Business Summary:

• Established in 1993, SDBL is a Bhopal based company engaged in manufacture of beer and IMFL.

• As of March 2017, it had total capacity of 59200 KL (kilo litres) of beer and 5400 KL of IMFL.

• Its product portfolio includes beer, whiskey, rum, brandy and vodka.

• 89% of topline is derived from beer. Company has three brands that sell more than 1 mn cases (~9000 KL) per annum – Hunter, Black Fort and Power Cool.

- Sales as of Dec 2017: Hunter – 21.2 lakh cases, Black Fort – 15.6 lakh cases, Power – 17.1 lakh cases

• Hunter and Woodpecker brans are supplied as draught beet to major hotels in Madhya Pradesh and Chhatisgarh.

• A number of key expansion measures are currently underway (look at section below)

History:

• 1994 – Incorporated and listed on BSE. Black Fort and Legend brands with depots in Delhi and Chandigarh

• 1996 – Commercial production started with 10000 KL of beer and 5400 KL of IMFL, expanded beer capacity to 18900 KL

• 2003 – Expanded capacity of beer from 18900 KL to 23800 KL

• 2007 – Expanded beer capacity to 29200 KL

• 2010 – Expanded beer capacity to 59200 KL

• 2012 – Launched Power Cool beer

• 2013 – Launched Whiskey Milestone 100 and Vodka White Fox

• 2016 – SOM allowed to supply rum and beet to Canteen Store Depot (CSD) pan India

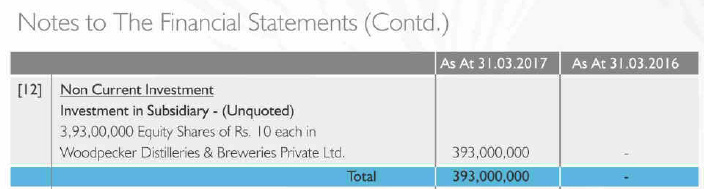

• 2017 – Set-up brewery in Karnataka through subsidiary Woodpecker Distilleries and Breweries Pvt. Ltd.

Management:

MD – JK Arora

CEO – Deepak Arora

DMD – AK Arora

Nilojit Guha – President, Sales and Marketing

Shareholding:

• Promoter shareholding – 23.17

o JK Arora – 6.61%

o Som Distilleries Pvt. Ltd. – 11.01% (JK Arora has 69.32% stake)

o Aalok Deep Finance Pvt. Ltd – 2% (JK Arora has 89.56% stake)

• Institutional holding - Nil

Industry Overview:

• Per capita consumption of alcohol in India is one of the lowest in the world – due to social stigma, high government interference and high taxes

• Beer industry is mainly concentrated in Southern states of India with market share of these states at 50%, mostly due to hot climate throughout the year. Some seasonality in sales of beer.

• Industry is strongly skewed towards IMFL. Among beers, strong beers are preferred -

- Alcohol is taxed by total volume, and not by volume of alcohol. Thus in comparison, on basis of alcohol volume, beer is taxed higher than IMFL.

- Thus IMFL has greater share (67%) in alcohols in India vs beers (26%). This is skewed compared to other countries. Beer market valued at Rs. 448 billion in 2016. Expected to grow at 8.6% for next 5 years. IMFL market valued at 2040 billion and expected to grow at 8.2% in next five years.

- Strong beers are seen as more value for money by consumers. This is in contrast to other countries where light/premium beers are preferred.

• Ban on direct advertisements and promotion imply that for a brand to become successful it has to invest in surrogate advertising such as glasses, mineral water, music items etc.

Key Developments:

• Woodpecker beer (in Mar 2017) and other four IMFL brands (in Nov 2016) allowed supply to CSD in March 2017. Entered into bottling agreements with Jagajit Industries and Oakland Bottlers in Apr 2016 to cater to CSD and Northern market.

• Launched new flavours in RTD vodka White Fox.

