Disc: Very small quantity bought recently for tracking purpose . My concern is on the revenue front , where the sales growth has been a bit subdued , however due to the recent capex and increased capacity it can deliver goods . Also to note the company is currently operating at 100% capacity in the DI Pipes segment .

While doing a search on the google for competitors , 2 big names which came up , where Tata Metallics and Jindal Saw . Tata Metallicsi is operating at half the capacity of SRI and Jindal saw has a huge capacity , however is debt loaded . I guess jindal steel was in news recently for not able to pay their dues , etc . However the analysis is incomplete and requires more digging .

Please note i am not an expert , just started learning .

On Valuation front, still unable to figure out the reason behind 7x TTM earnings compared to its competitor like Tata Metalliks quoting @14 PE.

I suppose the debt-ridden Electrosteel management at the helm could be the possible reason behind such low valuation given by the market for quite long time. Company also take its own sweet time to report their quarterly earnings which failed to gain investors’ trust.

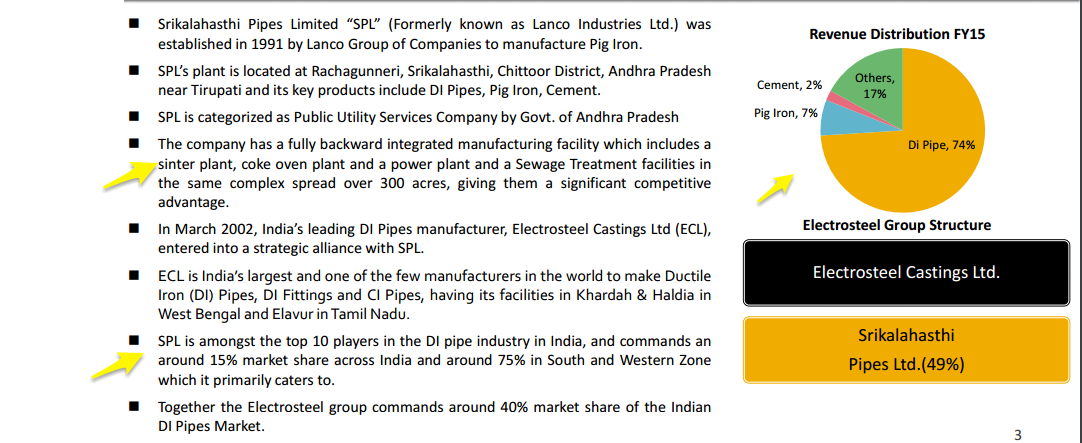

Having said that, Growth, the only hope/further trigger for the rerating of multiples and execution stands the key here considering the company commands >70% market share in southern & western India in DI pipes.

Expect Q2 results to look bad as a furnace was closed for a month for maintenance, this will increase capacity of DI pipes post maintenance. May be a good time to buy fresh if it falls further.

I had invested in it long time back, that time quarterly results were more than 100% up and stock tanked…Reason - mgmt decided to buy Hyderabad property of debt ridden Electrosteel at astonishing valuation… basically earnings of sripipes diverted to electrosteel… i eventually sold at loss… that explains lower valuation compared to its peers

Hi @sushildarveshi

Can you please share the link of the article which talks about purchase of Hyderabad property…I was assuming the low valuation was because of ESL Ltd loss carried forward to ECL and as a group, sentiment the valuations are low…

The capacity is being increased from 2.25L MTA to 3L MTA and SPL already operates at full capacity. The capacity expansion is from internal accruals and Debt is also coming down.

Since the Banks are discussing to sell ESL and if sold , ECL and SPL will be rerated and valuation will expand.

Till now i thought the money is not flowing from SPL to ECL. This Hyderabad property purchase is surprising.

