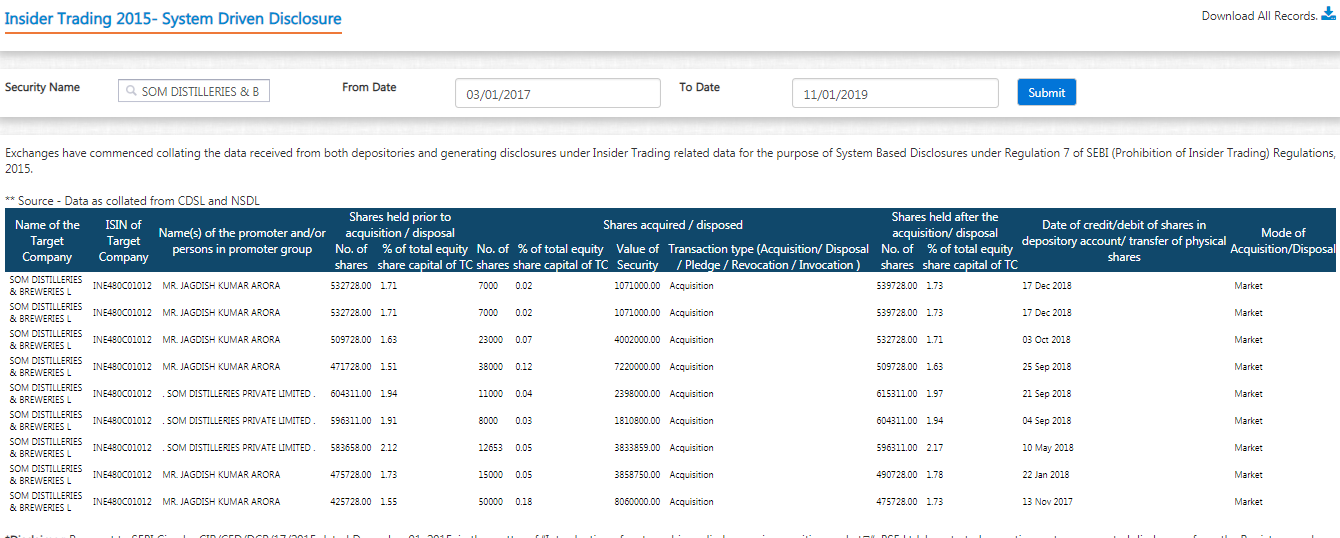

Series of acquisitions made by promotor in the open market.

1 Like

First two transactions are one and the same. Pls look at the total quantity and the percentage. All these purchases have increased his holding by 0.1%. Let us see these token purchases have anything to do with third qtr results. Historically 3rd qtr results were muted. Let us see whether this time it is different.

140cr net sales or gross sales?

Q4 is always greater than Q3 due to seasonality. Still 140cr can be good number.

140 cr gross sale can’t be good number, last quarter gross sales already 130 cr.

Net sales is net off excise duty which is 85 cr only for last quarter (45 cr is excise duty)

Generally we can see a pattern of 50% increase in revenue for Q4 QoQ due to seasonality of the bear consumption.

I couldn’t find the Q3 con call audio / transcript anywhere. Could someone pls provide me the link for the same.

Board is meeting on March 2, 2019, to consider conversion of warrants into equity shares @ Rs 271.55. Let us hope promoters take the shares @Rs 271.55.

Why should promoters buy @271 when it is available in the open market at @140 / share ?

i believe the recent upward movement in price is due to new FSSAI regulations. It appears many unorganised breweries will find it difficult to survive due to new regulations.

Could some one help me to understand the impact of conversion of warrants into equity.

Why does the SOM India gains 13% on this issue. how is this favourable to company ( or investors)

SOM promoters have taken the conversion of 12.669 lac warrants into equal No. of shares @Rs 271.55 paying the company balance 75% of the outstanding amount. This conversion has increased the promoter shares from 20.67% to 23.82%. Further they have called for an EGM on 26th Mar, 2019 to consider splitting the shares from Rs 10/- to Rs 5/-

1 Like

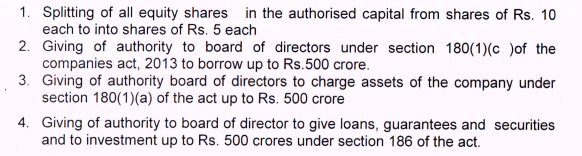

Agenda of board meeting to be held on 26th March

Why company need 500Cr borrowings further as it recently completed huge capex already.?

Are they want to give this borrowings as loan to other promoter entities or to themselves?

Disclosure:

Invested

Have been trying to reach the company secretary via email …no response even after couple of reminders. Funny part is they don’t have their own email domain …they r using rediffmail.com

Do anyone has got any info on reason to borrow Rs 500 Crore. The amount of loan is little over than the entire market cap of SOM, which makes to worry

Numbers are exceptional… Amazing growth in revenues and profit…

Hi Paresh,

I just saw Som Distilleries consolidated audited results… EPS of Rs. 7 is fairly less compared to Rs. 9.2 reported last year. Would you please elaborate how it looks exceptional. Also request senior boarders to give insight on results. Thanks in advance.

Regards,

1 Like

Funny the company has added 2 quarter results in Consolidated nos to show full year results. Seems this quarter results are 9 month results.

Financial Engineering!!!

2 Likes

SOM Dis results are puzzling. Q4 income is 108 cr on Standalone basis whereas consolidated income is 425 cr against Y-O-Y income 119 cr and Q-O-Q income 130 cr. It appears in Q4 FY19, subsidiaries have contributed an income of Rs 307 cr. The results are audited.

There is no explanation in the notes about this disproportionate additional income of subsidiaries. The published results are a poor photocopy of the results which are very difficult to read.

NSE and BSE have pushed the scrip to Z catagory. What is cooking in Som.

1 Like

Results submitted again, typing error put as excuse. A company’s MD signs the results without even looking at what he is signing!

3 Likes

Read the revised the results. Due to 260% increase in excise duties, increased RM cost , interest charges and depreciation charges, Q4FY19 consolidated results are depressed. Are the good days of Brewer companies are over ?

Based on the old results, scrip was in UC for quite some time and whether the company will compensate the poor investors who bought on old results.

Disc: Invested and no transaction for the past 60 days.

1 Like

Any specific reason why is the stock price declining recently. Any thoughts

1 Like