Has anyone contacted the co to get some queries answered and got the reply from them?

Sent them an email but no reply yet!!!

strong text

Has anyone contacted the co to get some queries answered and got the reply from them?

Sent them an email but no reply yet!!!

strong text

A very informative thread on SSWL

If someone has subscription to this website, we can dig out some major export trends for SSWL. The graph shows a S curve towards the end but the period is unclear.

Fellow boarders, is anyone tracking this closely?

I have a query:

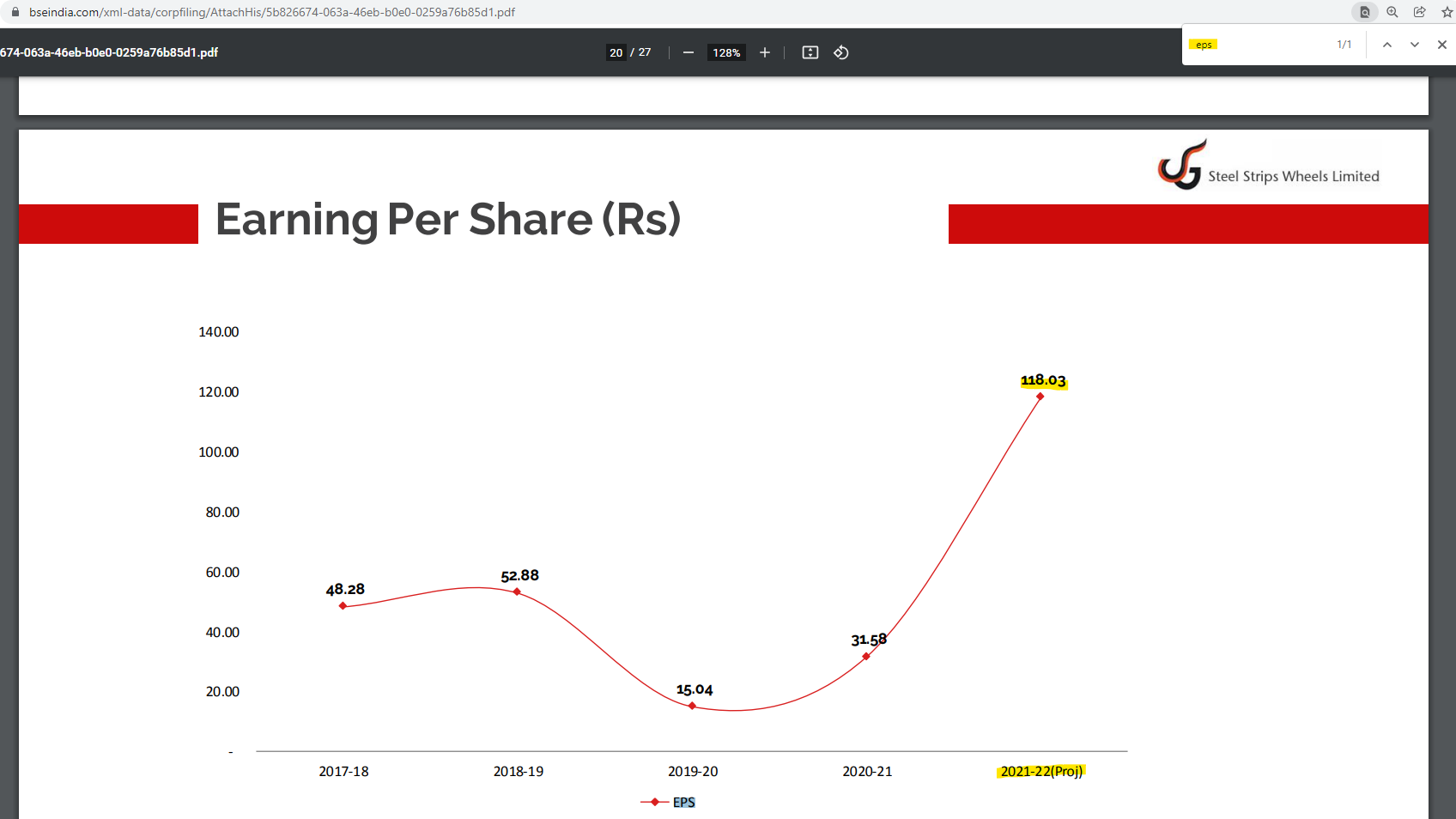

H1 EPS in FY 21 is 36 but they are guiding for FY EPS of 60 in their latest presentation.