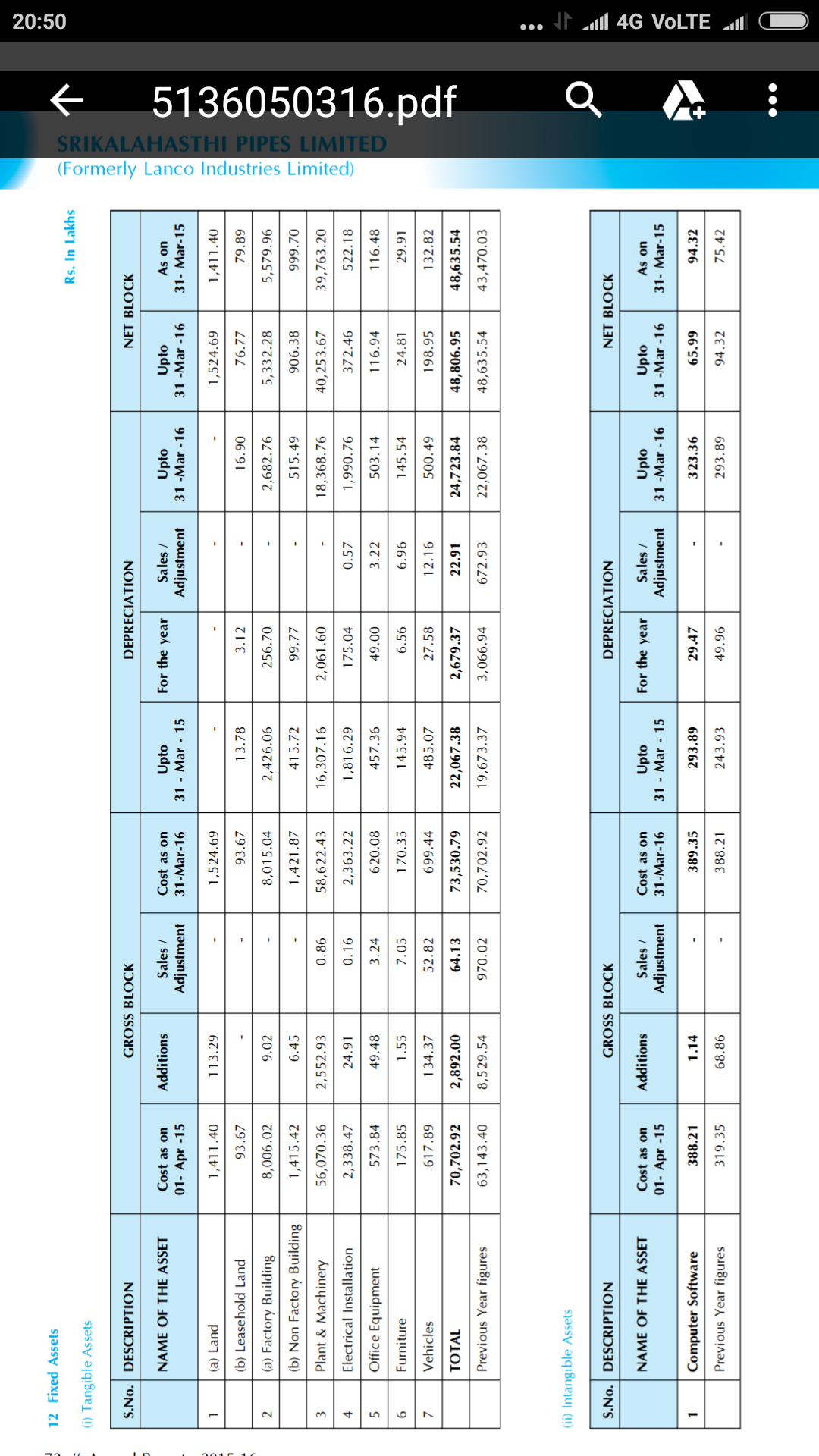

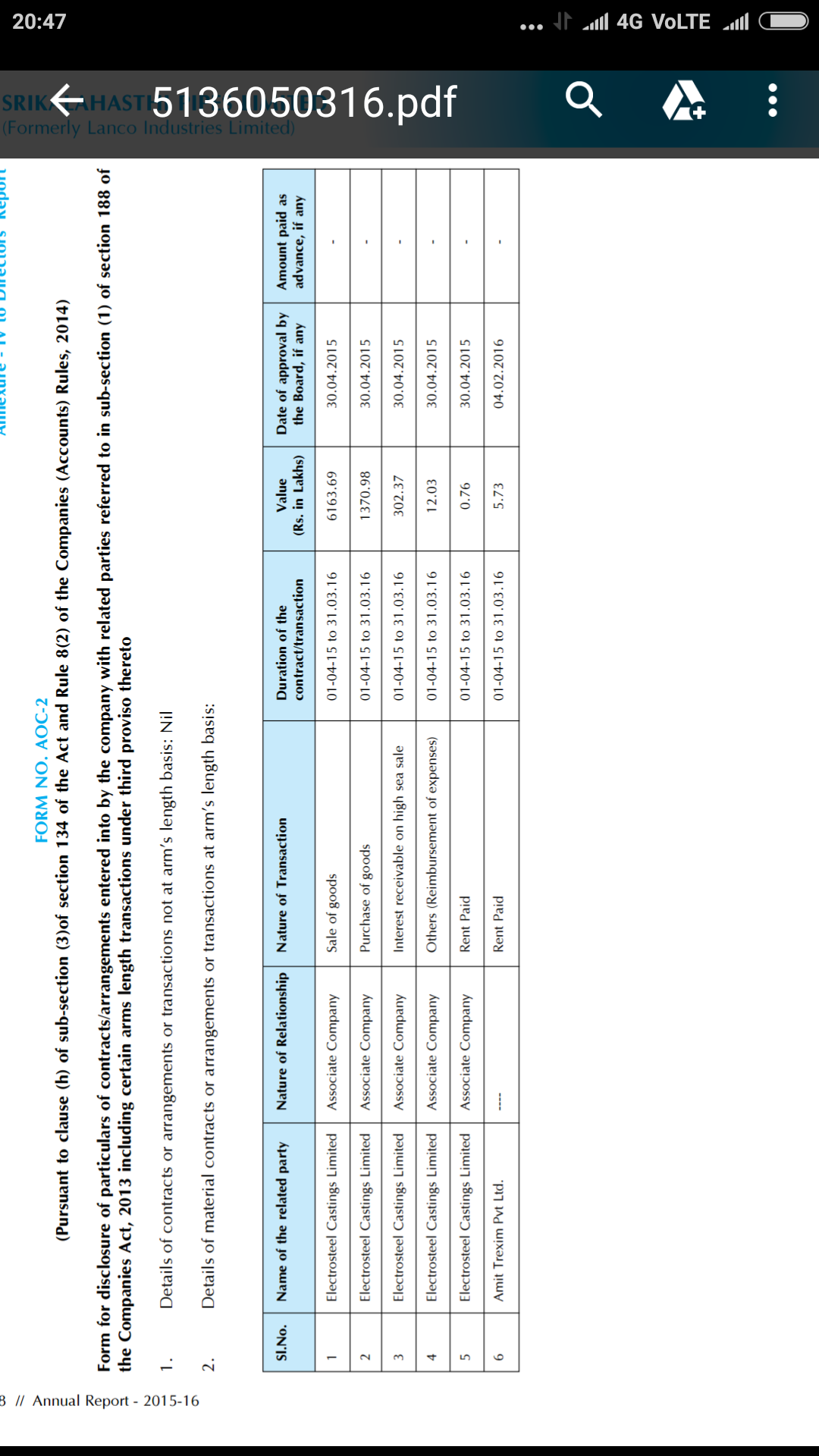

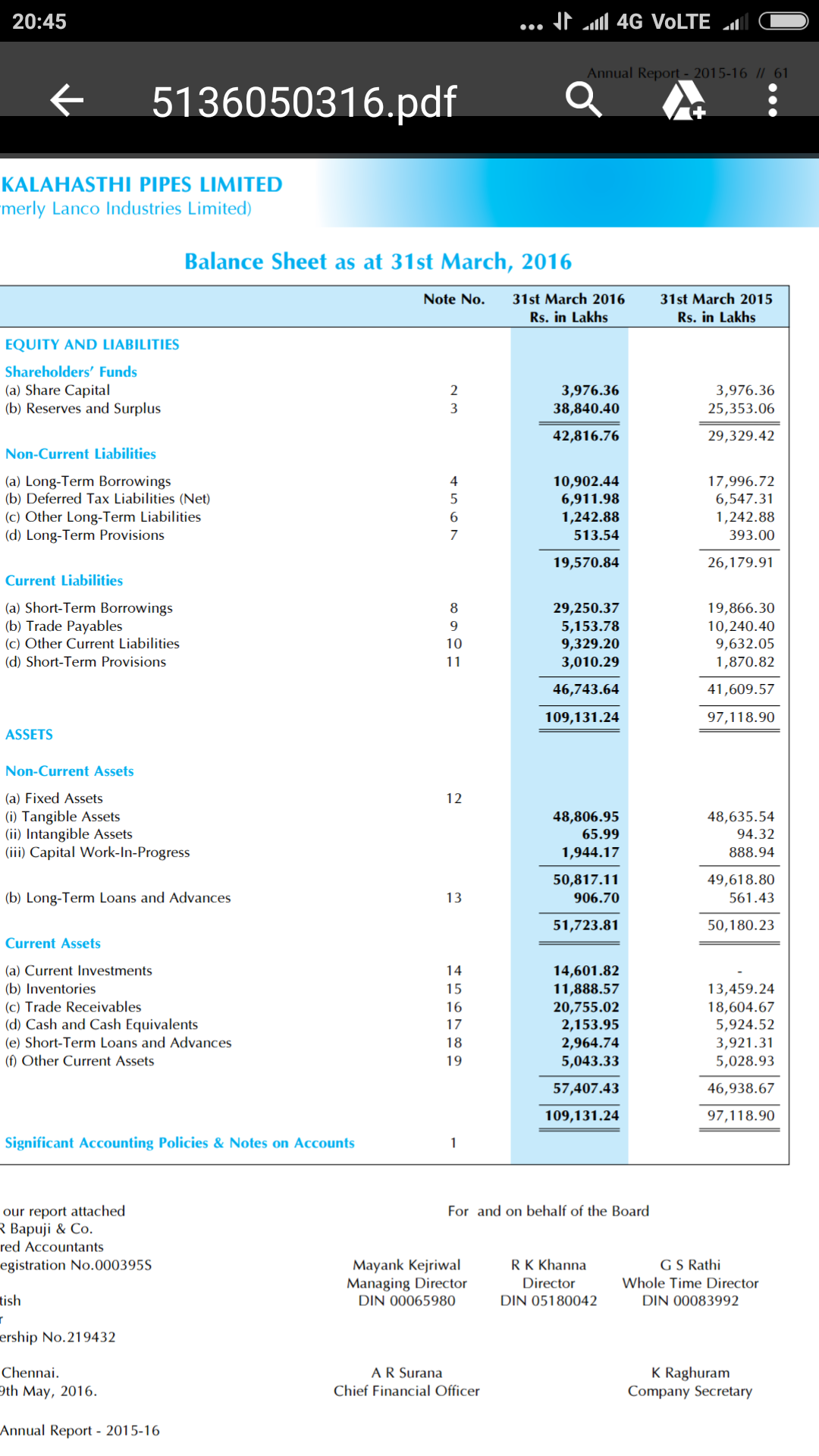

I am attaching the cash flow statement, Balance sheet and FA schedule from annual report of FY16.

I am not able to see the value mentioned in the above link either in Cash flow or asset register.

I also have a doubt…in the cash from Investing…there is a FA purchase of 39cr but this value is not reflecting in FA register…not sure if I am missing anything.

I just want to confirm, if the Electrosteel management is trying to stipend amount from SPL. As per related party transaction of AR2016 there is nothing alarming for me

Can someone please give some insights on understanding the 39cr FA purchase in Cash register but not in FA register. Also is there any clue on Mgt taking amounts from SPL.

Its a good point about the ECL overhang. Even though i cannot find any concrete proof for the same, a struggling parent is always a bad news for the subsidiaries. This remains the only -ve in my investment thesis on this co

