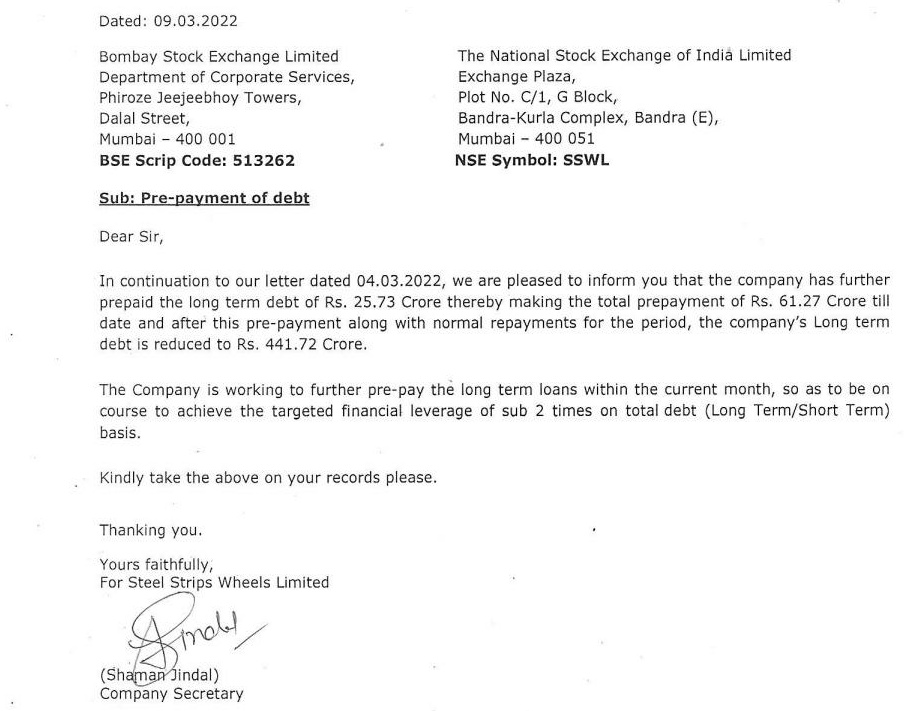

SSWL makes repayment of 61.27cr debt.

Long term debt reduced to 441.72cr.

Expects further repayment of 170cr debt in FY23.

Dividend policy to be announced in Q4.

For more details watch -

SSWL makes repayment of 61.27cr debt.

Long term debt reduced to 441.72cr.

Expects further repayment of 170cr debt in FY23.

Dividend policy to be announced in Q4.

For more details watch -

A detailed report on SSWL.

