The gap between returns from MF and stocks has increased even further. Thanks to fund managers

Ideally, I would have increased stake in HDFC AMC in place of adding new entrant ABSL AMC but valuation wise, ABSL AMC is very attractive. The only thing which can hurt can be any possible corporate governance issue which HDFC AMC is considered to be quite good. It also means, I spread my risk in financialisation theme from 2 to 3 - BSE Limited, HDFC AMC and ABSL AMC. To be very honest, UTI AMC is even better in terms of valuation but the promoter share holding is going to be a recurring problem there. HDFC is also attractive in its valuation especially with real estate upcycle however, in financials, but I am little biased towards exploring financialisation theme specific to AMCs.

Olectra lost 5450 mega electric bus tender to Tata Motors due to lowest cost quote. I did a very good research about Tata Motors in 2018/19, especially their R&D spend was one of the best in the world at that time. However, I did not go further looking at its debt. During the March 2020 crash, the price of Tata Motors has fallen below its book value and in fact, the market cap was below 30k crores. With a strong promoter like Tata, given that it was its down cycle, it must have been an easy pick, given the fact that with so much of liquidity around, the interest expense also can be brought down. For now, comparing between Olectra and Tata Motors, the chance of Olectra giving higher returns is much more given that the market cap of Olectra is below 5k Crores and recently they won 2100 Electric Buses Order which is worth ~3600 Crores. As Olectra has to deliver them in an year’s time, the price/sales is going to be less than 1. Apart from that, the promoter is rebranding Olectra where they are no longer going to be dependent on BYD from China. With government itself looking for 50,000 Electric Buses in 5 years, the sector can give multiple winners with demand in place and also with localisation policy enforcement in place, costs also can become less in future

The reduction in share price of Dr. Lal path labs is significant. Diagnostic space is attracting multiple big firms as the opportunity size is gong to be huge. The latest one is Tata 1mg which started with promotional pricing of 100 Rs for some medical tests whereas the existing players are charging higher. Now, the valuation multiple got reduced immediately. My idea of staying put in this company is - the company is nimble in upgrading its technology, have deep understanding of target market and looking for adding the next level tests. Mr. Arvind Lal who is the MD mentioned that they are not going to cut the prices due to the competition. As per Dr. Velumani, ex-CEO of thyrocare technologies, to capture B2C market of diagnostic space, around 1 billion dollars of money needs to shell out. For a Tata backed company, funding should not be a problem but then Tatas are also not successful in all of their ventures. I could have sold my shares immediately after Tata 1mg news came up and sit on the sidelines till I get the confirmation but then I wanted to stay put. The experience is going to be more useful here

Studied a mining company called OZ Minerals by going through their annual report. The company gives dividend regularly and also is a big beneficiary of post-covid commodities boom. Their incentive structure for executives is well worth replicating in cyclical industries.

Interesting Videos -

Astral is one of those few companies which has increased their cashflows significantly. Their enterprising foray into adjacent segments is worth listening to from the founder & promoter himself in this video. From pipes and adhesives, now they are expanding into the new segments - tanks, valves, faucets, paints and some infrastructure divisions. Many companies are entering the paint business with Grasim recently announced 10,000 crores capex to their paints business. I have a vague feeling that Saurabh Mukherjee in his appreciation for Asian Paints business spilled out to the market that its not about the quality of paint but mastering the logistics in selling paints. Astral is targeting 600 cr revenue in coming years from its paints business. With signs of real estate cycle in the uptrend, may be Astral wanted to capitalise the opportunity the market is presenting now.

@harsh.beria93 has explained well about correlation between returns and the valuations here. The art of selling has to be mastered to beat index returns.

Interesting Insight. Do these promoters listen to PMS managers like Saurav Mukherjea before venturing into any segment? I mean didn’t they already know , what is the strength of companies in general, being in Indian Business community for so long? Because , I have always found Saurav Mukherjee to be wanting in his research and data analysis. He is a Macro storyteller, which hypnotizes the lay retail investor and he always paint all with same brushes, missing out on small nuances as he may be incapable of giving proper attention to details. I have read all his books and find that he exaggerates too many thins , just to support his already decided narratives. So in my opinion, retail investors may get carried away with his style, but experienced promoters of established companies may not give him any attention. Your views are welcome.

