News doing the rounds that Lanco Infratech is one of the 12 NPA accounts named by RBI yesterday. Please share opinions on how this might affect SRIPIPES

Successfully completed capex initiated in the FY 2015-16 entailing an investment of Rs.100 Crores towards installation of Pulverized Coal Injection (PCI) and Bell Less Top equipment facilities in MBF, capacity expansion of DI Pipe Plant, which includes installation of new spinning machine and additional finishing line. These facilities are commissioned during 3rd / 4th quarter of the FY 2016-17, and the Company will be reaping the full benefits from the facilities in terms of increased production of liquid metal and DI Pipes coupled with reduction in coke consumption from the Financial Year 2017-18 onwards.

Further, to be self-sufficient in meeting the coke and power requirements, the Company has taken up the project of installation of additional Coke Oven battery along with additional boiler in the Captive Power Plant at an investment of Rs.65 crores, which is expected to be in place in FY18. This investment will yield perennial benefit to the Company in terms of uninterrupted availability of Coke and power. This apart, post commissioning of dedicated Captive Oxygen Plant, the cost of production will come down further.

As regards setting up of Ferro Alloys Unit, as the Govt. of Andhra Pradesh has not extended power subsidy of Rs.1.50 per unit, the Company has deferred setting up of Ferro Alloys unit, as it is not viable to take up the Project in the absence of power subsidy. However, the Company is seriously pursuing with the Andhra Pradesh Government to reconsider extension of power subsidy to enable the Company to take up the Project.

Upcoming ambitious water supply projects, Amaravathi Capital Development Projects and infrastructure projects in 100 Smart Cities and 500 other Cities under AMRUT (Atal Mission for Rejuvenation and Urban Transformation) of Central Government and use of Ductile Iron Pipe in the non conventional sector like irrigation schemes etc., will ensure regular business and the company is hopeful of maintaining its growth.

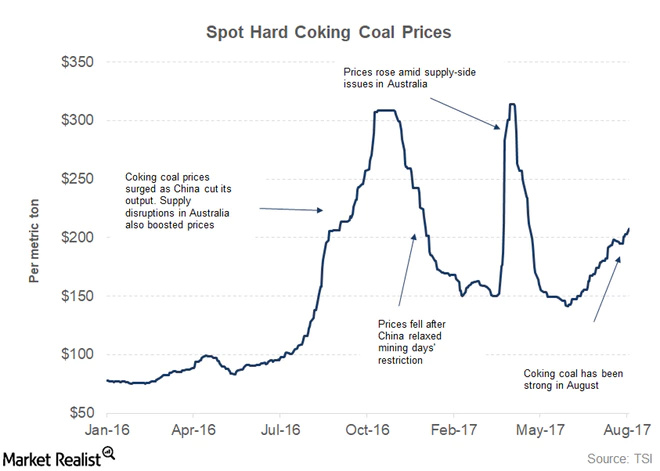

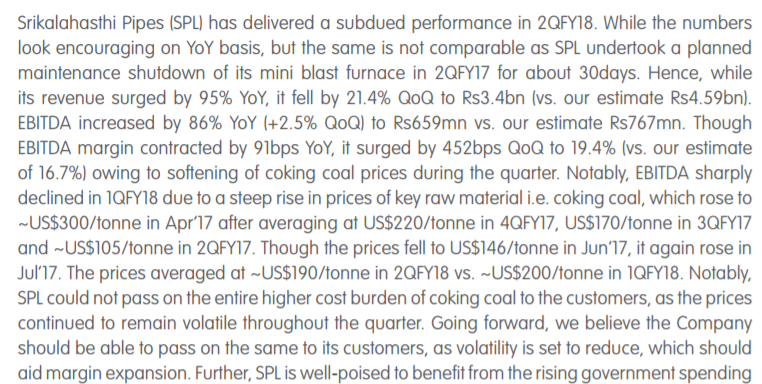

Multi-fold increase in the prices of coking coal during the 3rd quarter of the FY 2016- 17 due to supply-demand mismatch and partial rise in the prices of iron ore have resulted in higher cost of production, whereby leading to marginal reduction in the profitability at Rs.191.22 Crores compared to Rs.209.51 Crores registered in the FY 2015-16.