Regards,

Raj

Disc: Invested

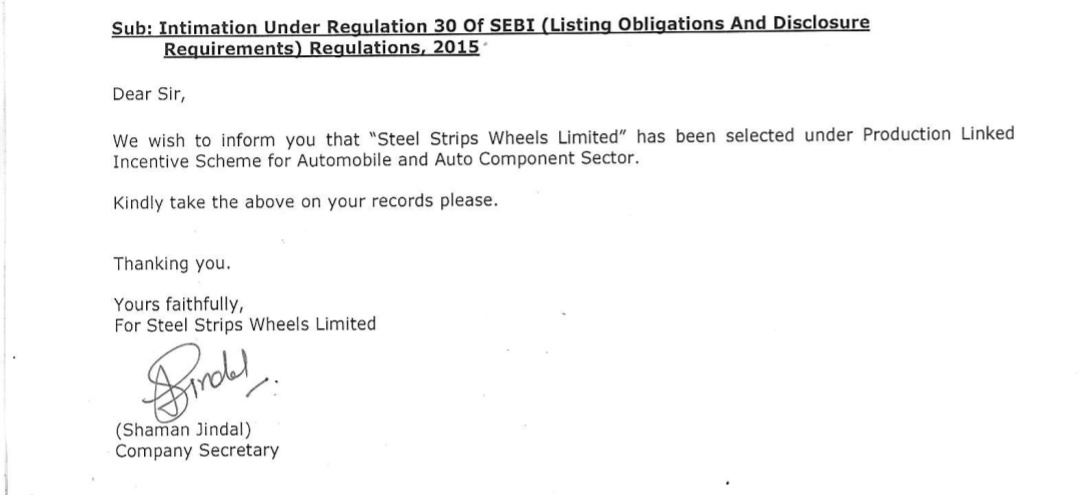

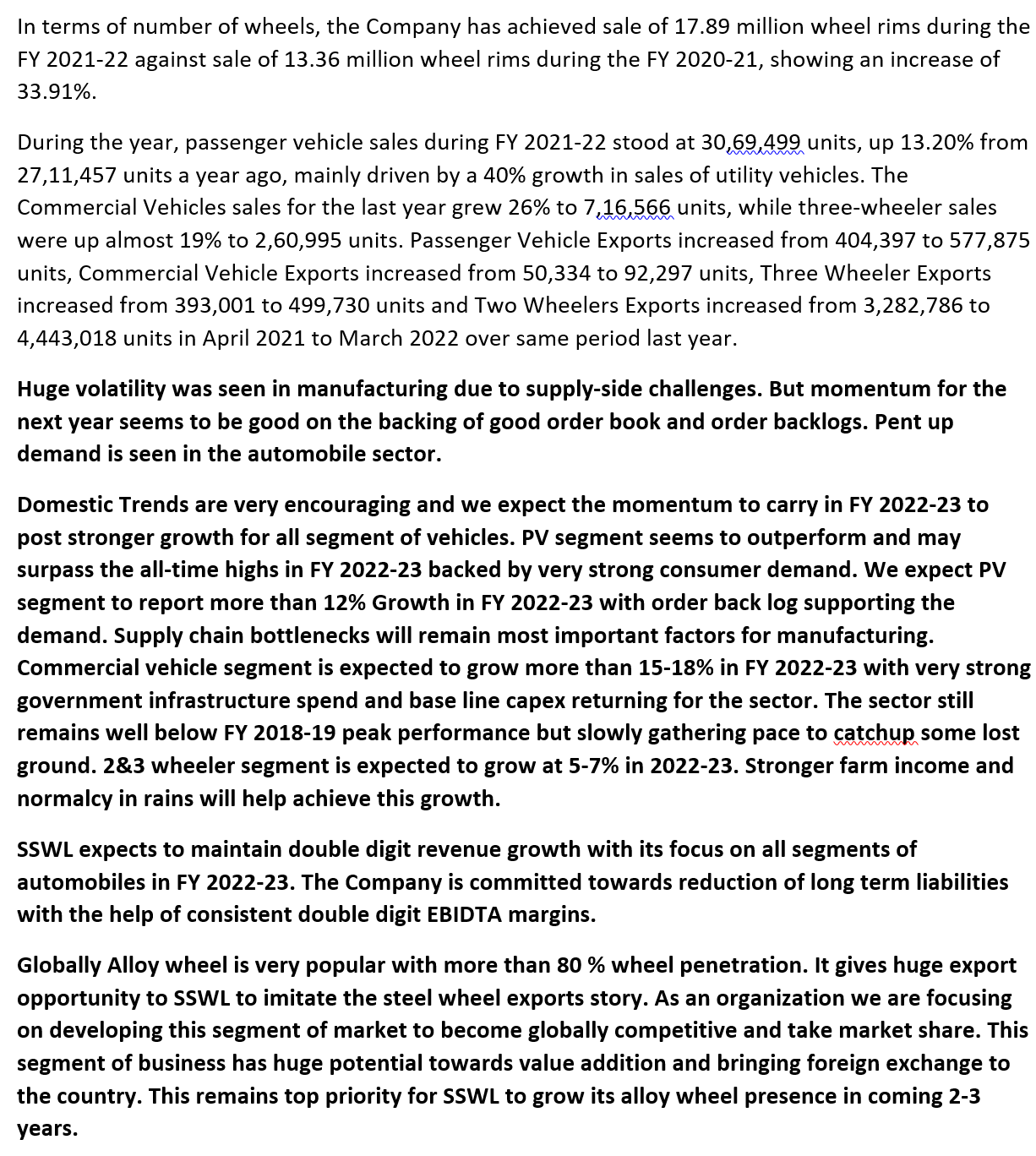

Steel Strips Wheels Limited (SSWL) has been selected under Production Linked lncentive Scheme for Automobile and Auto Component Sector.

