I think the primary reason is valuation. On 10th October, it was trading at 45 times PE multiple. Now the valuation is is in more reasonable 27-28 times. That is not to say that it cannot fall further. In general FMCG space is falling a bit more than market. Many of the more established players in FMCG market has fallen quite a bit, much more than index. In such a market micro caps stocks do fall more.

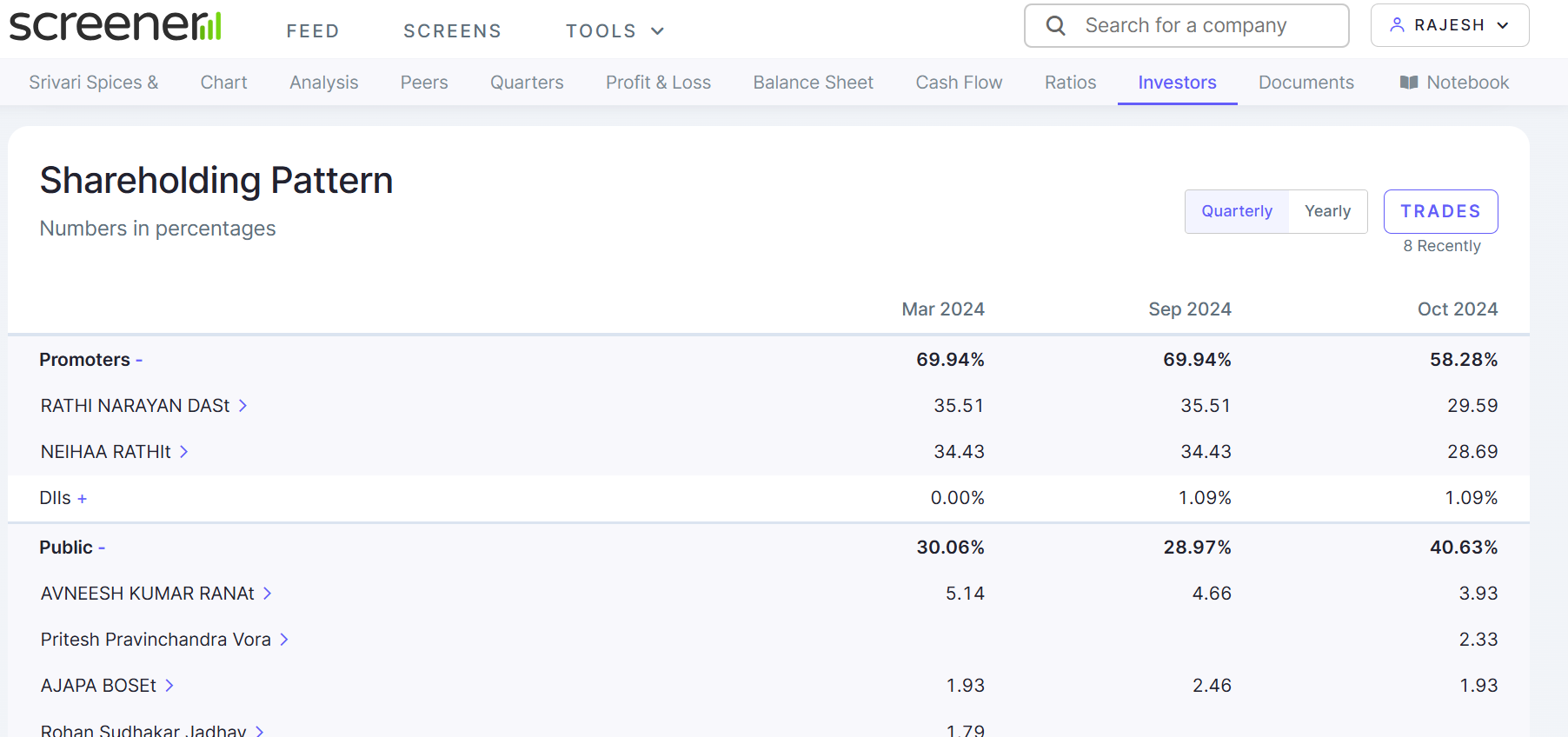

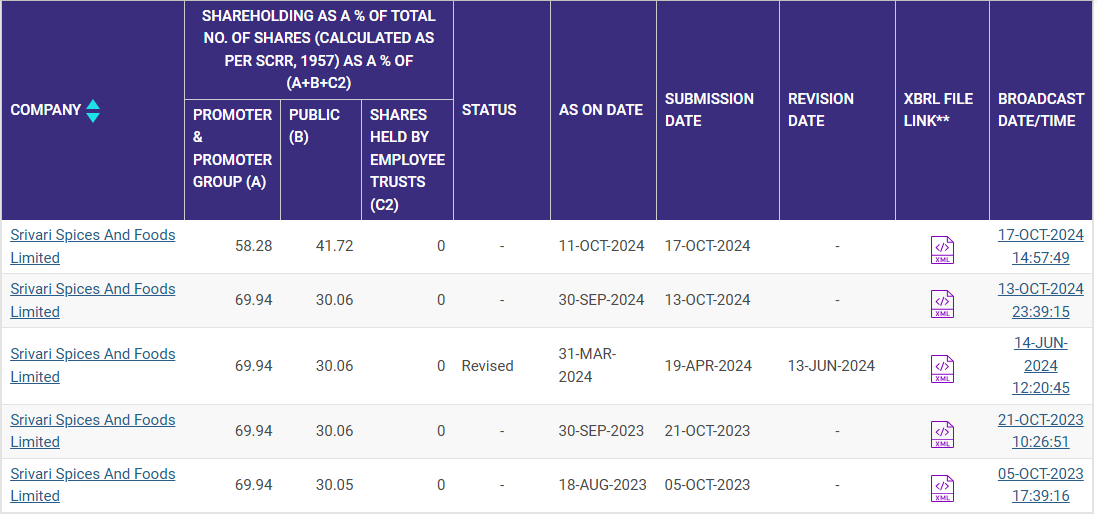

Looking at the company, there is no negative news about the company; however even the positives are missing. There has been no announcements about entry into oil and other products they planned. Further, the shareholding of management has come down in October fling, from 69.94% to 58.28%. Further, shareholding of one Avneesh Rana has gone down.

There is no news of promoters selling anything in market or any notice on exchanges. I think promoters should explain this.

On positive side, the company is expected to do well in H1. Further, the company has received around 25 Crores in rights issue. It should give financial strength to the company to grow at the projected rate. Even the management participated fully in the rights issue at Rs. 175 per share, as declared by management earlier. Thus, things are not looking that bad.

Yes, as an investor we don’t know everything, we cant know everything. Investing is all about taking bets in uncertain future.

Thanks for the insights.

Its a bit strange that the promoter holding has significantly changed and I can’t find any disclosures regarding this as to when and why did it happen.

The promotor Sold nearly 11% of shares and its Rights in the market and applied rights more than his share percentage. Even though it is fully subscribed only 30 to 40 % participated in the rights that means if applied for triple the quantity the possible of getting all is high. So the promotor i assume without liquidation sold part of his shares and participated in rights and gained most . Fair or unfair it is permissible with in rule book and all 25 cr of rights money going to invest in new oil production unit hence good future on the cards.

Disc: Holding good quantities and my views may be baised

The message to shareholder is to be on alert as the promoter can reduce their shareholding anytime if they forget about this company. Also pay to have your shareholding intact, the next we come with a rights issue. We will even crash the share price to take over your portion .

Unfair practice but within rule book. I do not thing promoter have any thing to do with the crash of share price .But now we have to look what is the future plan of the company to judge the worthiness.

This much of fall happen due to any reason, somebody knows better than retailers and promotors shareholding getting down is giving more doubt over this company now. Please be safe… information come to retail when share goes down by 70-80%