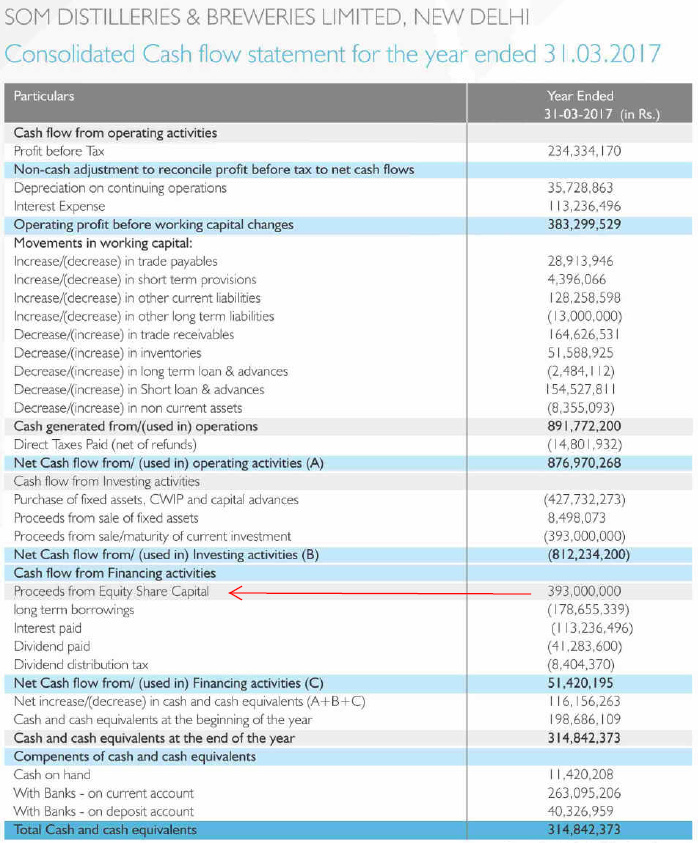

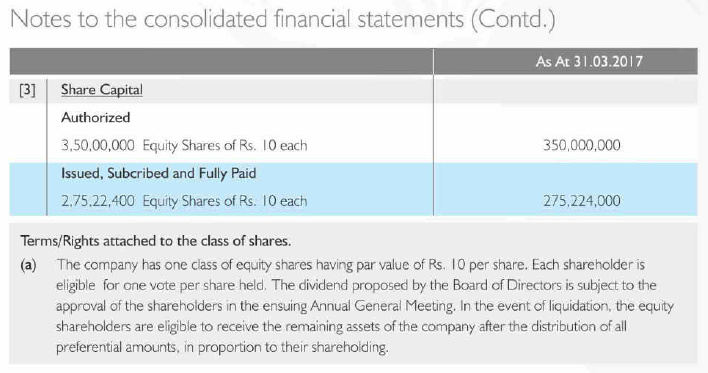

• Invested 40 crores equity in subsidiary in Karnataka. Capacity expected to go online from end of March 2018.

- Total outlay of 115 crores out of which 100 crores already incurred.

- Already started supply of Black Fort and Hunter beers in June 2017 width of distribution (WOD) of 30% across the outlet universe.

• Signed MoU with White Owl Distilleries in August 2017 to brew and bottle their craft beers -

• Entered Maharashtra market in Nagpur in Feb 2018.

• Approved decision to raise capital of 150 crores in March 2018.

- Also approved Employee stock option place to grant 5 lakh options convertible to one share each.

• Recruiting top management to strengthen sales

- Shirish Pilankar appointed as head of sales West. His last assignment was with Bacardi as Cluster Head Western region.

- Appointed Nilojit Guha as President Sales and Marketing. He was earlier Director Sales with SAB Miller. To focus on sales in Southern and Eastern markets.

• As of annual report 2017, in the process of implementing ERP across manufacturing sites and depots.

• Beer brands have been approved by USFDA for supplying beer to USA and trial orders sent.

Strategy:

• Focus on CSD and increase CSD sales share from 5-6% to 15-20%. Increase from 16 to 36 outlets.

• Diversify geographically into growth markets such as Karnataka, Kerala, Andhra Pradesh and increase sales in legacy markets such as Delhi and MP-Chhatisgrah

• Decrease seasonality in revenue from beer by increasing sales of IMFL and RTD drinks.

