Hello All,

This my second post on this forum.

Disclosure : Not a recommendation to buy or sell.

Just a deep dive into analysis of a stock whose valuation is not par with the peers in sector

Star Paper Mills

Part of Duncans Industries Limited

Background of the group : The Duncan Goenka Group (DPG) is one of the oldest business houses in India with a diversified product portfolio of Tea, FMCG, Engineering, Paper, Synthetic Fibers, Chemicals and Polymers.

The Chairman of Duncan Group of Industries., Mr. G. P. Goenka is a Member of Board of Governors of Indian Institute of Management Calcutta. He’s also the younger brother of RP Goenka

Srivardhan Goenka is the one currently managing the company (Son of GP Goenka).

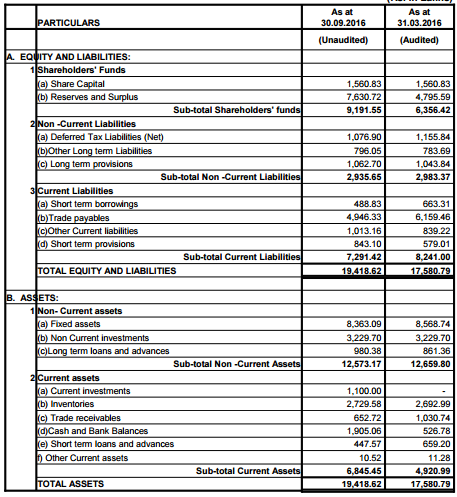

Since last few years after son’s take over there have been lot of positive developments . Please check below balance sheet and income statement for last five years

Debt Reduces

-Long term debt hardly 7-8 crores (which was 20 crores couple of years back)

-Other Liabilities (Deferred Tax, Provision, Trade Payables and Other Current Liabilities) -reduced to 86 crores (for which there is no interest payments so finance cost has reduced terribly)

-Short term borrowings 5 crores

Interest expenses are reduced due to debt reduction and its becoming virtually debt free

Earnings

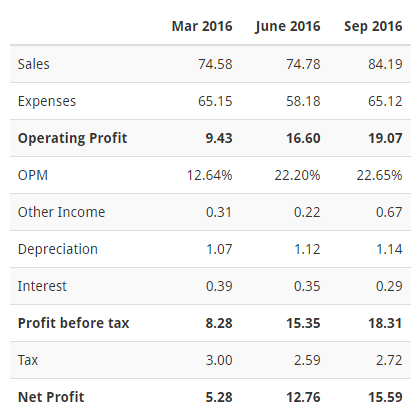

Operating Margins above 20%

EPS of 18 rs for the first six months ending Sep 2016

Stock has run up a lot in last one year (5 times)

Negative Parts

Pledging of Promoters

Contingent Liabilities of 15 crores approx

Please let me know if anyone is tracking this company and has any information

Disclosure : Holding less than 5% of total portfolio

Nice analysis @paresh.sarjani1.

Just looking the numbers I have few questions

1- Do you know why there is a reduction in reserves?

Looks like the management has turned around the company and lot of that turnaround is already captured in the prices which rose from 34 (Jan 2016 end) to 180 today ( 29 Jan 2017). It looks cheap considering TTM PAT, but a lot has been already captured in the stock price.

@paragbharambe

i think that’s quiet evident from earnings. All net losses of those period have been counted . You can clearly see the increasing trend in reserves in last two years and six months ended sep 2017

Big question - Can they increase their topline from here? 22% margins for the year (q3 / q4) are discounted at these valuations imho, If they can increase their topline or have some capex plan, this can still go more from here.

With cyclicals, one needs to be very cautious to book profits at regular intervals. Can not point an opportune time, but seeing last 2 qtrs (Margins around 22%), market has priced in these sort of margins for next 2 qtrs as well.

What are the utilisation percentage they are operating at currently?

Paper companies are cyclical in nature… We are in very advanced stage of paper cycle… It’s better to invest when some corrections happen…

I have been in paper industry and maintaining 22 % margin is difficult…

how do we track paper cycle? also shutting down of couple of plants by Ballarpur has changed the supply demand equation for the short term (till they are back) - do you see this playing a factor or no?

The current business cycle in paper is not a typical cycle which is driven by excess capacity, then demand reaching capacity and consequent product price rise, new capex & so on.

This cycle is partly due to temporary shut down of BILT and consequent capacity reduction - similar to what is happening in dyes & intermediates where china capacity shutdown led to product price increase. however, paper prices havent spike up, only risen somewhat. There are other supporting factors like variable cost reduction.

The cleanest way to play the space, since the translation of gross margins to bottomline isnt encumbered by an onerous interest burden. Would also like to mention that the current uptick in paper company fortunes is not solely driven by capacity reduction as has been widely disseminated in the press but also due to the considerable reduction in raw material prices vis-a-vis 2 years ago.

As for star paper, applying an industry average multiple to trailing earnings would likely yield a target of 30% in excess of the current price. Also boasts the highest ROE in the sector.

Discl: Invested and continuing to add

one small question if the experts can answer, why is this still quoting a single digit multiple whereas its peers with average fundamentals are already in double digits?, i dont think its priced in…the latest Goenka interview gave a good insight. ROE is at 30, ROCE is at 54/55( acc to my cal, i maybe wrong).

Discl: Invested at current price and now waiting for q3!

Bro, cyclicals don’t command high p/e. In fact, such stocks should be bought when there is no hope (noone is willing to buy) at bottom, and should be sold when everyone is buying (everyone is expecting bumper gains).

Please note that there is a limit at which it can grow. Do you know at what capacity utilization they are operating currently? Can they improve their topline from here (qoq)? Margins are 22-23% and that’s fine, but can these margins be maintained going forward? I don’t see re-rating from here unless raw material prices nosedive (especially because this rally is fueled by reduction in capacity due to some plants getting offline). Risk reward isn’t favorable at this price imho.

It looks cheap, yes if you see p/e valuation, but cyclicals never command higher p/e unless there is good visibility, which i see lacking here. Momentum can take stock price to higher levels, but timing cyclicals is very difficult. If you are stuck at top, you are not going to get back your price in many many years. So, be cautious.

Indian paper industry at present is growing at 8 to 9% annually.I firmly think we shouldn’t underestimate this sector.

Indian paper demand is set to rise by 53% by 2020.Growing consumerism, modern retailing, rising literacy (continued government spending on education and the increasing use of documentation will keep demand for writing and printing paper.Though India’s per capita consumption is quite low compared to global peers, things are looking up and demand is set to rise from the current 13 million tonnes (mt) to an estimated 20 mt by 2020.An India Ratings report estimates India’s per capita paper consumption at nine kg, against 22 kg in Indonesia, 25 kg in Malaysia and 42 kg in China. The global average stands at 58 kg.

After doing some research i feel it has very good potential to grow.From a demand point of view, every one kg incremental per capita consumption results in additional demand of more than one mt a year.

The two sectors projected to grow the most are packaging and published printing.Within packaging printing, the fastest growing sub-sectors are label and tag printing.India has climbed from the eighth largest market in 2011 to fifth in 2016 of the print packaging industry

The print machinery production registered a year-on-year growth of 20% in the last few years.

PRC India 2017: Trending upward, was held in mumbai feb 7,2017

An array of factors is causing paper consumption, production and recycling activity to rise in India. http://www.recyclingtodayglobal.com/article/paper-recycling-india-opening-session/