Hi All

I was trying a way to find the cheapest stock in banks and used the below methodology. what you all think?

I use an average of P/E x Gross NPA% AND P/B x Gross NPA % to find the lowest ratio along with those banks only where Capital Adequacy is >12.5% as required by Basel norms on a conservative basis**

Many of you might be seeing above stock-picking methodology for first time. Reasons for this is as below

Example 1: Suppose you have two stocks with a P/E of 10 and Gross NPA of 1% and 2% respectively with all else being the same. Which one will you choose? Of course stock 1 with NPA of 1%

Example 2: Suppose you have two stocks with a P/B of 1 and Gross NPA of 1% and 2% respectively with all else being the same. Which one will you choose? Of course stock 1 with NPA of 1%

So this is what this formula tries to do when I do use the above methodology. The assumption, of course, is if a stock has High P/E it should have lower NPA% and good CAR that’s why it depending high P/E. Given the inverse relationship NPA% has with P/E and P/B, I take a multiplicative average of both so that i can do a fair comparison b/w large cap and small cap as small-cap companies are expected to have lower P/E and higher NPA% than large-cap.

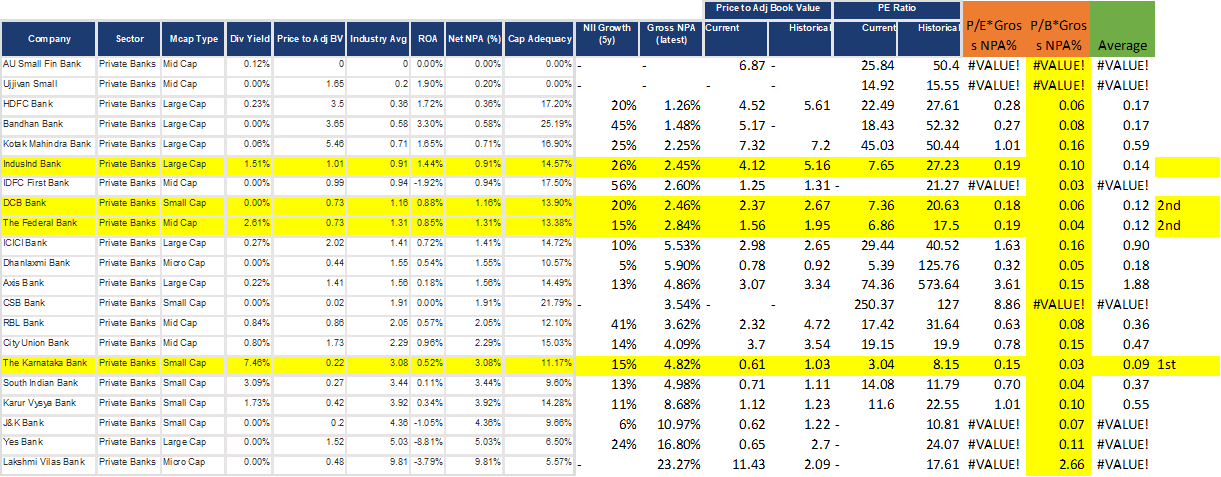

Now I don’t have all the data but last time I did an analysis of Banking stock I noticed below ( i usually refresh my analysis every quarter post result get published and rebalance my sector holding as per that and same goes for banking )

You will see the last three columns where I have calculated using the above methodology. You will see that the lowest average using the average of P/E x Gross NPA% AND P/B X Gross NPA % are of**

(1) DCB Bank

(2) Federal Bank

(3) Karnataka bank

Now on top 3:

-

Karnataka bank: I am not comfortable with such a high NPA % on absolute level although it might be the cheapest as NPA being high is already reflected in its low P/E. Different people can have a different view but my model showed this as the cheapest stock in Private banks

-

DCB vs Federal bank: Really a very close fight. On DCB:

-

Net and gross NPA % is slightly better although I agree P/E is slightly higher than Federal

-

The potential as per Historical P/E was higher in DCB as compared to Federal

-

Capital adequacy of DCB is slightly better than Federal

What you all think of this approach?