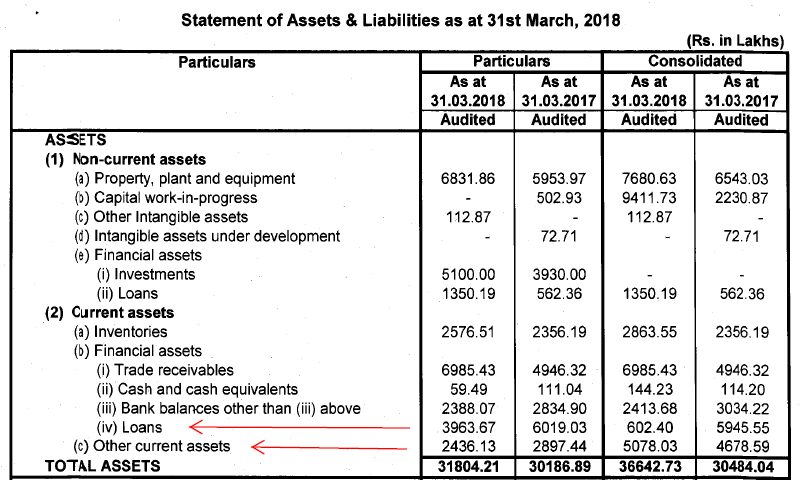

Financial statements:

Balance sheet

Profit & Loss Statement

Investment rationale:

- Overall consumption theme of beer in India remains good. Per capita consumption of beer in India is low. While this is not expected to increase dramatically in the short term, the growth of premium brands in cities is a good growth opportunity.

- Only listed player having both beer and IMFL products. These may complement each other and reduce seasonality going forward.

- Diversifying into key markets in South India (TN, AP, Kerala) where beer is widely consumed. Karnataka has 10% market share of beer in India.

- Ventured into craft beer with White Owl. I see this as a potential market with opportunity to give competition to Bira. I have personally had these beers in Goa and found them to be very good, will post pics in next post.

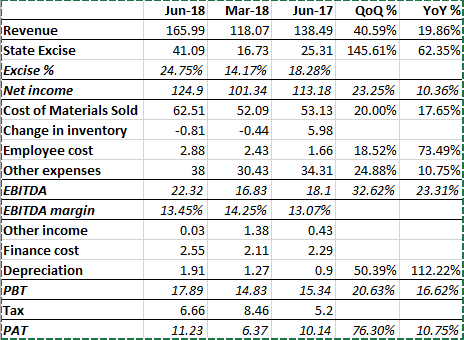

- Ability to sell to CSD is a positive. Company expects 15-20% of topline from this. I believe that is already reflecting with improved sales in last three quarters. Out of 36 CSD outlets, Som is catering to 16. Margins projected to be better.

- Few home grown brands that have successfully scaled up to become national players in beer. This is due to regulatory setup. Ability to manufacture and cross-sell in different states is a major advantage.

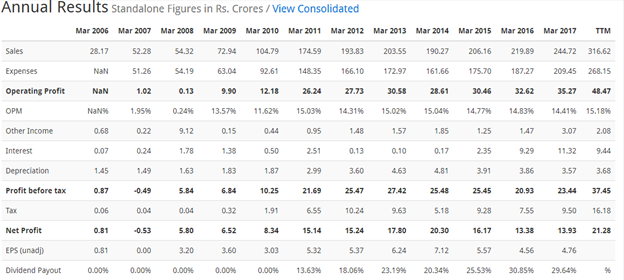

- Good financials - maintained EBITDA margins of 15% (except drop to 9% immediately after highway ban) and maintained a healthy balance sheet with gross debt to equity at end of Dec 2017 at 0.48. Dividend paying company with dividend payout ratio > 25%. RoCE at 14-16% for last 3 years.

Risk factors:

- Industry wide risks

• Highly taxed consumption item makes in unaffordable for a number of consumers.

• High regulatory interference including bans that may disrupt operations suddenly. For example, in 2017 there was scare that alcohol would be prohibited in MP, but company came out with statement what Finance Minister of MP has clarified that Excise policy of 2017-18 does not have any fix plan for prohibition.

• Unfavourable judgements such as the ban on alcohol near highways. Also the Constitution of India has Directive Principle (article 47) that states “…the State shall endeavour to bring about prohibition of the consumption except for medicinal purposes of intoxicating drinks and of drugs which are injurious to health".

• State wise differences in regulations make it difficult to market and sell across states.

• Difficulty in building a brand that catches the attention of the youth. Significant advertising and marketing costs might mar margins in the future. - Low promoter holding. Some sources say that some public shareholding is with distributors and other related parties, but this needs to be confirmed.

