FY 19 Q1 SIB_June_18_Financial_Result.pdf (1000.6 KB)

Higher provision dragged the profit down and the NPA shot up … I guess this year also the Total provision would be around 850 - 900 crores

FY 19 Q1 SIB_June_18_Financial_Result.pdf (1000.6 KB)

Higher provision dragged the profit down and the NPA shot up … I guess this year also the Total provision would be around 850 - 900 crores

Good set of numbers by south indian bank…stock was hammered badly by the markets due to the last quarter

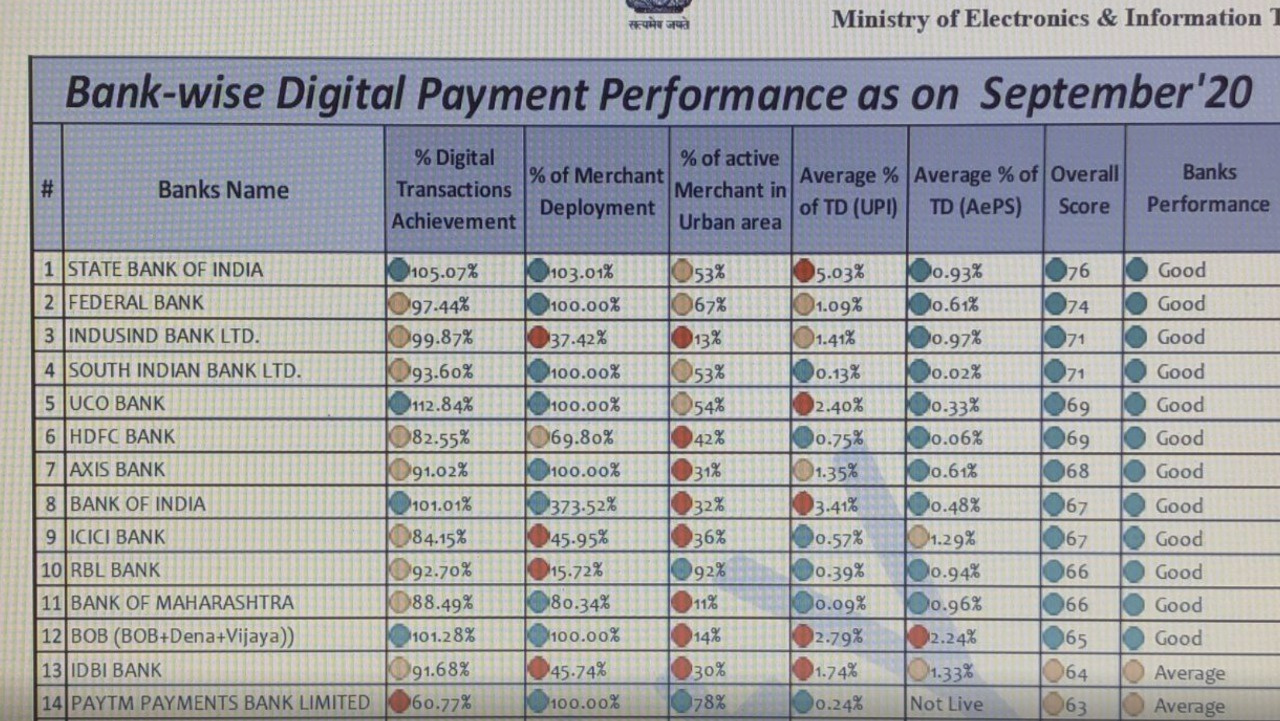

Does SIB have any exposure to DHFL ? Is there a way to find out ?

South Indian Bank Q4 profit falls 38% to Rs 71 crore

1)Is there any way to find out SIBs exposure to DHFL,Coffee day group or IL&FS.

2)Mohnis pabrai , yusuf ali, Lavender investment and many others have bought stake in this bank in past so at that time they must done some calculations and based on that they invested such a huge money.

So now what was changed ?

At Rs.10 isnt it good oppurtunity?

3)What are the major negatives with this bank other than NPA.?

DISC.:- not invested

Yes,

NPA is an inherent issue with this Bank.

Not so high that it fails, not so low that we call it a Quality bank.

Was offering Good value at 0.2 times the book value. Is not worth above 0.5 times of the book.

Being Kerala focused bank should have lower impact of Covid.

Disc.: Invested at lower level.

SIB price is mostly much below book value and it was always cheapest among peers. Considering the 20-Q4 result nothing improved from previous one. But just in one month its rallied over 80%, any fundamental change or because of its so cheap?

My views on South Indian Bank based on Q4 FY20 Results

Positives

Negatives

At Rs 1500 Cr market capitalisation, with a 929 branch network, access to lower cost deposits, and an almost Rs 150000 Cr business and a book value of Rs 30 (The bank is currently available at 0.3x book) the valuations are cheaper. But with more stress & slippages expected in the short to medium term one can expect 50% valuations decline. The bank is potentially a good acquisition target for some of the mid-sized / large banks & NBFC’s. Besides if the bank is in a position to survive the crisis over the next 12-18 months, contain and manage the slippages, improve the performance metrics, sort the legacy wholesale banking issues, improve loan book asset quality, there is a good prospect of NIM expansion, increase in ROE which can lead to re-rating closer to a 0.75 x to 1x book value

Disc: Invested at higher levels, will look at adding at much lower levels closer to its recent Low

In my view, FY21 and FY22 will be tough for SIB. Total business especially deposit will be down at-least by 20% due to Middle-east NRI remittance shortage.

Finally, their web portal looks decent. It was really unpolished before the recent update!

ok it might be copy paste but i think from valuation perspective this stock is not attractive. Refer to my DCB post on why i think so. Any thoughts on this approach?

Ex-ICICI Bank executive Murali Ramakrishnan likely to be named as CEO of South Indian Bank

It appears Ashish Dhawan booked loss and exited , he was holding 1.5% of SIB for a while !

Portuguese firm Pettigo Comercio Internacional LDA bought 99,71,500 shares of South Indian Bank at Rs 9.04 per share.

Source of this news ??

watch from 0:44

Why did they issue these equity shares for? Here is the link to the article. This action doesn’t dilute the existing shareholder if the purchase price of the existing share holder is below the issue price of 8.48 correct?