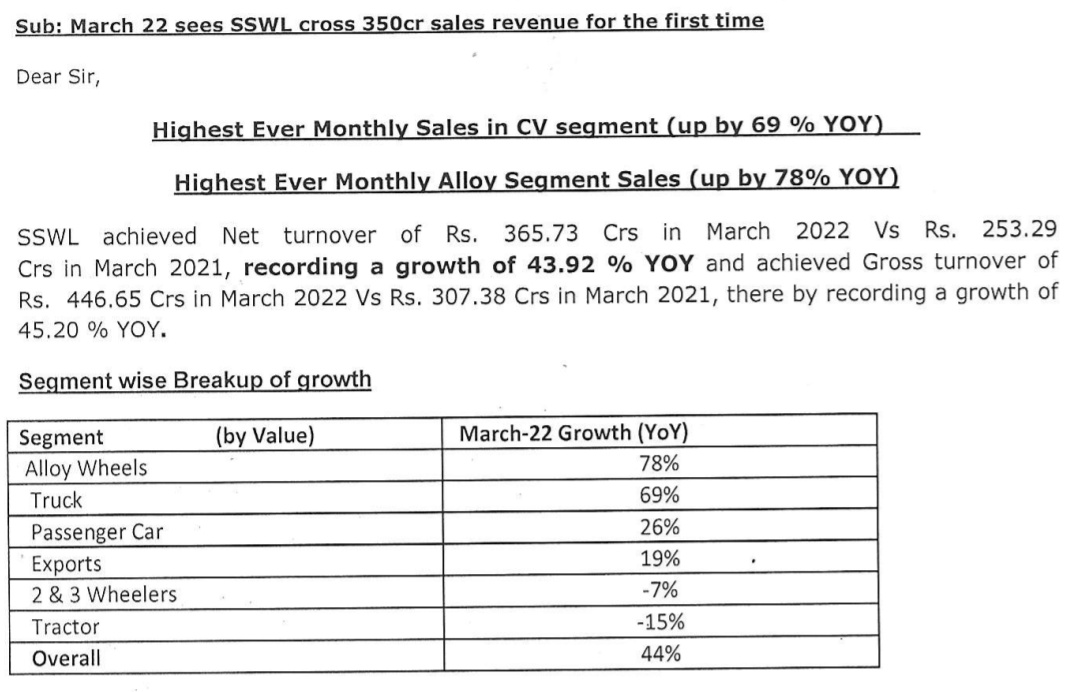

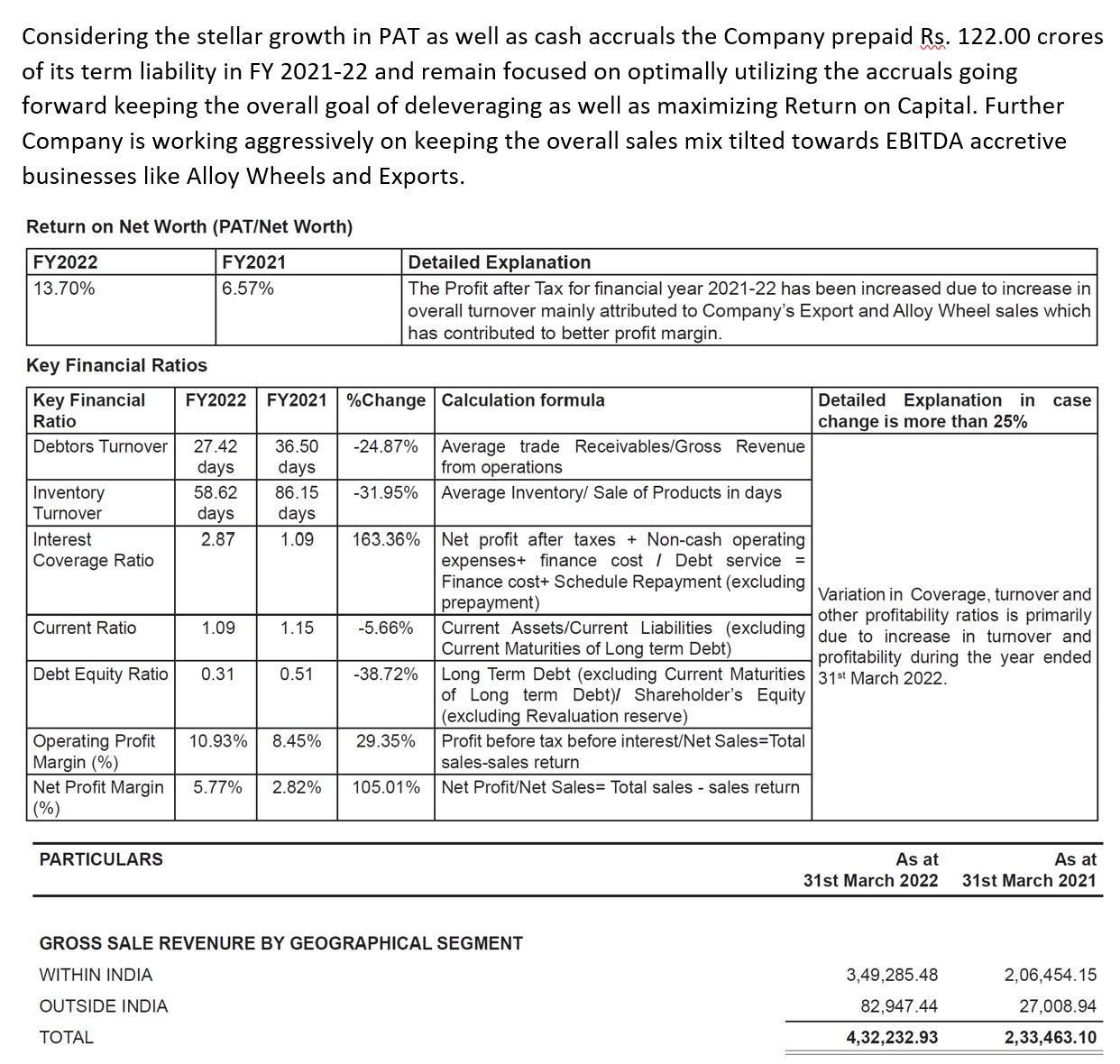

SSWL achieved Net turnover of Rs. 365.73 Crs in March 2022 Vs Rs. 253.29 Crs in March 2021, recording a growth of 43.92 % YOY and achieved Gross turnover of Rs. 446.65 Crs in March 2022 Vs Rs. 307.38 Crs in March 2021, there by recording a growth of 45.20 % YOY.

Very good sales considering Russia-Ukraine issue and supply chain issues.

They have also repaid Rs. 122.89 Cr debt bringing down the Long term borrowing to 374.85 Cr.

Management has so far walked the talk on all aspects -

Key thing to monitor now is margins.

April 2022 Sales at 329 Crs (2nd Highest Monthly Sales)

Some slowdown MoM but still a very good run rate if maintained

Key thing to note is exports are down 31% YoY.

CV upcycle helping SSWL as realization on CV wheels is 2.6x Average realization.

Awaiting results on 13th May.