- Promoter was super bullish in 2013 when they said they will double sales. Has only now started improving topline. I believe projections given by promoter have to be taken with a pinch of salt. Delay could have also been to legal matters as noted in point 7.

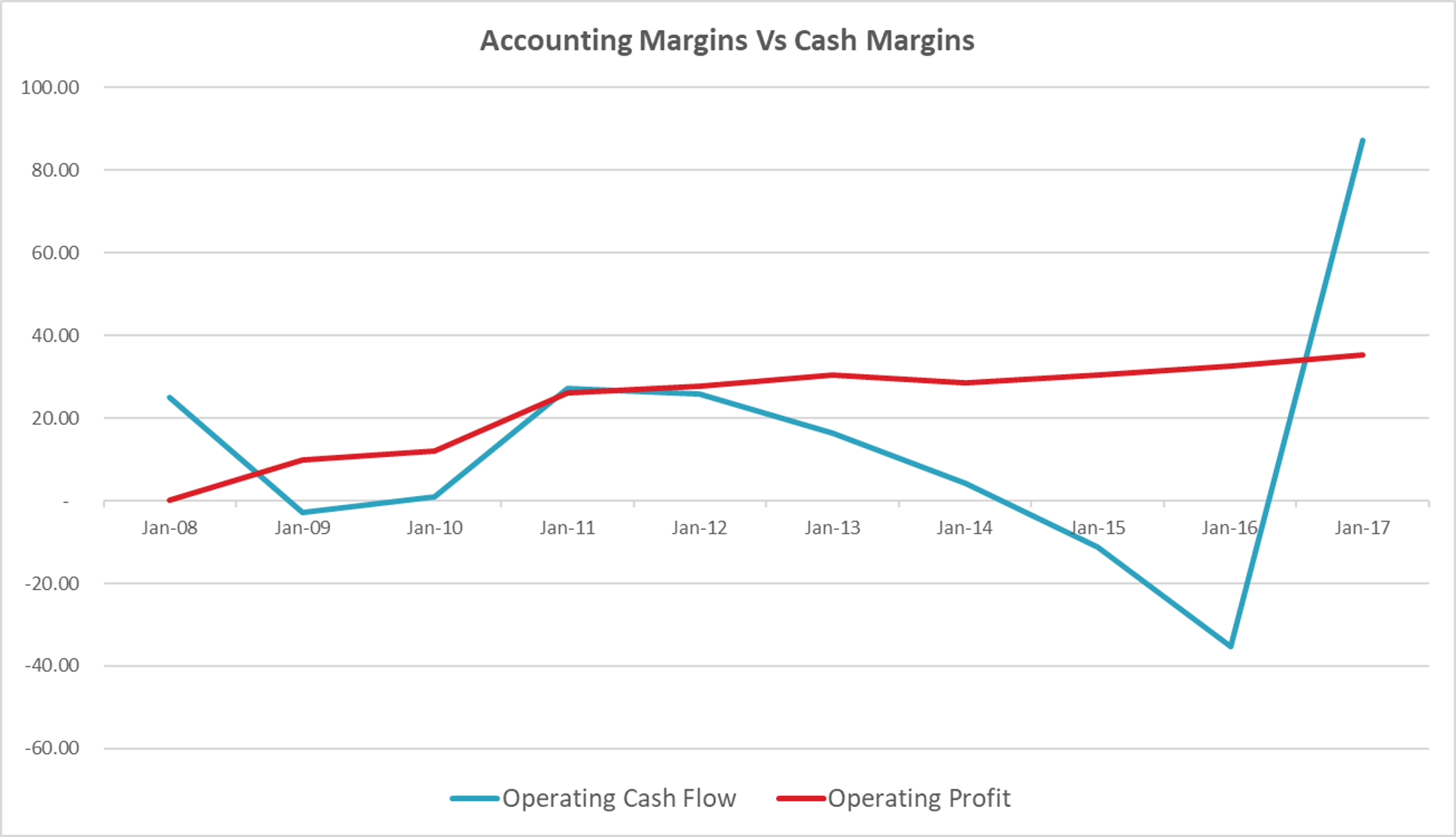

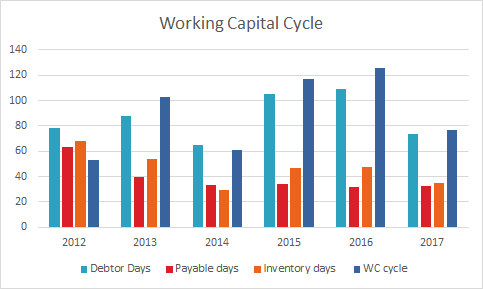

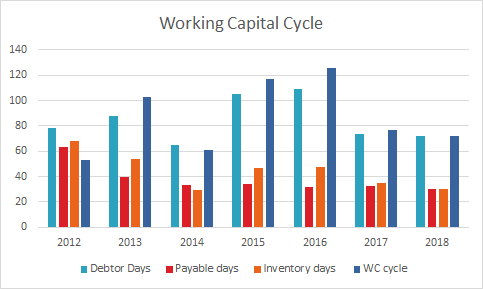

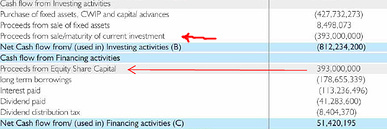

- Working capital cycle has fluctuated in the past couple of years and was as high as 125 days in 2016. Also led to negative cash flows in previous years. In 2017 however, drop in receivables led to increased CFO.

- Disputed statutory dues with respect to income tax stands at 6.38 crores.

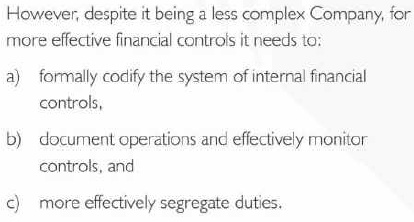

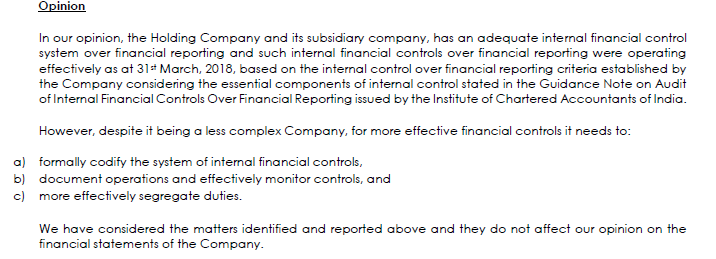

- While auditor noted that company had adequate finance control system, it suggested some steps to codify the system, document operations and segregate duties in AR 2017.

- Company has struggled with legal issues in the past. Need to check whether any cases are pending. Legal guidance in this regard will be helpful. Some legal issues found online -

