The Company:

Incorporated in 2019, Srivari Spices and Foods Limited is engaged in the business of manufacturing and marketing spices and flour (chakki atta) across Andhra Pradesh and Telangana. In August 2023, the company came out with IPO at Rs.42 per share. Total equity of the company is 7.14 crores. Promoters hold 69.9% of shares.

At current market price of around 225, the company is commanding a market capitalization of around 160 crores.

Narayan Das Rathi (Presently MD) is a serial entrepreneur and a visionary, who dreamt of taking spices, foods, and sharbati and regular atta to the discerning Indian consumer. The company claims to have a single-minded focus on QUALITY, and on providing the purest most authentic ingredients to customer’s kitchens. From their website [https://srivarispices.com/], it appears that the company is focussing on quality.

Financials:

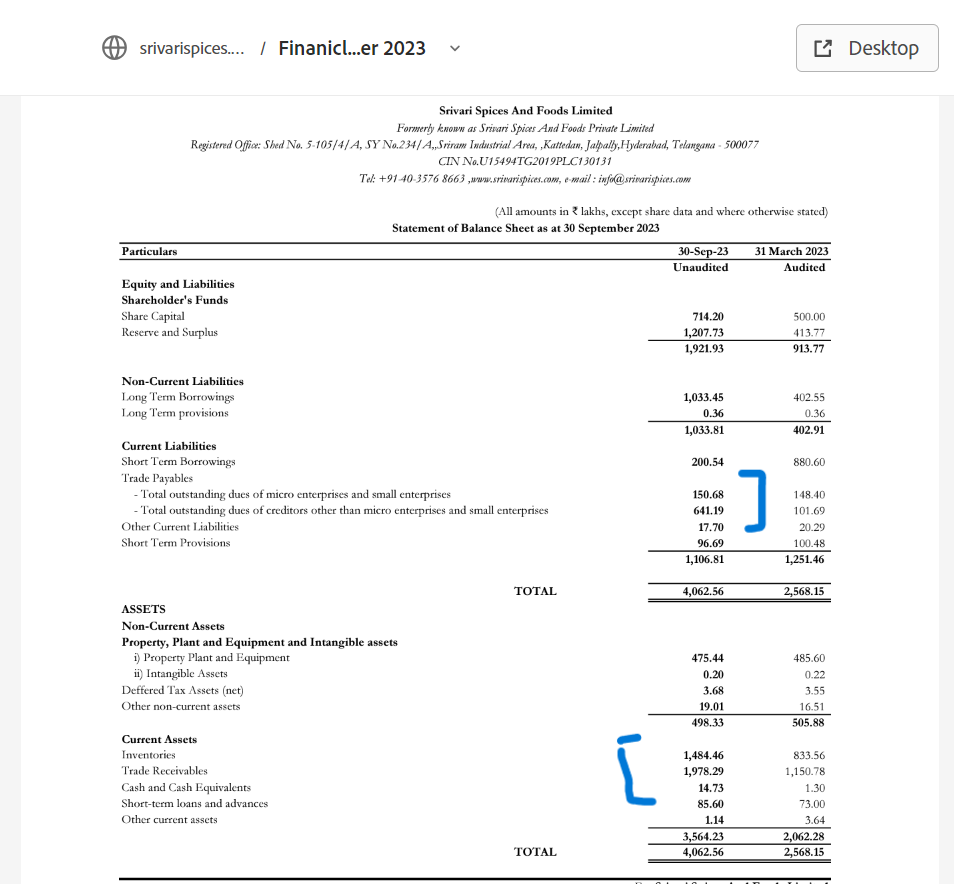

The company has been incorporated only in 2019, and hence financials for a long period is not available.