Does it mean the margins will contract in H2 vs H1? Is it because of high raw material cost that the management is talking about from Oct to March?

FY22 EPS is 120, looks to me! ![]()

CY 2021-22 means FY22 ![]()

FY21 is in the past

Don’t see any other mention of ‘EPS’ in the latest presentation, cannot find the ‘60’ EPS figure here!

Screener shows TTM EPS as 60, so they project that much in next 6 months alone I guess!

Disc: invested

120 EPS is pre share bonus. After bonus shares the EPS is projected as 60

In H1 FY22 they have already done 36 so they are projecting just 24 for H2 FY22

FY22 is apr’21 to mar’22

I feel they will easily do 70+ this year as they have spoken about their ability to pass on the increase in RM prices. Anyway we will get to know roughly in next one month(Q3 result will come by then).

It’s a stock split not bonus.

Regards,

Raj

Disc: Invested.

They are targeting export for Topline Growth of :

1000+ crore export

Aluminum : 750-800 crore

Expect : 3,500-3,600 Crore of revenues for FY22.

Current Risk : Semi conductor

Raw Material no risk as mentioned by forum members.

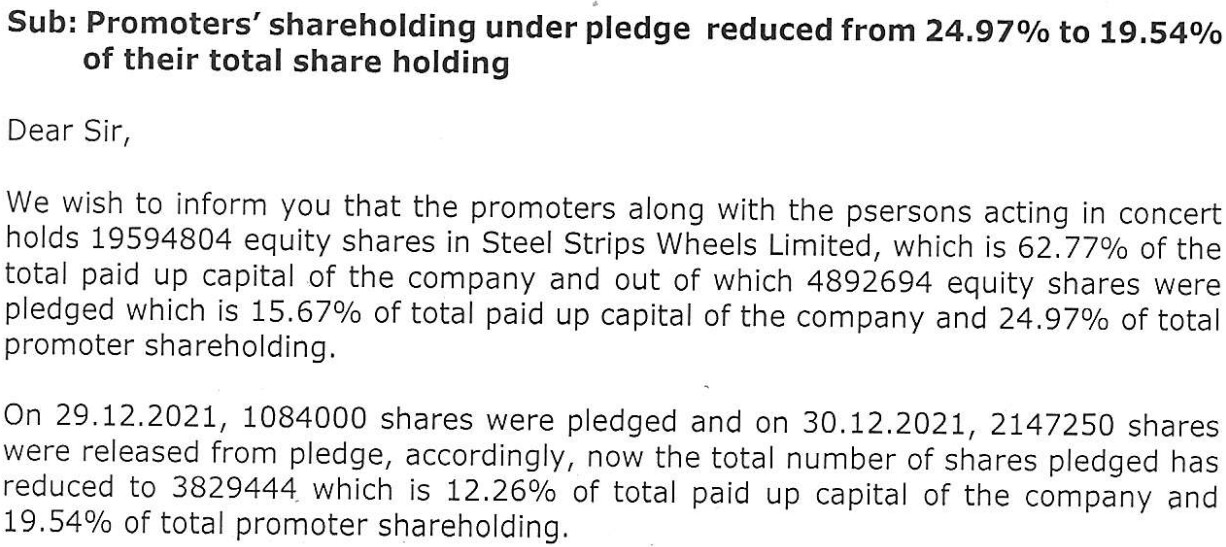

Management has reduced pledge by 16%

170 crore will be reduced

The contract are till March/April for the maximum Raw Material price (Fixed) and then they will renew the contract.

Disc : Exited (Found better opportunities) Expecting EPS to be around 70 with 1000 crore more sales…

Q3 Export was bit lower compared to Q2

Risks mentioned above i.e. semiconductor and RM pricing

Few developments in last one week.