• Copyright, design infringement filed by Carlsbeg and SAB Miller - Carlsberg Breweries A/S vs Som Distilleries And Breweries ... on 2 May, 2017, Formerly Skol Breweries Ltd. vs Som Distilleries & Breweries Ltd on 8 February, 2013

• Dispute over dues with MP State Industrial Development Corporation – Carlsberg Breweries A/S vs Som Distilleries And Breweries ... on 2 May, 2017. It came to a point where court asked for Som to be liquidated and then Som settled outside court. As I understand after settling issue, Som further appealed the decision as unjust – and most recent order is here - Som Distilleries And Breweries ... vs The State Of Madhya Pradesh on 1 September, 2017

Other inconsistencies:

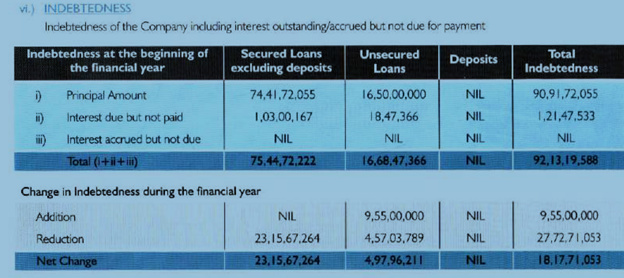

- Annual report 2017 says that interest due but not paid was to tune of 1.21 crores. Don’t understand why.

- As per annual report, CEO/MD salary is Nil. However senior management takes salary up to total 2.56 crores. This must be out of total 7.14 crores listed as employee cost. Total employees on rolls is 106.

Disc: Not holding presently.