Total outstanding debt is 487 cr, of which 387 cr is working capital debt. Last year was 444 cr.

Growth in India is coming in several ways like Municipal and industrial waste water treatment, a high priority in recent government policies, and water reuse. India lagged in water infrastructure and sewerage development with only about 35% of the total population having access to improved sanitation. In rural areas, where about 65% of India’s population lives, only about 25% has coverage for sanitation. Due to this demand for Ductile Iron Pipes has been growing consistently over the last five years. With the priority being given by the Central Government for the improved drinking water supply and sanitation coverage, active consideration of inter linking of rivers programme by the Central Government for raising the irrigation potential and power generation across the country, the demand for Ductile Iron Pipes is expected to grow further in the medium to longer term. However, in view of higher market potential, it is likely that capacity addition, by way of increasing capacities by the existing players and entry of new players may take place in the domestic DI Pipe industry, which may intensify the competition and result in lower sales realizations, if the demand doesn’t go up as anticipated.

Related Party Transactions -

1 Electrosteel Castings Limited for Purchase of property ~ 55.20cr

2 Electrosteel Castings Limited for Sale of goods ~ 53.53cr

3 Electrosteel Castings Limited for Purchase of goods ~ 28.73cr

4 Electrosteel Castings Limited for Interest Received ~ 3.14cr

Considering the profitability of the Company during the FY 2016-17, the commission has been provided, which is 17.35% lower than the commission paid in the FY 2015-16.

Anil Kumar Goel, Dolly Khanna and HSBC Infra Fund increased stake in year 2016-17. Avis Tie up reduced stake to half during the year.

CARE Limited maintained its rating for the Company’s borrowing programmes with the rating as “CARE A+" for long term bank facilities and A1+ (A One Plus)”for the short term facilities.

My take -

Most critical factors to monitor here are increasing coking coal and iron ore prices. Everything else is good for this company and industry is having tailwinds. Topline will increase this year due to added capacity but PAT might not increase in same ratio due to increase in RM prices. Coking coal prices have come down in June-July to normal levels but are again on the rise due to increasing demand from China. Iron ore prices are also increasing due to China factor.

RM/Sales (in %)

Critical to monitor their order book. Telangana project is almost complete, so would be important to monitor the order book going forward to ensure stability.

One should keep an eye on Satvahana Ispat (stressed). Srikalahasthi might take over this company in future, as in one of the recent press releases company mentioned its desire to consider inorganic expansion if an opportunity presents. Satvahana and Srikalahasthi are based out of Andhra and Telangana region, so there are synergies. .

They bought a land from related party for rupees 55.20 cr and now they are planning to raise money via QIP. Don’t you think corporate governance is a little bad?

Disc.- I was invested and sold out after QIP news came in.

Yes, management (Mr. Kejariwal) has been iffy but business is growing at a rapid pace. Here, there’s a trade-off between corporate governance and business prospects.

Mr. R. K. Khanna

He is a Graduate in Management - Finance and holds a Post Graduate Diploma in Marketing & Sales Management from FMS, Delhi University. He has also completed a Certification Course in Infrastructure & Housing Finance from Wharton School of Management, U.S.A. He has rich experience in Financial Management and Banking Operations and has served as Dy. Chief of Finance in National Building Construction Corporation Limited, New Delhi. In his long stint of 25 years with HUDCO, he has held senior management positions viz. Executive Director and Sr. Executive Director and contributed for the business development of Western/ Eastern/ North Eastern Zones. He holds Directorship in Shivshahi Punarvasan Prakalp Ltd. (SPPL), Mumbai.