It is a given fact that every established company will have a market research team to continuously evaluate the competitors and also look for areas of expansion. Like you mentioned, Saurabh Mukherjea is a storyteller, the quality which inherently compels him to give more details to entice the audience further.

In the above video, he is giving out the numbers, underlying business model and strengths & weaknesses. Now, as and when his research team comes to know about some other snippet, he unknowingly will also share it with others as part of evaluating some other opportunity. When I say, I have a vague feeling, I mean to say I’m not sure but the story teller mindset can spill out information more than required to the market. In my opinion, Saurabh Mukherjea has got good research team. And this story telling helps him in getting more clients, selling more copies of his books and eventually gets more intellectual satisfaction.

BSE Sensex is performing slightly above in terms of returns

PF is down by 14% in Calendar Year 2022

The MF portfolio is more resilient than the stock PF as I did not deploy capital in MF after Dec 2020 but I still bought/sold in stock PF after Dec 2020. Ideally, if there is no incremental capital, I should have reduced my equity component as part of rebalancing exercise of my Equity: Debt ratio.

It takes a lot to drop a company like Titan, but like Charlie Munger says, investing is akin to Parimutuel betting. I see better risk-reward in the case of GPIL than Titan. Same is the case with reduction in Laurus labs.

Mid-cap and Small-cap indices have corrected a lot. I am contemplating on restarting SIPs in my existing MFs

Growth continues in Dmart & Nykaa. Avenue Supermart: a compounding machine? - #1958 by akash_das - Dmart revenue jumped 95% YoY growth. I don’t want to advocate BAAP(Buy At Any Price) but holding Dmart gives a sense of safety even though it always stays at high valuation. In the end, investing is about paying for the certainty of returns - predictability and sustainability of the earnings. I convinced myself to not sell it even though the stock was way overvalued when it was quoting at more than 5000 Rs as I felt staying put is more profitable for my PF in the long run and big corrections if any can be bought on dips.

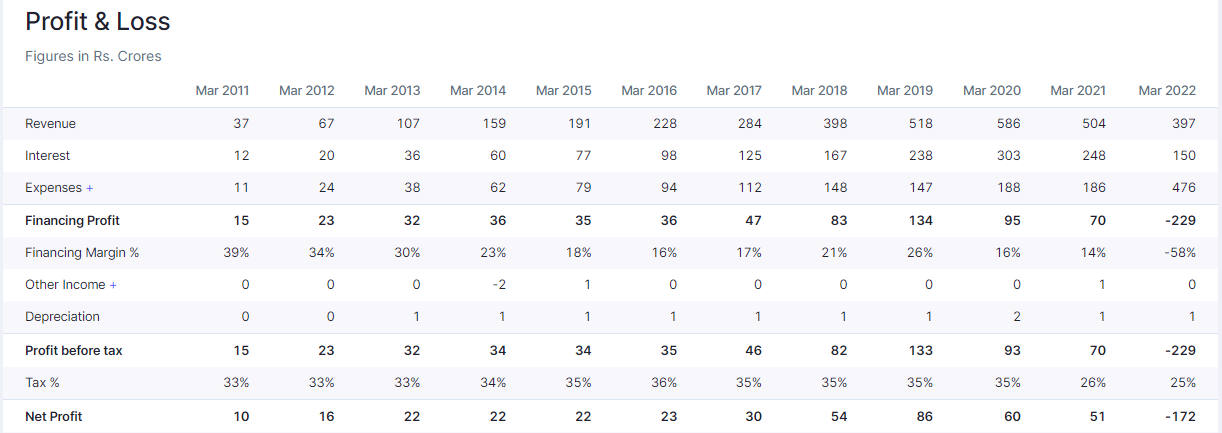

Long-term Investing in small/micro caps is very difficult. As I mentioned in the beginning of the thread, Muthoot Capital Services was selected as part of Coffee Can Portfolio stocks mentioned in the namesake book by Saurabh Mukherjea. That means, the stock displayed a consistent sales growth YoY and also ROCE for 10 years. Even then, the stock is now a fallen angel. The chance of it raising is very less as compared to its market cap of 276 Cr, it has a PBT of -229 Cr. I sold this last year as I could not convince myself staying on course with this even though, management is good, consistency in execution till March 2020. Especially, in finance sector, it is better to stay with leaders. The stock has fallen more than 50% from my sell price.

