Just to give a background to those who are not aware of it, here is the chain of events (feel free to point out errors)

Karvy provides broking & demat services

Karvy illegally transferred shares of its clients to its own demat account (or maybe the common pool account)

Karvy then pledged these shares to borrow from banks/NBFCs

Karvy, apparently, also sold some of these shares and transferred the proceeds to its related businesses

Some clients noticed this misuse of shares and complained to SEBI

SEBI found that about Rs 2800 crores worth of shares were misused to borrow some Rs 600 crores

SEBI directed Karvy to stop its broking services and onboarding of new clients

NSE/BSE suspended Karvy’s broking license

NSDL, on its own, decided to transfer shares pledged by Karvy (but actually belonging to its clients) back to the clients’ demat accounts. So some clients were lucky enough to get back their shares!

Here is a press release about this:

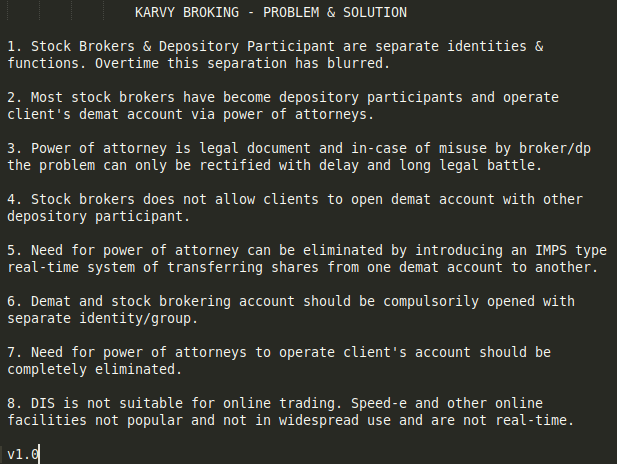

Its about the PoA

Everything boils down to Karvy’s misuse of power of attorney (PoA), provided to it by its clients. Most broking houses make it mandatory (at least the onboarding executives say so) for new clients to provide a PoA. A PoA allows the broker to initiate debit requests to your demat account when you place sell requests. Apparently it can also be misused to pledge and/or transfer your shares to any other account, which is quite scary!

My question

Today I received an email from NSDL with some advisory. It had these points (amond many other points):

• Be careful while executing the PoA (Power of Attorney) - specify all the rights that the stock broker can exercise and timeframe for which PoA is valid. It may be noted that PoA is not a mandatory requirement as per SEBI / Exchanges.

• Register for online applications viz Speed-e and Easiest provided by Depositories for online delivery of securities as an alternative to PoA.

Is any one here experienced with going about using the above alternatives?

How do we register for them and ask our broker to revoke the PoA?

How do we limit the PoA to only allow debits for trades initiated by us?

Very valid and important points above. These brokers make us sign dozens of documents. I am thinking aloud…the trading account is linked to dmat as well as savings account…when we do not need to sign any PoA to debit our bank account to hold funds when we need them to buy shares (they happen only on our request initiated in the tool) then why do we need any PoA for dmat account? Is PoA only a safeguard for brokers to save them in case of genuine defaulter clients? In that case, it should not be mandatory for clients? Thoughts welcome!

Those having NSDL demate account must open speed e facility. It’s free and easy to operate. And risk free as u can transfer online to only predefined broker only . And any additions of broker can be done only by nsdl

I don’t have the exact answers to what you have asked, I received the same email from NSDL. Investing without a POA is very difficult even if you buy sell only a few times a year. Your signatures need to match every time, go to the physical office.

I have an alternative that was suggested by some gentleman in the “select a broker” thread. If you are interested you can use this method. I will give a small brief here, and you can go into the detailed execution on the actual thread.

Essentially you keep 2 DEMAT accounts, one is linked to a broker for buying, selling, with POA, another is a standalone account with no broker having the POA to it.

You register for online transactions with the respective depository, ie. CDSL or NSDL for both DEMATs. This will allow you to transfer the shares from one DEMAT to another. Or you can use the offline DSI as well.

This method is ideal for long term investors, you buy the shares and after t+2 you transfer them from your broker linked DEMAT to POA free DEMAT. And for added security lock the shares from transfer with the depository.

When you want to sell the shares after a few years or decades, you remove the lock in, transfer the shares to the broker linked DEMAT and then sell.

Another alternative suggested by a gentleman on twitter, what he does is he creates a LAS pledge on his entire holding for a small amount of loan. So the collateral is very high compared to the loan. He puts this loan amount in an FD or debt fund and gets security of his shares with a carry cost of say 3-4% on a very small amount.

