You have to find it amusing that this is priced cheaper than Uno Minda which is not as technologically adept as Sona. Management has been walking the talk and remember that we still are not in the golden age of EVs. I predict that this will start as soon as EV production gets to the price of fueled vehicles. Market will realize this sooner or later.

3 Likes

Comparing with a over-valued stock doesn’t make Sona BLW’s valuation reasonable (I don’t track Uno Minda, I take your word on it’s over valuation).

If we buy Sona BLW at current multiples, how big their business and bottomline growth should be for an investor at current valuation to get good returns?

2 Likes

The value of any business is sum of all the future discounted cash flows.

Sonacoms is sitting on 7X order book to its annual revenue, which they will deplete over 10 years. The company has outstanding track record over past 5 years of delivering 20% RoE.

They average growth rate has remained > 20% over 5 years.

What all this means is that you can expect consistency and predictability going ahead too. The future cash flows for next 5-6 years should grow at 18-20% in as-is scenario. Considering that, the market price is lower than value. Also, company is going to benefit from PLIs from next fiscal year.

What is troubling market is US tariff fear and China’s EV push. I am more fearful of later because Chinese have their own ecosystem. If they conquer EU EV market, it will be bad for entire EV value chain in rest of the world - OEMs, Part manufacturers, ER&D players…

Chinese EV manufacturers only employ Chinese auto parts manufacturers, own software providers. So you can’t supply to them, unless you build trust with them in China market, not in EU.

So when these are the challenges, recovery becomes time-taking and would require clarity in the global ecosystem. Also, when everything is down and becoming cheaper, the competition is not with its own price and value gap, but price and value gap of other interesting businesses also. Therefore, it will be very difficult to say when the gap between price and value will be bridged.

Stance - Invested

.

16 Likes

Given the recent tariffs news, how do we see one year business & margins impact for Sona Blw? There was a general slowdown in EV market even before the initial 10% tariff announcement. So,there is slow down in demand, possibility of order book realisation getting delayed, potential impact on margins and so on. And even at current prices, I feel the valuation is quite rich

2 Likes

They have a plant in Mexico, which may take a hard hit of tariffs.

In the last call Vivek is confident that tariffs may not impact much but tariffs will boost the vehicle prices, which is -ve for US itself.

Sona has some pricing power, they will manage growth margins equally to an optimum level

Most executives, will be slow in alarming the investors of these kind of effects, partly , they initially think, they can to some extent mitigate the issues, or the issues are not fully clear and are still evolving, or they dont want a knee jerk reactions/panic among their investor, for good or for bad reason. But experience says these will hit the economics if implemented, So it will be upto us, how we make risk adjustments in these kind of situation , especially when the valuations of individual company are high.

3 Likes

You are right. Very rarely you will hear management saying that they will be highly impacted by the tariffs or some other bad news. All of them put up a brave face and try to say it will have minimal impact on them. It will be interesting to listen to commentary of various concalls and compare it after few quarters with reality.

3 Likes

Interesting to see such low activity in Sona BLW forum. I was reminded of this company yesterday after the kids of Swargiya Sunjay Kapoor(Through Karishma) filed a case in Delhi HC seeking their part in the inheritance.

I have taken some time to study this company yesterday and today morning. Currently, it seems to be down due to the legal tangle(which actually has no bearing on the company operations), some degrowth in revenues in Q1 and Trump’s tariff tantrums.

I think within a few weeks, at least a few of these factors will be eliminated. In the earnings call of the company(which also drew less interest is evidenced by 1 guy asking so many questions) they have discussed that the revenue was not lost, just shifted to Q2. That means Q2 will have more earnings than usual. The railway business too will report its first full quarter in Q2 results. So earnings are bound to increase. By how much, is anybody’s guess. But my sense is there will be substantial growth and will surprise many of us.

On the tariff issue, the deal is again on after today and it should be finalised sometime later this year. Sunjay’s assets’ division shall have zero impact on running of the company. So, sentiment should improve starting sometime in October.