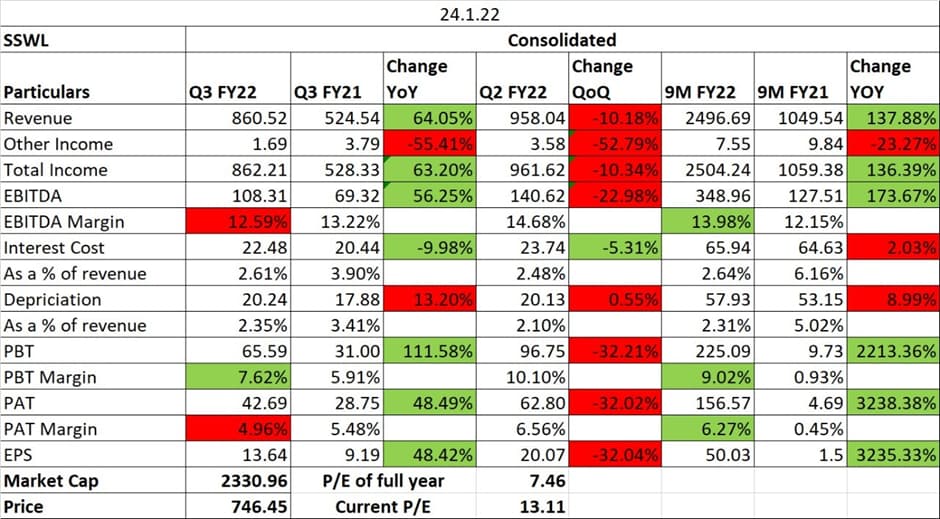

They have reported below than expected December sales numbers so sales for Q3 would be 850+ cr which is significantly up yoy but down qoq. Company in their presentation is guiding for 59rs EPS for FY22 which means only 25rs for H2, a significant decline versus H1.

Mostly the company will report lower margins both in Q3 and Q4 despite higher exports as raw material increases will be reflected in these two quarters. Important to see how much margin contraction happens.

They announced results date on 24th Jan and only after some time of announcement the stock locked in LC. So market is expecting significant margin compression in this quarter.

Stock is consolidating around 800 range for past 4-5 months and should come out of ASM framework in 1 weeks time. Personally at these valuations, I don’t see much downside risk but upside movement totally depends on margins that they will report.

Thanks

Investor presentation post Q3 - https://www.bseindia.com/xml-data/corpfiling/AttachLive/0cbc47f0-2256-4eb5-a2db-319dd109761b.pdf

@vikas_sinha , @fundoo and others, Even with poor than expected numbers the EPS projected is about 60. With that also, the valuation appears attractive given the massive spike in Export during current FY. And kind of cash flow company can offer in next few years? Am I missing something?

TTM EPS is already 65! So, yes the company is not promising anything great! The hope though is that they under-promise and over-deliver.

Company has started being more communicative, monthly updates etc., the presentations also show intent to increase their margins by export and alloys focus. I am kind of betting on rapid ramp-up of sales from the factory being acquired through NCLT. Auto sector is cyclical but more geographic diversity would help and the situation can only improve from here. Hopefully they are able to ride the steel price roller coaster though.

SSWL Q3FY22 Concall Notes -

Guidance -

FY23 Revenue 4200 - 4400 crs of which

Exports 1050 - 1100 crs

Alloy Wheels 1000 crs

Currently they don’t have any alloy wheels exports but in FY23 80 - 100 crs alloy exports expected.

Overall, 20-25% Volume Growth in FY23.

December sales slowdown due to holiday season in UK/Europe and Scheduled Maintenance by Auto companies.

January sales back to 300cr levels with CV and Alloy wheels taking the lead.

Added 5 customers on the CV side for Exports and 2 customers on the PV and trailer side for Exports.

Expanding Market Share in Exports.

AMW Autocomp acquisition in progress.

Couple of meetings done and expected NCLT approval in 4-5 months time.

AMW can add 600crs to topline

Acquisition funded through internal accruals and some debt.

Debt -

Term loan at 527 cr

Working Capital loan at 326 cr

Overall 853 cr

Repayment of 145cr in FY23 and 135cr in FY24 expected.

Pledge reduced to 19% so far.

Further plans to reduce to 15% in FY22 and eliminate it in 2 years.

Utilisation levels -

80% Dopar Plant

81% Chennai

64% Chennai Truck Plant

64% Jamshed Plant

70% Mehsana Plant (Alloy wheels)

Management says Capacity can be expanded through debottlenecking and brownfield as land is available at plants and the AMW acquisition is also there. Expects 95-105% utilisation levels at 4200 - 4400 cr revenue.

Margins -

Since the raw material is complete pass through, margins are skewed as raw material as a % of product price is taking a larger share than their usual prices but still holding well due to better product mix (alloy wheels)

Alloy Wheels have 17-19% margins

Overall margin will move upwards as Raw Material price subsides over time.

Market outlook -

Seeing a trend in more SUVs/MUVs being bought in which people prefer Alloy wheels due to better looks and fuel efficiency due to lighter weight.

Currenly Maruti is not taking alloy wheels from SSWL but there is a discussion going on.