For a part-time investor like me, I see two approaches to make profit in stock market

Looking at index’s long-term PE or develop some other mechanism where we already track the company and get an estimate of normalized earnings and then enter when risk/reward is better. This PF thread explains this well.

Study a company in-depth, do extensive research and if the conviction is very high, enter at full force even in the middle of a bull market. The number of companies in the watch list should be very less and also conviction should be very high.

Based on the investing style, top-down works well with 1) and bottom-up with 2).

I am more of a top-down investor.

Few years back, while I was working in Paris, having seen different regions of France, I asked my then French manager about what would have been the motivation of general public(not government) to leave this resource rich, beautiful and highly developed region and work in relatively tough climates & foreign conditions elsewhere during French empire. He is a wise man and thought for sometime and told me, the primary reason must have been about inflation, security of future and then of course the attraction of high lamps & services. Reading about high inflation these days, I remembered those words

Words of Experienced Investor -

@zygo23554 has explained about the last decade in investing in this blog and I found the below words worth reading again

From whatever experience I have as a money manager in India, I can tell you this -

At an annual pre tax return of 8.5% from fixed income, many investors will happily take that over the volatility of investing in the equity market.

The most likely outcome of buying and holding the headline benchmark index in India over a 5-year timeframe has been a CAGR of 10-12% p.a. Across the world, investing gurus and academicians agree that the equity risk premium is broadly in the range of 5-6%. From here one can do the math and see how a 12% p.a. return from equity isn’t very superior to a credit risk free 8% p.a. in fixed income on a risk adjusted basis.

Doesn’t mean one stays away from equity, it is still one of the only few asset classes that has been proven to beat inflation over longer time frames.

It just means that one should be more demanding of above average growth from businesses rather than happily pay up 50 PE for a 10% growth based purely on 5-year average multiples. Consider 10-year average multiples to demand a higher margin of safety from here, of course adjusted for changes in business quality over the timeframe.

For this very reason, valuation is an art and not just a science.

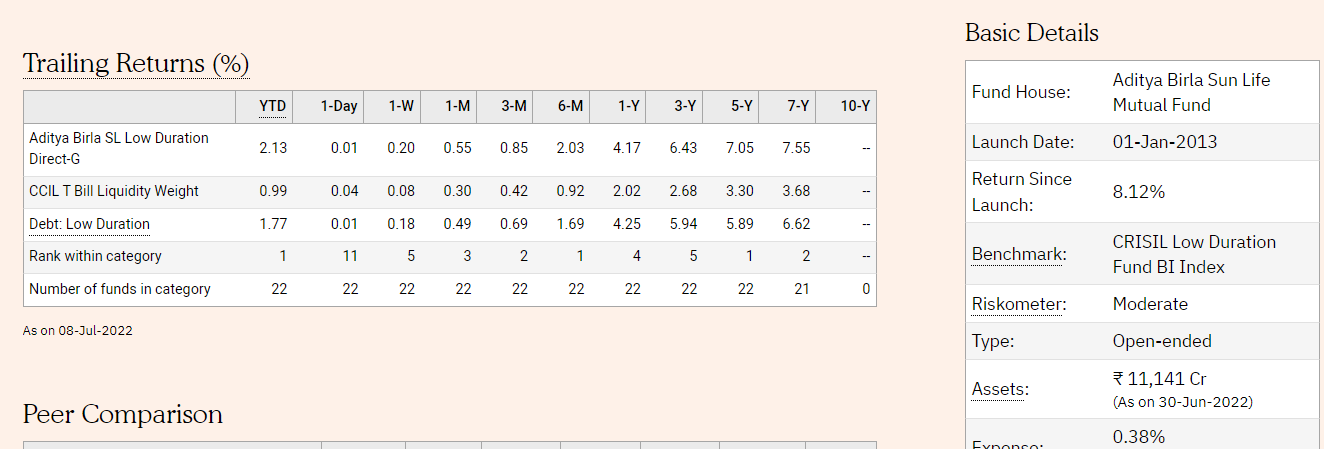

In the above screen-shot you can see that Aditya Birla Low duration fund has a 7-year CAGR of 7.55 and the category average is 6.62