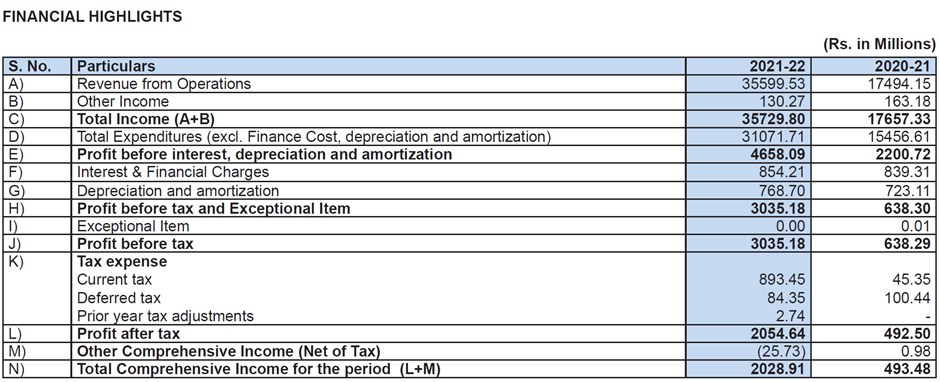

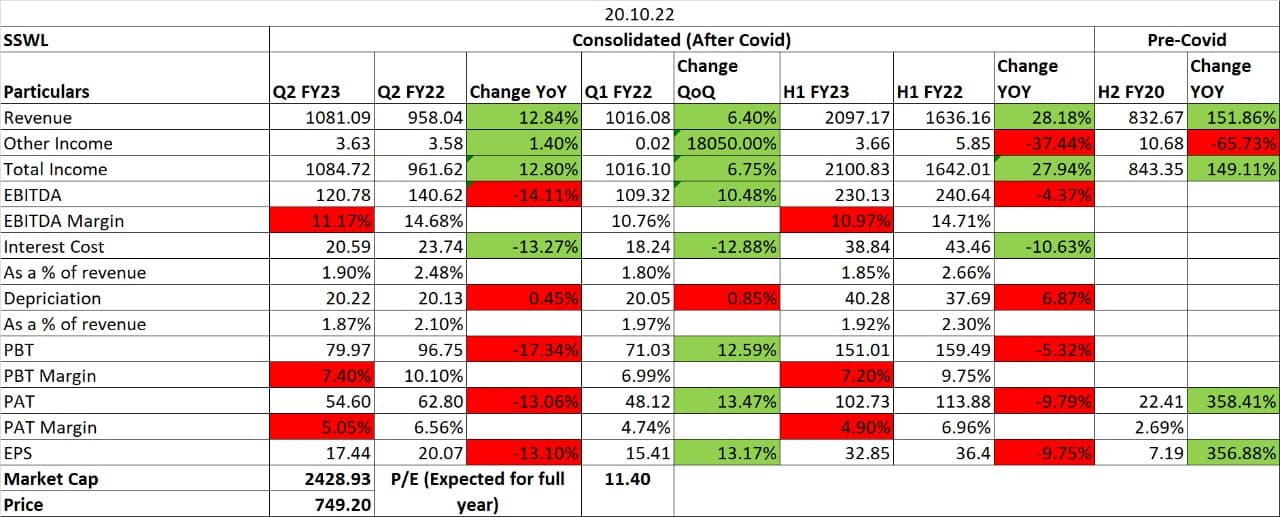

SSWL came out with Q4 numbers. Met the estimate of 3,500 Cr. top line

Solid 400 Cr. odd cashflow for FY22 for a company with 2,400 Cr market cap. With CV cycle looking upward trajectory going forward, and alloy wheel penetration increasing - Company seems to have a good platform to take advantage of these tail winds. Capacity addition acquisition via NCLT at a reasonable price would help. Valuations are undemanding.

@vikas_sinha - How do you read the numbers and your anticipation on business performance please

Disc-Invested.

Nice summary! Thanks!

Yes, seems to be on track. Even with commodity prices shooting and logistics pressures, managed one of the best quarters in FY22. Somehow the management quality is not very inspiring, bit too boastful and then there is the unusual tax bill of the past 3 quarters. Though disclosures are very regular, even if bit pompous. Best quarters seem lined up next with valuations quite reasonable. Hopefully they plan a quick capex soon, which would kick up valuations.