SSWL expects its market share in PV alloy wheels to be 35-40%.

Seeing upcyle in CV and says will surpass 2018 sales levels due to the upcycle.

(Evident in January sales note, Highest ever CV sales)

No lag in passing RM cost so no RM risk.

Yearly maintenance capex is 30 - 40 crs.

Currently at TTM PE of 12.5

Thanks for the notes. Do you have the link to the concall. Could not find it anywhere

Just to add to this - Management clarified that even though the annual EPS for current FY is projected at 59; the actual EPS for FY22 should be better than that.

Some questions:

Any details on robot introduction?

Any idea on margins in exports vs domestic? (I know exports is higher but the number?)

They already have high market share so growth would have to come from market expanding right? There is limited scope for capturing much more market share (at least in domestic)?

Disc- no holdings as of now but tracking closely

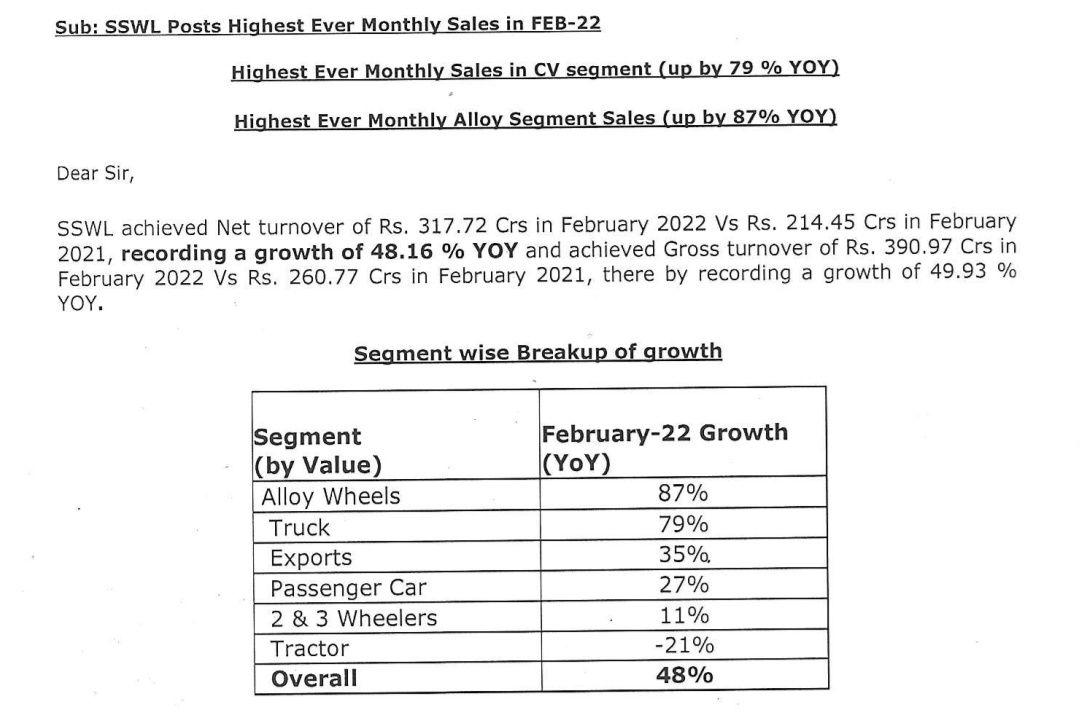

Highest Ever Monthly Sales for SSWL.

Highest Ever Monthly Sales in CV segment (up by 79 % YOY)

Highest Ever Monthly Alloy Segment Sales (up by 87% YOY)

SSWL achieved Net turnover of Rs. 317.72 Crs in February 2022 Vs Rs. 214.45 Crs in February 2021 recording a growth of 48.16 % YOY.

Gross turnover of Rs. 390.97 Crs in February 2022 Vs Rs. 260.77 Crs in February 2021, there by recording a growth of 49.93 % YOY.

They are targeting Exports in both steel and alloy segments so thats a whole new market to grab.

On domestic, Alloy is seeing a good market size expansion due to Alloy wheels being preferred in SUVs and their better looks and weight (good for fuel efficiency)

EVs should also go for alloy wheels as EVs are supposed to be as light as possible to make space for battery packs and reduce dead weight for better power efficiency.

Also Maruti is not a alloy wheels client for SSWL so if they onboard them (discussion ongoing as per latest concall) that opens up a good market size for them as Maruti is a leader and has good offerings.

CV upcycle is also there for short-medium term.