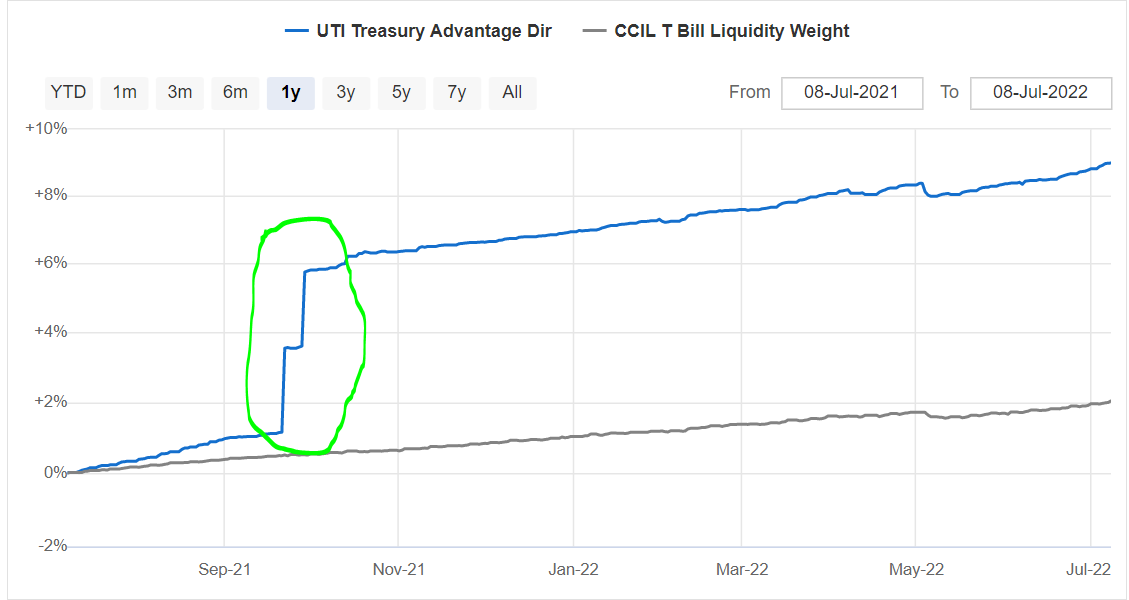

In the below screen-shot, UTI Treasury Advantage Fund 1-Year returns are close to 9. Usually, the higher the risk in the underlying bond is, more will be the returns. You may explore the underlying securities from this debt fund to find high yield ones. I have seen bonds from big listed firms like Muthoot Finance giving close to 10% yield as well in the past. As a cautionary note, government of India & RBI bonds are gold standard but even bonds from state government corporations carry risk.

In the past, Franklin Low duration fund was giving more than 9 as 3 year CAGR and I invested in it. In the first stint, I did not see any issue but in the second stint, even though I got my money back but I felt fixed income is not really fixed in debt funds.

What the author means here is, as soon as the debt funds/bonds/debentures give secured returns of 8.5%, the institutions/FPIs/FIIs leave much of high risk equities and prefer debt funds.

Rajeev Thakkar from Parag Parikh Mutual Fund actually started his career as a debt fund manager and continued in that role for many years - in fact, MF AUM has been much more on the debt side till 2014 as institutions are happy with debt fund returns. You can see that debt funds were quite popular back then. Aditya Birla MF Equity AUM jumped to 41% in FY22 of its overall AUM from 26% in FY17. FDs itself used to be touching 9% in 2000s & early 2010s. If those days are back, the demand for equities which we see now(ref high PE stocks) is meant to fall down drastically. The retail will be left high and dry. I just want to explain this to tell the importance of equity : debt mix in the portfolio.