My notes from Earnings call

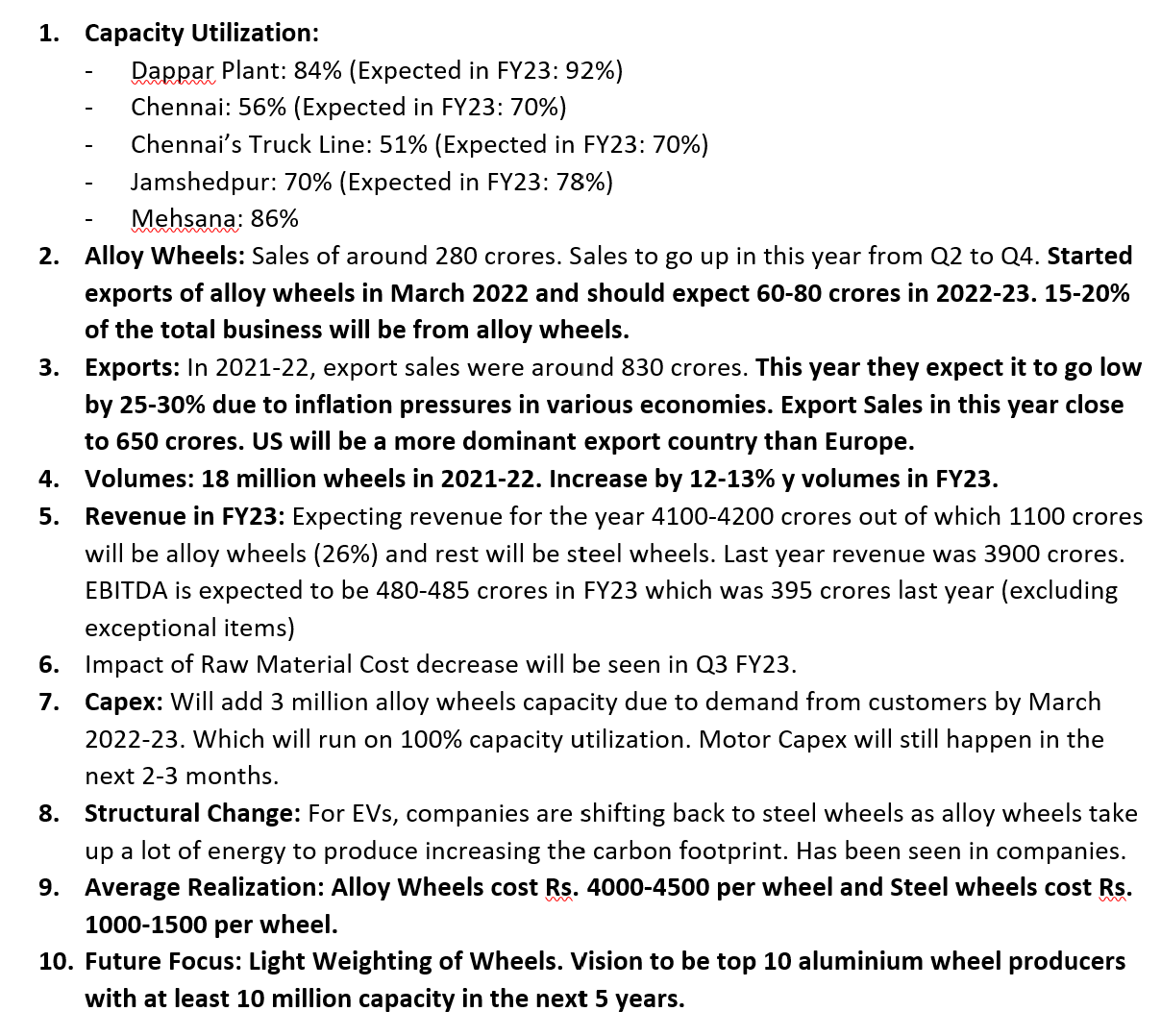

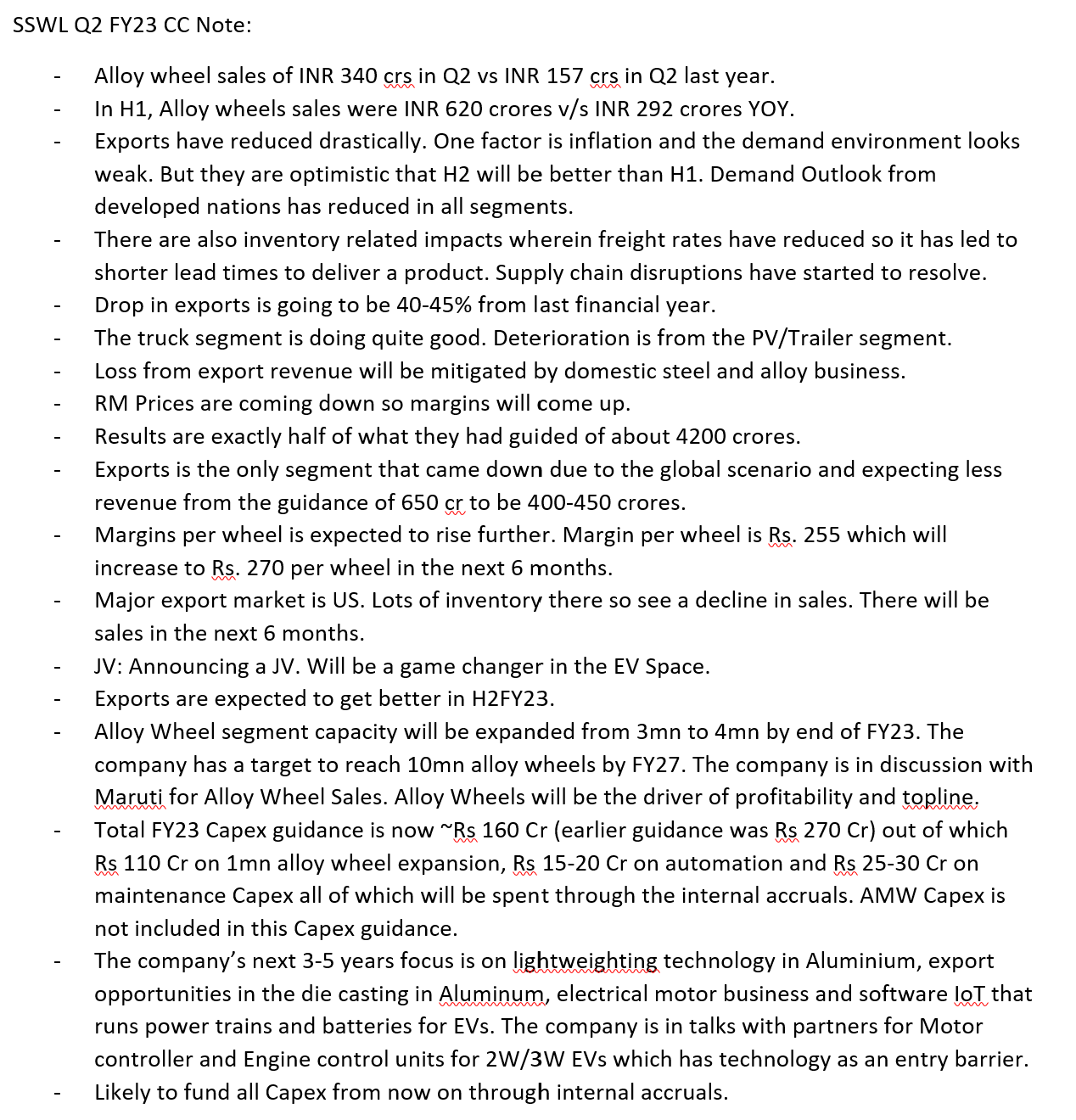

Revenue guidance 4200-4300 Cr FY23 against 3500 Cr in FY22; Overall volume guide 11-12%, For alloy wheels 33% volume growth expected.

Current plan utilization ~ 68-69%. With current capacity 5,000-5,500 Cr revenue feasible. WIth AMW acquisition additional 1,000 Cr revenue can come.

Company level margin to remain 11-11.5%; If RM prices cools, the margins have potential to improve

Alloy wheel margins are 14-15%

Increase in raw material prices - Steel and Aluminium, these gets passed to customers

Capex wise - AMW acquisition from NCLT. This is likely to take 4-5 months.; 60-80 Cr. capex for this

Including working capital, total debt is 775 Cr (including short term+long term); To repay 95-100 Cr. this year

Complete reduction of pledge until FY24.