So until he clears the loan and the pledge no one can remove the shares from the DEMAT.

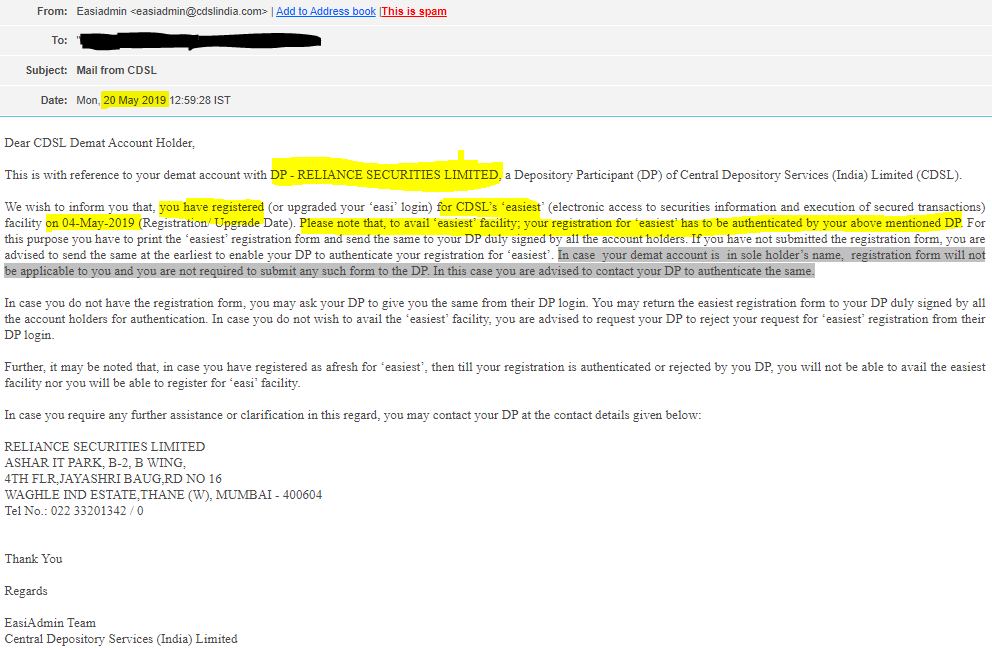

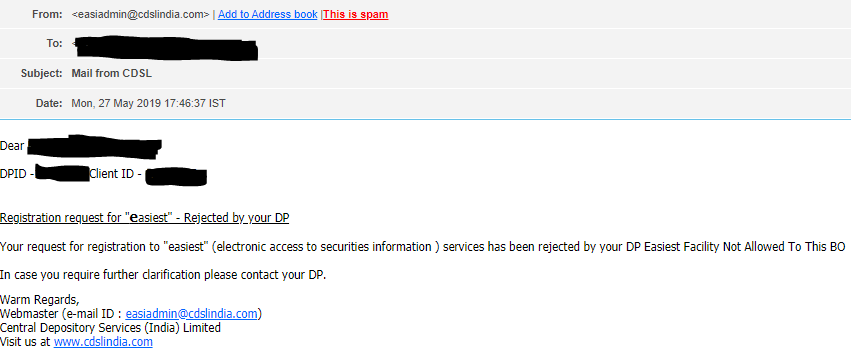

Thanks for sharing details, which I have been exploring for last few months (well before Karvy issue exploded). I did register for EASI & Easiest, wherein CDSL requested me to get it authenticated by DP. When I contacted DP (Reliance Capital now Reliance Securities), they informed that they don’t have such facility with them & aborted the process initiated by me.

Now the question arises that if its (Easi & Easiest) owned & provided by CDSL/NSDL, why DP has to authenticate? I feel that it opens the scope for other DPs to misuse POAs and create another Karvy like scenario, where retail clients are blamed for either not reading POA during account opening process before authorizing the DP or not monitoring various statements/ sms received by DP & Regulators.

I am not a moderator. You can put this in the following thread. That thread is meant for discussions on alternatives to providing a PoA. The discussion can be continued there.

The difference between easi & easiest is that in case of Easi you can only view your statement whereas, in case of easiest, you can execute transactions electronically without the actual use of instruction slip. Since easiest involves transaction execution without the use of DIS, it requires your DP to have it enabled from the depository which not every DP gets it done. On the other hand statement viewing facility (Easi/Speed-E) is available to all account holders of CDSL & NSDL who are registered for that & no authentication is required from your DP.