I think we should wait for the ESL ownership to change from ECL to anyother company…if it’s done…I think the stock can rerate to some extent.

But looking at ECL books…it seems ECL is also suffering from high debt and low growth…advantage for ECL is its access to iron ore mines and experience in ductile Iron pipes…they can be low cost DI pipes producers…so need to wait for sometime before committing some part of your PF

On the sidelines thinking on contrary lines, what can this parent-child relationship do to Sripipes: Here are my guesses:

These guys are the leaders in the business despite the huge debt. Could all the 3 be brought out by a big guy for almost no cost? I remember Lakshmi Mittal buying Steel companies in Russia by repaying just the debt during his early years.

Worst case, sell off all the promoter holding? Implying that somebody else becomes the promoter. Sripipes at this stage doesn’t look like in need of big promoters to push its product across.

Keep Siphoning funds from one arm to another? Looking at the debt levels of the other 2 companies, no amount of siphoning is going to help. So i am ruling out this option beyond minor aberrations.

Status quo remains. Implying that Sripipes is going to grow atleast at 20% over the next 2 years atleast,

By actually deep diving into the possible outcomes, all of the 4 outcomes seems to be beneficial for people invested at current price.

Can somebody find a tragic end to this story from here just to prove me wrong?

If he doesn’t hold any shares, how does it hold against other corporates who are given ESOPs and RSU’s, 2% of net profit ?

And he’s got a 84.9% raise on top of a good performance by the company.

Total profit = 158 cr => 2% is roughly 3 cr

By any means, this is a significant amount and considering that they are paying this year after year irrespective of Company’s performance, it is certainly a red flag. It will be noteworthy to investigate if he was instrumental in getting some of the key projects and being paid for his marketing skills

On good aspect to this fact is that they have paid a very good dividend of Rs 5 to ensure that the minority shareholder is also rewarded.

Looks like we are told that everybody gets paid, but don’t ask who gets how much