Last year export ~825 Cr. led by export to US.

Export to be 50% and domestic sell to be 50%

Expect 115-120 Cr Ebita run-rate every quarter

To penetrate US market with alloy wheels, Company would be adopting the same strategy as they adopted in case of steel wheels

Management anticipate that they will be able to win business from Maruti towards the end of FY23 for alloy wheels

hi,

who are the other players operating in the product segment?

can someone help me with this?

Thanks in advance

one of the players is Minda Ind.

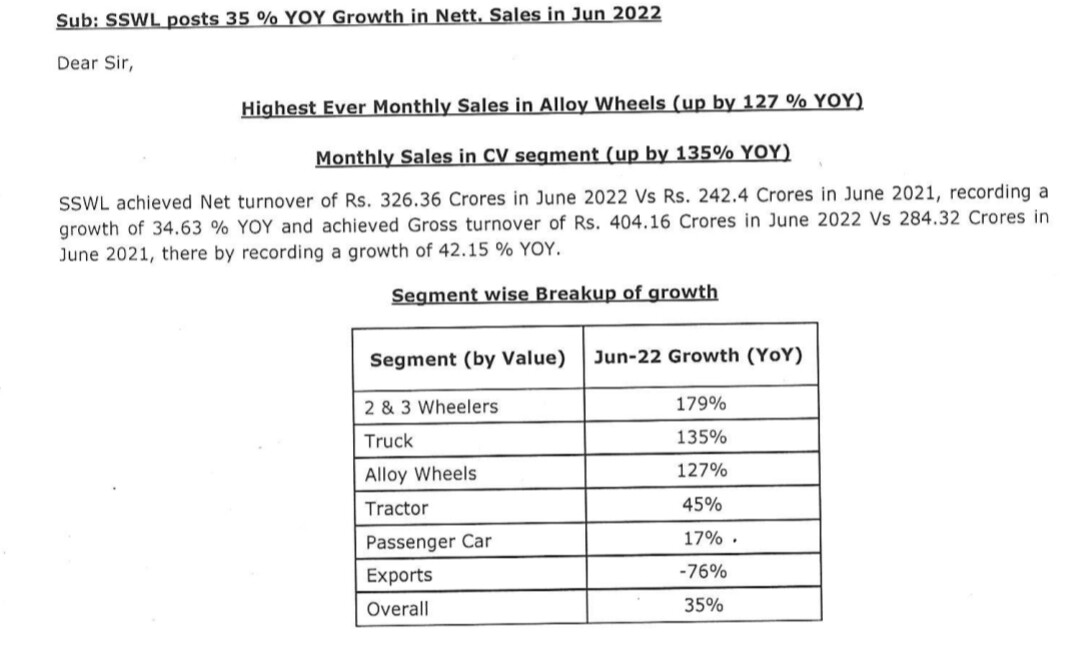

SSWL achieved Net turnover of Rs. 326.36 Crores in June 2022 Vs Rs. 242.4 Crores in June 2021.

Exports are down 76% YoY due to inventory build up by OEMs and general slow down in US/UK.

Domestic has picked up the slack with PV and CV leading the sales growth.