Thanks a lot, it throws lot of light on the aspect.

Sharing may experience, for understanding of your readers who might be interested in debt options:

Historically my debt portfolio was divided in 2 components : EPF with my employer & Debt MFs.

For last 2 years, returns on Debt MFs had been dismal. I was not lucky enough to have invested in UTI Treasury advantage fund & thank you so much for sharing this example, shall help to deepen my understanding on debt funds. Shall study further what exactly happened from 20th Sept to 15th Oct 2021.

HDFC ASSET MANAGEMENT COMPANY LIMITED (XNSE:HDFCAMC)

Financial

Large Cap

15%

Financialization theme

2

GODAWARI POWER AND ISPAT LIMITED (XNSE:GPIL)

Metals

Small Cap

15%

Cyclical debt free & Value

3

OLECTRA GREENTECH LIMITED (XNSE:OLECTRA)

Automobile

Small Cap

13%

EV theme

4

HCL TECHNOLOGIES LIMITED (XNSE:HCLTECH)

Technology

Large Cap

9%

Coffee Can

5

AVENUE SUPERMARTS LIMITED (XNSE:DMART)

Services

Large Cap

7%

Long-term retail play, debt free

6

DR. LAL PATHLABS Limited (XNSE:LALPATHLAB)

Healthcare

Mid Cap

6%

Coffee Can

7

DEEPAK NITRITE LIMITED (XNSE:DEEPAKNTR)

Chemicals

Mid Cap

6%

Growth

8

ABBOTT INDIA LIMITED (XNSE:ABBOTINDIA)

Healthcare

Mid Cap

5%

Coffee Can

9

ASTRAL LIMITED (XNSE:ASTRAL)

Chemicals

Mid Cap

5%

Coffee Can

10

PSP PROJECTS LIMITED (XNSE:PSPPROJECT)

Construction

Small Cap

5%

Asset Light business in construction

11

GATEWAY DISTRIPARKS LIMITED (XNSE:GATEWAY)

Services

Small Cap

4%

Promising sector for future

12

ADITYA BIRLA SUN LIFE AMC LIMITED (XNSE:ABSLAMC)

Financial

Mid Cap

3%

Financialization theme

13

LAURUS LABS LIMITED (XNSE:LAURUSLABS)

Healthcare

Mid Cap

2%

Growth

14

Fsn E-Commerce Ventures Ltd (XNSE:NYKAA)

Services

Mid Cap

2%

Growth

15

HDFC BANK LIMITED (XNSE:HDFCBANK)

Financial

Large Cap

2%

Coffee Can

Stocks

Top 5

58%

Top 10

85%

Top 15

98%

Market Cap

Large Cap

32%

Mid Cap

31%

Small Cap

36%

Sector Split

Financial

21%

Metals & Mining

15%

Services

14%

Automobile

13%

Healthcare

13%

Chemicals

11%

Technology

9%

Construction

5%

Defensive

22%

New Age/Theme

15%

Investing Objectives –

Return of Capital

Beat BSE Sensex in terms of CAGR

Beat FD returns

Reach 15% CAGR

Beat MF(direct) returns (21.8% Vs 20.1% CAGR)

Changes -

• Sold off BSE Limited after change of CEO announcement in July 2022

• Sold off DSP Healthcare MF units completely in January 2023 due to personal needs

Notes -

PF is down by 5% in Calendar Year 2022 following great returns of 62% in 2021

2023 has been another good year in terms of returns in direct equity. The portfolio 1 Year returns are 43% and beats Sensex (19%) & NIFTY 500 (25%)

Overall CAGR since inception (Feb 2018) is just above 20%

Direct Equity: MF stands at 77:23 & Equity: Debt stands at 68:32

I have intentionally stayed away from stock market most of the time after July 2022 to focus on my new job & subsequently increase my investible corpus

What investing in stock market has helped me is to think clearly to understand the drivers that determine bottom-line/desired target state, appreciate the process than outcome, understand core human nature, appreciate time - I am understanding & investing in myself more now