Undoubtably the share price has fallen by more than 50 percent in last few months, and there may be some message market is giving we are not able to understand. Nevertheless, the fall is after a rise of 10 times in a very short span of time, from around INR 40 IPO price to more than 400 in around 6 months. Sharp falls do occur after sharp rise in any stock. We can find many stocks in the market, even in high Mcap category which has fallen by 50 percent in the same time. It doesn’t mean that something is drastically wrong, though it is possible.

Let us take a fresh look;

The company did 80 Crores topline with good margin last year. The company is growing at a very high rate for last 3-4 years.

Management has guided 100 percent growth rate for next couple of years. Let us presume it can grow at @ 50 percent.

As the topline is increasing at fast pace, working capital requirement goes up. This, cash flow from operating activity is likely to be negative.

Management has subscribed rights at Rs. 175 per share. Many retail investors didn’t apply, and still the issue was fully subscribed. Looks like management or large shareholders applied for more.

Even at 50 percent growth, the company is likely to report a topline of 120 crores, with 10 crores of net profit; eps of around 12.

Thus at today’s price, the stock is available at 18 times current year earning. For a company growing @ 50 percent, the stocks look not stretched.

Thus the stock is reaching a level where value investors will start finding something, if nothing is fundamentally wrong with the company. Let us see what happens.

As per records the management neither participated in rights nor sold RE and their total share remains same around 50 Lakhs. Due to non participation of rights their percentage is reduced accordingly. So the management hand is clean and they are going to use rights money for

New oil manufacturing unit costing 10 cr

Reducing Debt

10 Cr for working capital .

Now they have tie up Big basket and D mart. Retailers including HNI bought all the rights and some game going on for accumulation. In couple of quarters due to low equity if the business goes well as per plan the price will surge .

Srivari has come out with decent results, growing over 60 percent on corresponding half year last year. Margin is maintained. Nevertheless, growth over H2-2024 has been subdued- around 10%.

However, cash flow statement looks good. Receivable and inventory is under control, leading to positive cash flow from operating activity.

Company has 16.73 crs of short term debt on the balance sheet. This is very concerning. If the money from rights issue is used for growth and not to service this debt and there are any mishaps in the receivables, company can be in a lot of trouble.

As mentioned above, it is due to right issues and promoter has not participated in the same nor they have sold any share. So promoter shareholding has decrease by 20%.

What should be more concerning to all the people here is how can an FMCG company with Rs. 100 cr of reported revenue on TTM basis have only 20 employees.