Management claims they are now the No. 1 player in Alloy wheels in India in just 2 years time from starting.

Sees good PV sales and hence higher alloy wheels sales.

Says 2 plants are fully booked with good order book overall.

EBITDA for FY23 should be around 450cr mark with increase in % EBITDA margins (while absolute EBITDA will be same as during the RM hikes they passed only input cost hike and their absolute EBITDA per wheel remained same)

Planning to venture into Motor with wheels category (Hub motor wheels?) For 2 and 3 wheelers initially.

Says this market’s size is 5000 crs and they aim to capture 1000 crs in 3 years time with initial capex of 70-80crs and upto 300crs capex for achieving 1000cr topline

Implies 3x asset turnover and says it’s a high margin product which no one else is supplying as a combination.

For this they are scouting startups in India and in Europe for technology and know how.

Summary of latest credit rating report from India Ratings:

Rating update and rational: Upgrade of Long-Term Issuer rating to ‘IND A+’ from ‘IND A-’. The Outlook is Stable. The upgrade follows a substantial improvement in SSWL’s credit metrics on account of a solid improvement in the operating performance, and an increased share of higher-margin business (alloy + exports) in the revenue, leading to a significant improvement in business profile.

Expectation: The agency expects the company’s net adjusted leverage to remain at 2.25x-2.5x in FY23, on the back of strong profit generation, although partially offset by the expansion plans over this period. The company’s leverage could be around 2.5x if the acquisition of AMW Auto Component Limited (AMW, which will increase its capacities in steel wheel rims) materialises during FY23. SSWL’s interest coverage (EBITDA/interest expense) rose to 5.3x in FY22 (FY21: 2.4x) due to improved operating profitability and is likely to remain around similar level in FY23.

With the expansion undertaken by the company over FY18-FY22, it is now a leading supplier of alloy wheel rims in the country, through its plant in Mehasana (Gujarat), with a total facility size of 3 million units at FYE22, which is operating at more than 80% utilisation levels. The company’s capacity is likely to increase further to 4 million units by FYE23, making it the largest alloy wheel manufacturer in the country.

Alloy Wheel Segment: The company has a strong share of business in the alloy wheel segment in the models it caters to Hyundai Motor India Ltd, Mahindra & Mahindra Ltd, Tata Motors Ltd, KIA Motors India Pvt Ltd etc. The revenue from alloy wheel rims contributed 20% to the FY22 revenues (FY21: 19%; FY20: 7%).

Liquidity Indicator: The company’s net working capital cycle (creditors exclude LC acceptances) improved to 85 days in FY22, primarily due to a correction in its inventory holding, which had increased significantly during FY21, and a yoy decrease in the blended receivable days as the company’s sales to customers with a shorter credit period increased. The company had unencumbered cash and bank balances of INR232 million at FYE22. Ind-Ra expects SSWL’s FCF to remain positive in FY23, primarily due to its lower yoy capex plan of INR1,000 million in FY23 (FY22: INR1,691 million, FY21: INR928 million), largely towards alloy wheel plant expansion. The management also expects a cash pay-out of sub-INR1,500 million towards the AMW acquisition which Ind-Ra has factored in for 2HFY23. The capex and acquisition put together are likely to be funded partly through internal accruals and partly by incremental debt.

Debt repayment and promoter pledge: SSWL has term debt repayments of INR951 million in FY23 and INR901 million in FY24, and the agency believes it will be met through internal accruals. On 10 June 2022, SSWL’s promoter pledged shares reduced to 17.6% (March 2022: 19.5%, March 2021: 45.0%, March 2020: 49.9%).

Locational Advantage and Strong Customer Relationships: SSWL’s Chennai plant is located close to the port as well as Renault Nissan Automotive India Private Limited, which enables the company to keep its freight costs cost low and helps it cater to the export markets. Its Jamshedpur plant primarily caters to the requirements of Tata Motors, and its proximity to the latter and Tata Steel Ltd gives it an advantage over its competitors in terms of lower logistic and raw material costs.

SSWL’s alloy wheel plant in Mehsana is situated close to Tata Motors. SSWL has strong relationships with its suppliers – Tata Steel and Sumitomo Metal Industries Ltd, which are also strategic investors in the company, with a stake of 6.97% and 5.45%, respectively, at end-March 2022. SSWL has technology tie-ups with Ring Techs Co Ltd, Japan.

Share of Business: SSWL has healthy market share of 50% in PV, 53% in medium and heavy commercial vehicles, 44% in tractors, 70% in off the road segment, and 30% in two and three-wheelers.

Capex: The steel/alloy wheel business is a capex-intensive business. SSWL has undertaken continuous capex totalling INR7,798 million over FY18-FY22 primarily to expand its manufacturing facilities, including the expansion of its alloy wheel plant. At end-June 2022, the company was operating at around 80% utilisation levels in most of its existing plants, except CV. This necessitates SSWL to incur incremental capex towards capacity expansion to maintain its market share and be the preferred supplier for its customer. Ind-Ra takes comfort from the fact that the steel wheel rim capacity is likely to increase with the AMW acquisition, while alloy wheel expansion would continue in a phased manner at its Mehsana plant. However, any greenfield acquisition could delay the deleveraging exercise for the company.

Read the full report here.