Studying annual reports of clients have become a pre-requisite for me before engaging with them to get a good overview about them

I strongly believe equity investing is one of the safest & fastest ways to achieve Financial Independence given you have a sound temperament & process aligned to your goals

I’m glad I stumbled upon this forum, it helped me not only to understand different thinking patterns but also refining my thoughts by way of journaling

Return of Capital

Beat BSE Sensex in terms of CAGR

Beat FD returns

Reach 15% CAGR

Beat MF(direct) returns (18.9% Vs 17.8% CAGR)

Changes -

• No buying or selling shares or MFs since July 2022

Notes -

PF Returns vs Sensex vs NIFTY in % - CY 2025 (5.2,8.6,11.9), 2024 (18.3,8.2,8.8), last 1-year return is 17%

After a strong PF Performance in 2023 and 2024 where it beats Sensex and NIFTY 50 significantly, the PF was down in CY 2025.

Overall CAGR since inception (Feb 2018) is 18%

Direct Equity: MF stands at 76:24 & Equity: Debt stands at 43:57

Top performing stocks by amount - GPIL, and HDFC AMC. Both having a significant allocation % lifted the PF performance.

Stocks with more than 20 CAGR - GPIL, Laurus Labs, Gateway Distriparks, Aditya Birla AMC, HDFC AMC

My bet on finalisation theme turned out to be good apart from GPIL - HDFC AMC and Aditya Birla AMC did very well during this period. In fact, with HDFC AMC giving Rupees 54 Dividend, It translates to 5% based on my buying price. With increasing dividend YoY, it I am going to sit on a stock which gives me more than FD returns even if stock price growth might slow down in some years. I thought HDFC AMC being my portfolio highest allocation gives me peace. I am happy for giving it the weight it deserved.

I have intentionally stayed away from stock market most of the time after July 2022 to focus on my new job & subsequently increase my investible corpus. All the free cash flow from the job is parked in Fixed deposits during this period. The AUD to INR exchange rate appreciated by ~22% in last 1 year. This has helped with a very good war chest.

What investing in stock market has helped me is to think clearly to understand the drivers that determine bottom-line/desired target state, appreciate the process than outcome, understand core human nature, appreciate time - I am understanding & investing in myself more now. I evaluated my current state in life by going through Maslow’s hierarchy of needs. Corporate engine thrives due to goal setting and feedback mechanism. I am kind of doing it myself tracking it to eventually realise Self-actualisation phase.

I heard from a consulting leader in Europe that the world always tries to highlight our areas of improvement but the best thing for us is actually focus more on leveraging our strengths. This along with application of Pareto principle (80/20) has a significant effect on both my professional and personal life. I focus on leveraging my strengths as much as I can.

I strongly believe equity investing is one of the safest & fastest ways to achieve Financial Independence given you have a sound temperament & process aligned to your goals. In equity investing, the bet is on the CEO/Management/Board who run the company of behalf of the shareholders to deliver the returns - Indirect way. I found a trusted and aligned partner, and started my entrepreneurial journey - Direct way. The direct way is comparatively risky but the war chest created, strategy and execution so far based on our detailed planning is giving us confidence to thrive. The dream is to list our company in stock exchanges one day.

To conclude - I started doing option analysis of Stocks vs MFs for my investible corpus. I realised higher salary translates to higher contribution to net investible capital and subsequently to net wealth - Depends on your corpus size. I now believe I can increase my net wealth faster as an employer than an employee. I aim to be FIRE in 5 to 10 years.

Good to see your post after long. No selling stocks/MF maybe fine but no buying either inspite of so many opportunities macro as well as in individual stocks means you have turned into passive investor. (maybe temporarily) or either you had invested significant capital (as much as you intended) into equity in 2022 itself. Whats not clear is that you mention FIRE via equity investing but had been completely inactive since almost 4 years. Did you never think of adding on to your positions or weeding out any pick for better ones, buying dips/crashes etc.? If not, is your invested capital by 2022 enough to lead to FIRE in next 5-10 years as you mention?