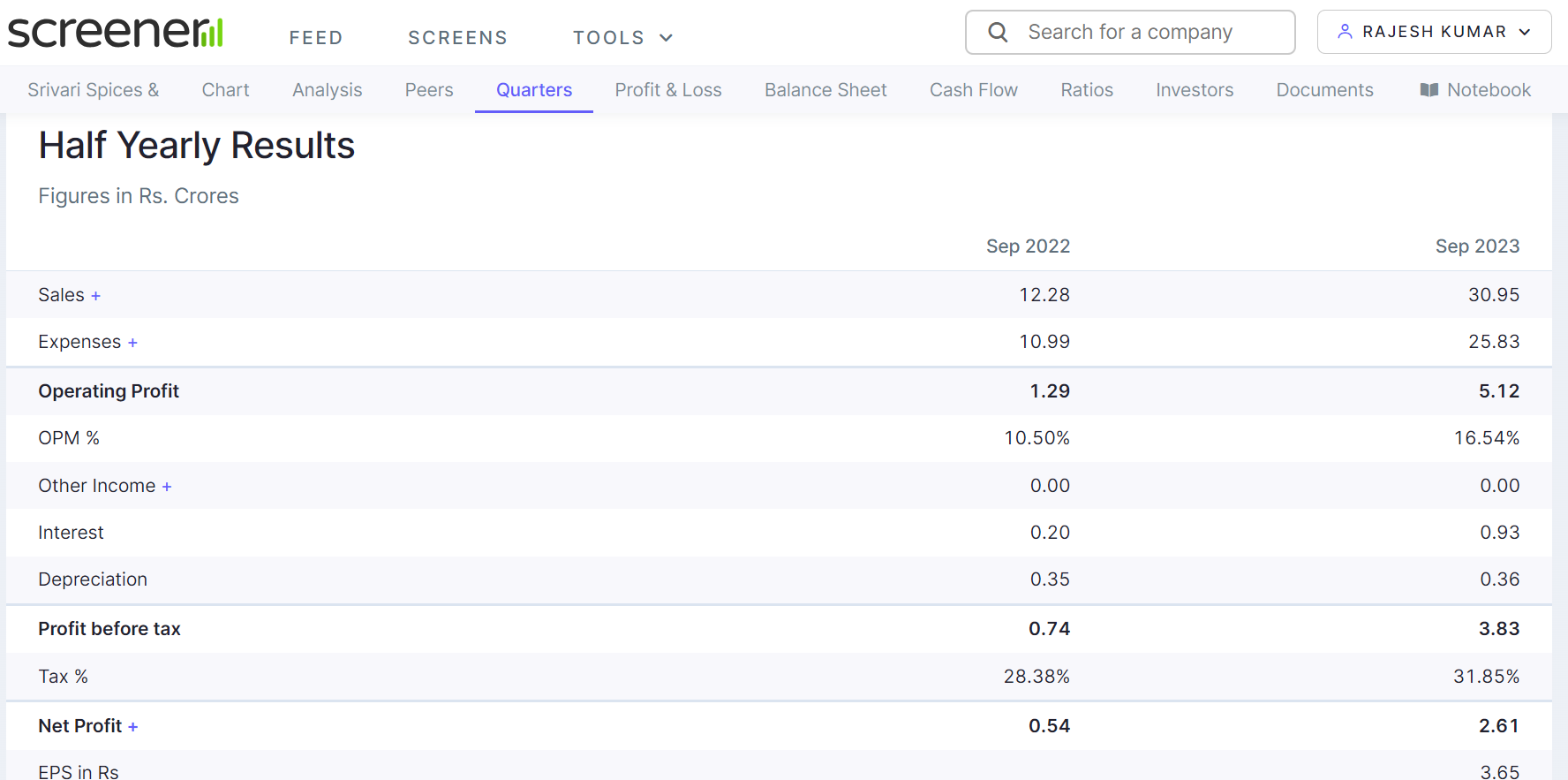

On a half yearly basis, the company has shown 30 crores topline and 2.6 crores PAT in H1- 2024.

The management has said that they are running Rs.8 crores revenue presently. They are operating on 26% to 27% of the gross margin overall. Thus, we can expect a topline of 50 Crores and PAT of around 4.5 crores in H2-2024 by extrapolating the numbers. Thus, I expect an eps of Rs. 10 in the current financial year.

Business:

The company has two manufacturing locations in Shad Nagar and Katedan in Telangana. These are state-of-art plants which manufacture spices, masalas and sharbati and regular atta.

The manufacturing plant, made by Choyal, in Shadnagar, manufacturers over 3 tonnes of sharbati and regular atta every day. The freshly ground atta is then packed and sent to over 15000 retail outlets across Telangana and Andhra Pradesh. The plant at Katedan manufactures spices and masalas. It has a capacity to produce over 3 tonnes of spices and masalas every day.

It looks like atta, spices and masala are commodity business; but in the present scenario a slice of population is willing and capable of paying premium prices for purity and quality. It looks like the company is tapping in that market. All communication from the company is insisting on quality and purity, including procurement of raw materials only from accredited farmers.

Future Plans:

In the latest investor meet the company has said that they are coming out with the new 15 masalas which are into the pipeline which are delayed because of our penetration into atta was very high. They are also planning to come out with pure safflower oil as well as groundnut oil. The are planning a unit for it, and they expect to launch the product by June this year. They are also eyeing export market. In the oil segment, they are expecting a gross margin of 15-18%.

The company plan to concentrate on Telangana and Andhra market only. It said,

“We are only in Andhra and Telangana and next financial year we will be focused on Andhra and Telangana only with the potential of the product and the category is very high. So, apart from going to geographic expansion, it’s better to focus on our current market, which will help easily to penetrate the market as well as maintain the profitability. If we make an expansion in other states too fast it will affect our profit margin also. So, we want to first capture the market here and we want to be in the top three numbers, then we will open the new location…… We will not focus on the other geographical area expansion in other states. So, we have huge potential in Andhra, Telangana itself. So, you can see after 400 crores to 500 crores of revenue we will think about the next stage for the geographical expansions.”

The management further says-

“By 2030, we will be the best company in India, we are giving the healthy product out of all the other with quality check as well as you can check the lab reports. Today also all the parameters if you check we are the best in the industry throughout India, if you compare with all the national brands we are above all the national brands of Tata or Aashirvaad and other MDH, MTR, we are maintaining the high quality, we are focused on the healthy product line as well as quality product. So, this is our objective to make. By 2030 our brand will be there. It’s too early about the next first, two years, three years. We are coming out with a lot of products in the pipeline. We have planned almost 300 products to launch overall into the next till 2030.”

New Initiative:

They are increasing the dealer’s network- from 15k dealers to 50k dealers. Further, they are also starting to distribute the product on EVs, which will gibe better visibility to the company and brand. Their direct to customer initiative will result in lower working capital requirement and better margin for the company.

A copy of the investor meet is enclosed herewith.

SSFL.pdf (923.8 KB)

Investment Thesis:

- A food company, growing at a very high pace is available at a reasonable valuation [22.5 times current year eps], or 2 times current year sales.

-Taste of Indian consumer is changing and some consumers are willing to pay higher price for purity and quality.

-Growth story looks promising based on past performance of the company.

-First generation entrepreneur [my personal preference is first generation entrepreneurs].

-Sensible strategies like sticking to small area, expanding the portfolio, maintenance of margins etc.

Risk:

-Micro cap stocks are risky by nature and one can lose 100% of invested capital.

-Company has already seen sharp upside and deep correction cannot be rules out.

-The company has very ambitious growth plans, and will need huge capital outlays for financing such growth.

-Cash flow of the company is negative.

[Disclosure- Invested]