remuneration relative to the revenues; (ii) contingent liabilities as % of networth; (iii) miscellaneous expenses as % of total revenues; and (iv) yield on cash and cash equivalents.”

Link- The Three Ps of a Global Little Champ - Marcellus

Disc- no holdings

From latest concall

Now for the first full year of operation in FY23 first 12 months of operations we will be profitable. I would not like to hit a number, but I can assure you we will Sterling Tools Limited May be profitable or be it on a low margin perspective.

On MCU Price

Two-wheeler starting from 9, 000 going to a bus public transport vehicle about 2 lakh roughly. FY23 bulk of the revenue will come from the two-wheeler and three wheeler space. Of the 175 cr orderbook 80% from 2 wheelers, 10% from 3 wheelers and rest from others.

can you please share fy21 annual report?

Dear Souresh - Did any where they specified about their margins in this segment?

With thanks

No they didn’t mention anything specifically. Whatever I replied is from their concall. That’s only what they mentioned “low margin”. single digit or double digit nothing.

The most important thing to figure out is not saurabh mukherjee sirs comments & counter points but rather the competitive advantages of sterling

Why do sterling mcu sell more than Bosch? Do they sell more than Bosch as claimed in concall? How large of a mcu co is gtakes in China ?

How would sterling Pay gtakes for the royalty or jv interest from day of 1st sale to the point at which the agreement willl be formalized ?

On competition

- Right now, the only companies in India I mean there is a wide range, but the only companies that I actually selling large production volumes would be MAHLE and maybe Hella and Bosch may be little bit. So, I mean these three companies most of the companies have not been able to industrialize the products yet. They are mostly catering to lower end of the EVs which are like commodities. See there is a lot of large segment of business which is there in the low-speed scooter range which is not a market we are addressing

- EV is a new field. In china it’s just 10 years old. So experienced player like Bosch does not have that much experience in this field. But I just say I genuinely believe that in the EV space it is a very level playing field everyone is new.

- It seems like they are getting the first movers advantage for higher end evs like high speed scooters.

- GTAKE is having more than 10 years experience in this field

On royalty fee

Dear souresh- Good point to highlight it but there are no 100% working fixed rules to success in stock selection. Every fundamental rule has some limitations or conditions.

MCUs, batteries, vehicle/train drives, BMS, electric motors are the key components to watch out for…

Sonacomstar, KPIT, HBL power are the some of the stocks working on above themes and HBL power looks attractive…

SOIC team came with a detailed stock study on Sterling Tools and its a must watch video.

With thanks

Stocks to win

Dear Members I have Some Question

1)Since MCU is about 10% of cost of 2w why can’t other 2w companies can manufacture it .

2)Many Auto Ancillary Company can announced their plan to enter MCU then how it will Impact Sterling

My both question focused on Long term views