Stock starts reacting - great…One good thing which we can see is company has started penetrating into after market segment. It got couple of orders from Korea, Egypt and Europe. Enkei wheels has good hold on after market in India as far as I know. It would be great if SSWL has started into after market in India as well. Can anyone do some scuttlebut. Trying to do myself also.

Steel is a raw material for SSWL. Given steel prices have plunged over last few years, operating margin for SSWL have remained same ~9.5% during last 4 years (https://www.screener.in/company/SSWL/). Are there any raw material sourcing contracts which protect SSWL from steel price fluctuations?

Given rising exports from SSWL, it would be good to find out if there are any Chinese competitors. Assuming steel prices continue their downward spiral and Indian govt imposing anti-dumping duty to protect domestic players, Chinese competitors will be able to source raw material cheaply. So in case they are able to produce same quality, then can put pressure on SSWL.

@ashish_trader,

Collaboration with Tata Steel & Sumitomo will work in-favour of SSWL w.r.t mitigation of increase in raw material.

SSWL recently own good orders from Mahindra, Kubota etc…

Commissioned State of the Art wider Hot rolled Coils Slitting Line. Similarly some outsourcing activity will be replaced with inline work by January.

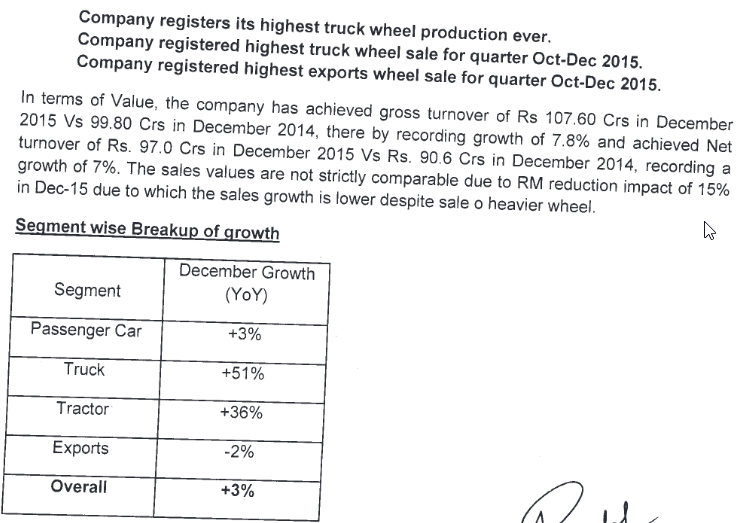

Similarly SSWL reported highest exports,production selling in December…seems to be everything going good for now.

I recently heard a management call wherein they stated the exact opposite. It is because they have been sourcing from Tata Steel, they are not getting the benefit of fall in steel price. They have been sourcing from Posco due to this and hope that Tata Steel will pass on the fall in steel price in future.

The rise in exports is an encouraging factor. The company intends to cut debt by 53 cr annually for next 2 years. So overall I am positive on the company.

Could you please also let me know why did they go for allocating pref equity to Halink for that new alloy wheel plant in Gujarat which the company expects to be operational by Mar 17. Are there any caveats with that deal which may harm company in the future?

Regards

Ashish

Disc - Not invested, but looking to create a position soon

No issues here. Kalnik is a Korean company known for its technological intelligence in alloy wheel making. SSWL has rich experience about the Indian auto sector and Kalnik has rich technical expertise. If Kalnik took shares from open market (which easily it can) - it wouldnt get mgmt control (BOD control). Kalnik wanted to do business in India and joined hands with SSWL. Thus by getting shares allotted at 640 - Kalnik will get the mgmt control also. We can say 640 is the true value of the company stock - correct me if I am wrong.

I was worried about this stock to be a quality trap - good quality business run by great people - but no growth (or less growth).

But, the initiatives taken by the mgmt proves my thinking wrong. I think we should give the stock some few quarters - downside is limited and upside potential is very high. Alloy wheel plant and exports will increase topline and backward integration and cost efficiency will boost bottomline. If company enters the domestic aftermarket like wheels India and other competitors - it can be a game changer altogether.

Was going through the AR of Enkei wheels and Wheels India limited.

Wheels India is not only into wheels - it is into air suspension, heavy engineering, etc. In their AR they have clearly written that their business has shown little growth in wheels segment due to heavy demand for alloy wheels - since aluminium alloy wheels look attractive. They are not going for any capacity expansion this year.

Enkei wheels is purely into wheels and that to only alloy wheels - its major clients are maruti suzuki, honda, etc. It is overvalued (trading at 55 +PE). No expansion on cards.

SSWL purely a steel wheel player - now will start into alloy wheels as well and trading at cheap valuations.

Steel wheels are good in quality, whereas alloy wheels are light and attractive. It is not that the demand is getting shifted from steel to alloy wheels - since Landrover Jaguar even today buys steel wheels from SSWL (BSE announcements). Alloy market is increasing at 18-20% CAGR and SSWL is taking right steps to serve the market.

Q on Q comparison, in my outlook, is for Finance and IT cos only…not for manufacturing cos, like SSWL. Y on Y if they do ok, it is fine. I think, lower raw material cost will continue to add to profits but some savings may have to be passed on to OEM purchasers as well and hence top line growth might still be low. That is where the new Alloy wheel plant will do wonders

PS - invested

yes you are correct that Q on Q is not that important here. Company did pass on some of the benefit to the OEMs which might have led the sales growth to just 5.63% y on y. I feel management is little bit conservative - where enkei wheels is already there in the business of alloy wheels, SSWL is still not there. Opposite also apply to enkei wheels - they are not in steel wheels. The crux lies is that the alloy wheels demand is increasing at 18% CAGR and steel wheels demand is growing at much less rate.

Couple of big ticket expense items have grown disproportionate to business growth of 22% CAGR over last 5 yrs. Store Spares have gone up 44% CAGR and Employee expenses at 33% CAGR. Disproportionate Store spares growth has only halted in FY15 while Employee expense growth continues. This is not a sign of healthy operations.

Results came out before market close. Looks very decent and roughly on the lines of monthly increases in sales. There was a bit of drama, when an earlier date was announced for results declaration and they pulled out in the last minute (http://www.moneycontrol.com/stocks/stock_market/corp_notices.php?autono=3891621) ;

but looks, all is well now. With a possible Annual EPS of around 50, one can gauge where this goes. The trigger will continue to be the alloy wheel plant and that can put this in a different league

Also, order flow like this, although of small value, keeps the lock for a longer term trend. In my limited time with this stock, I had seen that they bag small value orders that have to be executed over long period of time and to me, that is spreading the risk, over time. Hopefully, any raw material price change that may affect the dynamics as well is contained by inclusion of suitable clauses…

If that been the case why their net turnover is down by 6% on yoy basis for 2016 Q1? As from the statement I have understood that 20% RM drop has caused this issue but in that case are they not passing on this loss to their customer ?