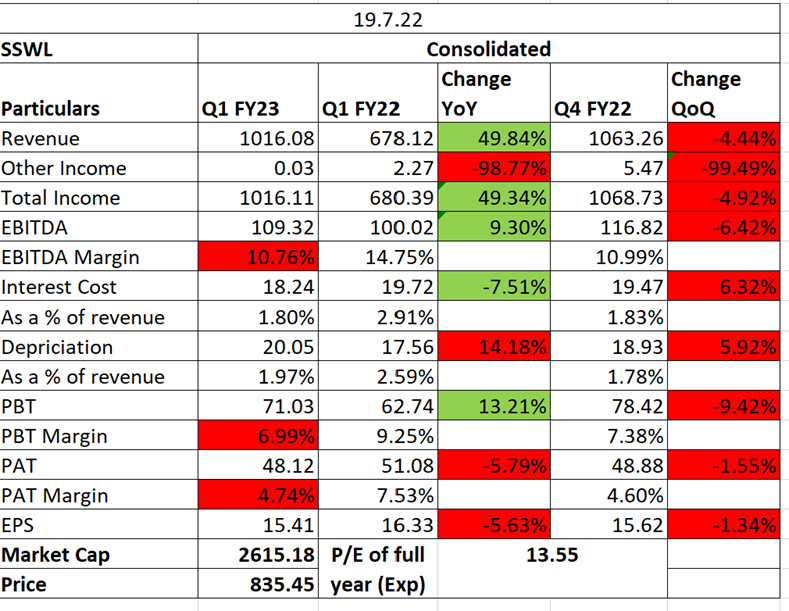

Result update: Healthy growth of 50% YoY on topline. The profitability has reduced on account of increase in raw material cost by 4%(67% in Q1 2023 against 63% Q1 2022) and other expenses(must be logistics related).

Stock Split - sub division of shares: Company has approved subdivision of shares from current Rs. 5 per share to Rs. 1 per share.

Read the results update here.

AJ

Disclosure: Remain invested and have a positive outlook.

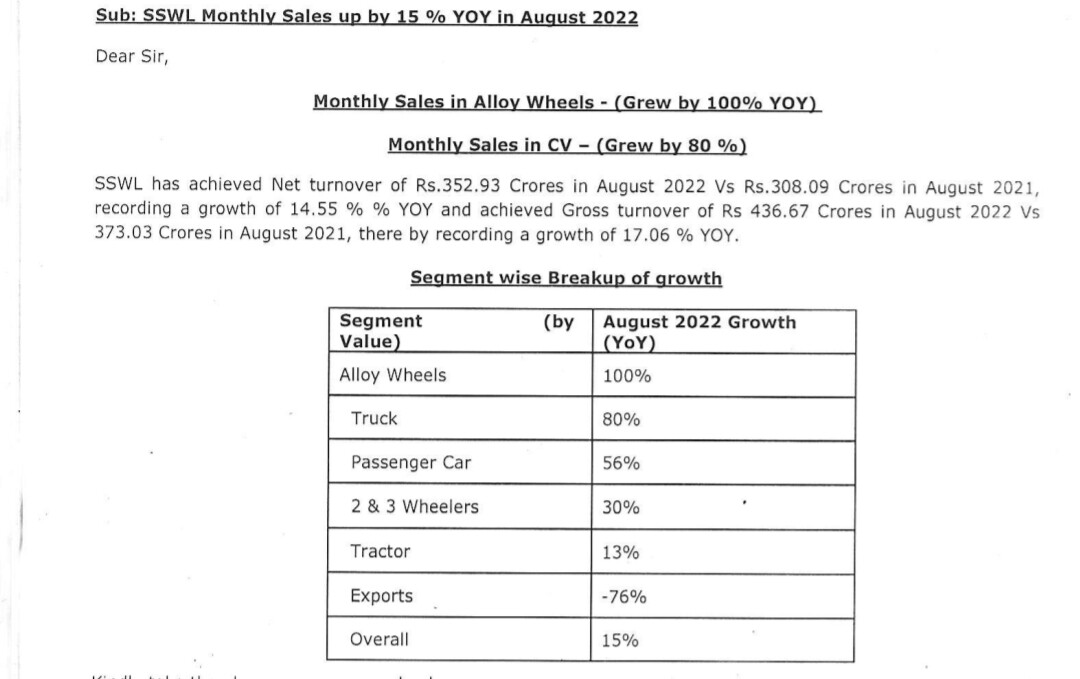

SSWL has achieved Net turnover of Rs.352.93 Crores in August 2022 Vs Rs.308.09 Crores in August 2021,

recording a growth of 14.55% YOY.

Commodity (Steel, Aluminium) prices have cooled off in the last 3-4 months and since they make up a good % of price makeup I bet the volumes have increased as the topline is around the March 2022 365 cr revenue mark.

Wish they’d give volume disclosure as well to get a clearer picture.

Since they operate on fixed absolute EBITDA margin per wheel bottom-line should benefit from volume increase.

Exports are down 76% YoY still the net sales are near ATH.

When exports kick back in this could propel the monthly sales to 400+cr run rate however the recession in Europe and USA could delay that for some quarters.

Drop in export sales more likely more than they expect… (Oct revenue data shows a export degrowth of 84% (valuewise) )

But should be covered through domestic sales…