yes i also have same doubt. whats the problem of raising fund through QIP. please clarify. and if you observed their 2016-17 balance sheet they are expandig the Plant capacity from 2.25 MT to 3.0 MT… so requirement of fund is necessary and they are not diluting right. Please correct me if i am wrong…

Raising fund is not issue as long as it is funded for expansion or reduction in costs. Issue price needs to be considered before terming it as good or bad for existing investors. I don’t see the issuance details yet. Out of 250 Cr planned, 150 Cr will be used to repay ECB and buyer’s credit. 65 Cr towards captive power plant and rest for investment needs. ECBs should be generally low cost debt except for potential forex losses. As per last AR, it stands at LIBOR plus 4.6262. Debt will come down but not sure if it good for shareholders Optimal Debt is not a bad thing in my opinion. The excess return the company makes over the cost of the capital will drive its value.

Investments of around 200 cr vs market cap of 1400 cr

Trading at around PE od 10x on FY18E earning (considering H1FY18 results) vs Tata Metaliks which trades at 14-15x

Why is the market discounting Srikalahasti Pipes despite good operating performance and considering they are catering to South and West India where demand is more and hence logistics cost for them is low?

Yes, the recent results were good and it seems company has been able to optimally utilize the recent capacity expansion from 2.25 lac tonne to 3 lac tonne. As RM costs have been easing, we should see good margins for coming qtrs too.

I was worried to see the increasing debt and increasing receivables in the Sept 17 balance sheet. However, there is a substantial amount in investments…which are parked in mutual funds. It seems this amount is being accumulated to take over Sathavana, if they go ahead. From concall it seem Tata Metallik is also interested in Sathavana.

Don’t understand why Sripipe wanted to do a QIP sometime back

I have collated some data about D.I Pipe industry and manufacturers from public domain. summary is as follows

• Demand of DI Pipes grew by 13% CAGR during FY12-FY17.

• The current demand as per end usage of DI pipes is 80-85% for water projects and 10-13% for sewage and balance for others.

• Penetration of tap water in India is 44% as per 2011 census.

• The GoI spend in WSS sector has risen at a CAGR of 10% to 11% during 2012 to 2017.

The aggregate capacity in the sector has risen from 1.5 million tonnes in Fiscal 2012, to 2.25 million tonnes in Fiscal 2017. The capacity and utilisation of DI Pipe manufactures for FY17 is as follows.

Company Capacity (in Mn Ton) Utilisation

Jindal Saw 0.5 75%

Srikalahasthi 0.23 100%

Electrosteel casting 0.3 104%

Tata Metaliks 0.2 90%

Electrosteel Steel 0.2 70%

Rashmi 0.2 70%

Jai Balaji 0.2 26%

Electrotherm 0.2 51%

Sathavahana 0.2 46%

Total (Industry) 2.23 72%

Most of the companies are in trouble and this industry is consolidating among efficient and well capitalised players. Sathavahana is under SDR and Electrosteel steel is under bankruptcy proceedings.

The GoI’s continuous efforts on increasing the penetration of tap water and improving sewage facilities under various schemes will continue to support the sector during 2017 and 2022, which shall be facilitated by:

• Several GoI’s schemes such as, amongst others, ATAL Mission for Rejuvenation and Urban Transformation, Swach Bharat Abhayan and National Clean Ganga Mission;

• City level water grids planned by the state and municipal corporations such as, amongst others:

Telangana water grid project (₹ 370,000 million for laying 0.12 million kilometers of pipelines for supplying water to towns and villages apart from providing water for the industrial needs);

Marathwada water grid project to resolve water issues in the district;

Silk city water project at Behrampur, Odisha (₹ 5,820 million) for resolving drinking water problem of Berhampur and also for supplying water to 52 villages in Aska, Hinjili, Sheragada and Kukudakhandi blocks in Ganjam district.

Disclosure: Invested in Srikalahasti after recent correction.

Hi, due to recent market correction there income from mutual funds might get afffected and as a result might effect the bottom line. As other income is almost 20% of there PAT.