As I can see, you are already registered for Easi facility, you can log in to CDSL site and check your statement online.

I have an account with Karvy in Bangalore which I used to buy shares. All shares used to be in pool account till I realised that dividend was not properly credited. So I moved all shares to demat. Thereafter I moved to Mumbai but didn’t transfer account to new place. But once in a while used to verify demat holdings. The account was dormant.

I am currently with different broker since many years. Recently when I checked my Karvy account after recent fiasco, all shares are there in demat with some cash lying in account. I could trace out my DIS also, all lying unused.

Since I am in Mumbai and can’t travel to Bangalore for this reason alone, how can I transfer my shares to different DP? Is visiting branch must? I checked easiest cdsl. All it allows us to verify holdings but is there any way to transfer from Karvy dp to different DP online?

Yes, I regularly use Easi & my query is related to Easiest (you can see from the snippets of mail shared in earlier post)

So the DP keeps the individual in dark & breaches the trust as Karvy did. Somehow I don’t trust regulators in our country & I have valid reasons for this. These regulators achieve 100% efficiency in protecting big corporate houses & retailer / individual always remains the sufferer. TRAI actions in recent DTH rules increasing each house hold bill & their claims that they protect viewers rights is known to everyone. Similarly CDSL asked me to get my request authenticated by DP, which was denied by DP. Now CDSL knows that request was raised by retail investor but they will NOT take action against DP (or even request DP to have such facility enabled, if they need some infra/process etc at their end for this facility)

One way they claim that its FREE service in interest of investor but on other hand they leave it loose for DP to authenticate / reject the request. My complaint to CDSL / SEBI & DP in this regard couldn’t get any positive response.

u can open demat account in other dp , if your broker permits. and transfer shares in pay in thru online speed e to your broker. so u have full control over your shares.

Very interesting ways you mention to mitigate the risk. Some basic question come to my mind.

In case of a long term investor - suppose I buy share from a Trading account linked to DP and my DMAT account (typical 3 in 1 accounts that Banks offer). Is it possible that if I want to keep those shares for very long, I simply close the Trading account only with the DP (That should keep my Savings and DMAT account open. This ways, until I link that DMAT to any trading account - no one, including myself, can sell or pledge those shares?

I see in statements from Depositories that they link the DMAT account with DP. Can we not have a standalone DMAT account with Depository only? (no DP involved - like in case above if we delink the DP by closing the trading account) When needed, can we not link that DMAT to any new Trading account we open?

Yes you can do that. I closed my account with HDFCSEC last year, if I remember correctly there was definitely an option to close just the trading account and maintain the DEMAT.

As per my knowledge a DP is absolutely needed to open a DEMAT as per SEBI regulations. CDSL and NSDL cannot directly deal with the clients.

Remember the POA is given to the broker and not the DP. Ex. before zerodha became a DP they used ILFS SEC as the DP. The POA was given to zerodha. Nowadays we have lots of brokers who have become DPs. This makes extra income for them and they can provide extra services to their clients. Unfortunately, it also creates a potential for misuse if the operations are not separated.

As I said in the original post the idea was not mine, it was someone else’s. I haven’t actually executed the above plan as I do not feel the need of it yet for me, but the gentleman in the original thread has executed it already. I will try to answer whatever queries I can, but he will be of greater help here.

Even ICICI Securities (ICICI Direct) at account opening made retail investors to sign PoA. I am talking this about almost 10 years back. Not sure if now DP such as HDFC Sec and ICICI Sec make customers to sign PoA.

I understand SEBI came with some guidelines on PoA. If our DP made us sign PoA years back and as per rules now DP should not make sign PoA, then can we approach our DP and usk them to end the PoA now?

I had approached ICICI Direct a year or so back but it didnt work out. I have actually signed a POA with them 10+ years back when I was doing my graduation and wanted to invest. At that point of time I didn’t understand the implications. On the other hand my father had been with Karvy for decades! Luckily he switched when I started taking a keener interest.

As a reactive measure I have the usual checks and balances put in place. But nothing is proactive like they way Abhinav has suggested.

I do maintain some relationship with Zerodha but that is maybe 10% or lower of my overall capital market exposure.

Here’s a Podcast between CapitalMind’s Deepak Shenoy and Zerodha’s Nitin Kamath. They discuss the Karvy issue and the future PoA. Nitin actually mentions they are testing a beta model that doesn’t require PoA to debit the demat ac.