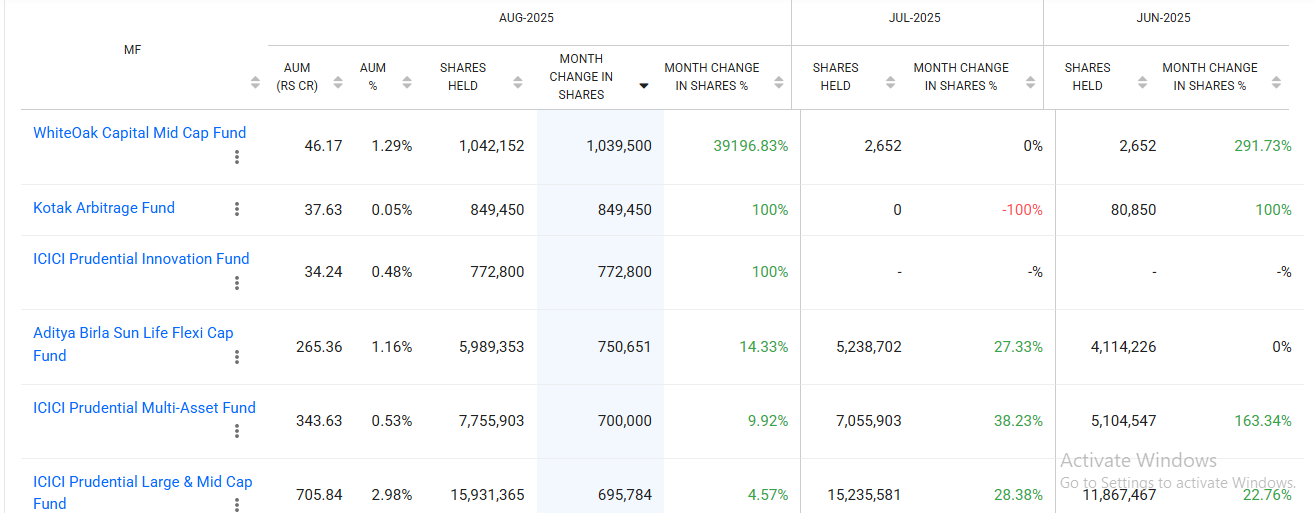

Mutual Funds have been using the time to increase their positions in the company over last few months. SBI and ICICI already had large positions and have increased the same. A snapshot from trendlyne is below :

The revenue of the company is sticky and innovation is happening with a tech roadmap in place.

Disc : Invested today around 450. Very biased.

14 Likes

I think the major concern ( the legal tussle as you mentioned doesn’t impact operations) is the lack of topline and bottomline growth from last 2 Qs. Remember Sona is running at a stable OPM% of ~26-28% in the last 3Y. During that time, they grew topline and bottomline by 19-20%.

Now, they are entering the railway business which might give some filip to the topline but it has a lower margin profile than the company average (atleast for the near future).

I would think the PE de-rating from 70-90 range to now 45-55 is taking this into account. Can they grow their topline much faster than 20% to still have a ~20% PAT growth while the railway business matures? This is the main question. Operationally, management is top notch, no doubt.

6 Likes

Thanks.

I got the sense that this is not only possible, but highly probable.The margins will shrink, no doubt, as the management has accepted. But all other ratios being good, the question is volume(revenue) growth.

The Chinese JV too is basically for volume growth a few years in the future. That with the tech roadmap to move up the value chain give me a feeling that we are good for the time being.

Of course, I am highly biased.

4 Likes

They gave clarifications related to lot of fake news that is floating around the company and they feel like some value erosion tactics are going on with the company. Is it really true or are they trying save their reputation and/or trying to divert shareholders from the real matter? if someone can shed some light

Disc: Invested

1 Like

I may have missed, but can you elaborate, saving reputation from what? and what according to you is the real matter? did the mgmt of the company do something wrong?

Thanks for clarifying.

1 Like

Recent interview of the CEO. He has a vision for sure and an eye for industry trends.

4 Likes

Since I last posted, Sona has fallen further. Technically, I think it is in a good place now. We should be seeing the results of this quarter sometime in November. I think the revenue would be much higher than last time. They deferred revenue recognition from a large order to Q2 from Q1 as explained in Q1 concall. This and coupled with Railways being there for the full quarter, there is a very strong possibility that revenue would be north of 1000 crore for the quarter. More important would be the margins. If they retain good margins and PAT growth, we could see the good times again.

The current share of 2 and 3 wheeler EVs in its revenue is 8%. With the PLI certification of its 2 and 3w traction motors, we could see an increase in domestic orders. On the other hand, US tariffs are going to hurt it in its biggest export market. Some of that would be countered by the Mexico plant, but management expects about 3% impact on revenues. As the trade deal is finalised it will be a breather for Sona and for us shareholders. The quarterly results will also show the imapct of these tariffs on Sona. I think Sona may have to digest some tariffs while the OEMs will have to digest the rest. The OEMs cannot shift to entirely new supplier as they will have to get all parts to be recertified, homologation to be done etc. etc. Basically, all manufacturing will stop. So, for at least a few quarters they too will hope for a peaceful resolution. In the meanwhile the Mexico facility of Sona can help them reduce some burden.

Eagerly waiting for the result.

Disc : Inested and biased.

11 Likes

5 Likes

Yes. One of the few Indian companies that is actively working on deep RnD and technical fields. Past 3 years have been a drag because of the unreasoable 2021 valuations but confident od decent valuations now given the high order book and cutting edge focus

6 Likes