Are they due to newly launched subsidiary? Though new subsidiary was ready by 2018 Jan, they haven’t started the operations as on the preparation day of financial i.e. March 2018. We can see difference in some line items standalone n consolidated balances sheet.

That’s the only explanation I could think of too. They said the operations commenced in April 2018, so probably they should write off the amounts this year.

2 directors bought total 12,000 shares on 21sep

Promoters have bought in Aug 18…10K and in Sep 18 32K. With introduction of new variety of beer in Karnataka and impending elections, scrip looks interesting.

A few more pointers that I noted from the AR:

-

The related party transactions between Som_Listed and Som_Pvt are to the tune of 38 Cr (Debit) and 21 Cr (Credit). However, no explanations for such transaction has been provided. As previously pointed out, the CEO does not take any salary from the listed company. So do the related party transactions in effect include the salary part?

-

In FY18 P&L, the company has recognized previous year taxes to the tune of 4 Crores. I could not understand, why would they recognize previous year taxes in this year’s P&L. Wasn’t this recognized earlier or has there been subsequent revision in taxes?

-

The number of employees and aggregate employee expense is almost equal in FY17 and FY18 (106 employees each year and 6.65 Crores in salaries). This seems a little weird because the AR also mentions that the median salary for employees increased by 8.1%

-

Lastly, the company spent about 5.5 Crores on new vehicles and 0.82 Crores on Fuel and maintenance. This seems a little high considering the company already accounts for freight outward separately (21 Crores expense recognized)

It would be great if anyone could share their views on the above.

Disclosure: Invested and looking to add more

1 Like

Where is the filing for these?

It is all in BSE notification and disclosures.

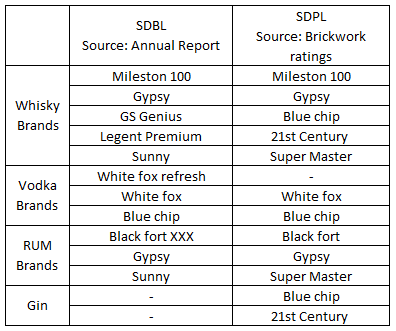

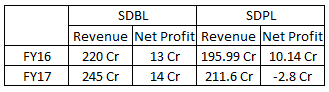

I wanted to understand the nature of business of Som Distilleries Private Ltd. (SDPL) which is a group company of Som group which may have similar nature of business like Som Distilleries and Breweries Ltd (SDBL) as their names suggest and hence the conflict of interest.

Here are my findings form publicly available information.

SDPL founded in 1982 prior to SDBL. It engaged in manufacturing of alcohol from molasses. Its product range includes Industrial spirits, Country liquor and IMFL. 74% of SDPL revenues comes from country liquor and for SDBL, 90% of revenues comes from Beer segments and hence there is no complicit in majority of their business. However SDPL is getting 19% revenue form IMFL whereas SDBL is getting 10% revenues from same segment.

Both business also have some common names in their brands hence there may be some conflict of interest.

Financial performance of SDPL and SDBL are completely different, SDPL posted net loss in FY17 which may in line with its business segments (Country & Industrial liquor)

Disclosure: Holding

5 Likes

JK Arora, Som Distilleries: Subsidiary Woodpecker Distilleries Commences Its Production, IMFL Unit To Start Its Production This Week

— BTVI Live (@BTVI) October 15, 2018

Expect Capacity Utilisation Of IMFL Unit To Be At 25%@Heeraal pic.twitter.com/24siL7IB1c

Don’t understand Arora’s point on regulator permission to increase the promoters stake.

Is there any restriction?

1 Like

Very poor results again. Sales down, margins down.

Edit/Additional point: The management’s claim that results are negative due to increased depreciation does not appear appropriate. Though the depreciation amount is up, it is not significant and therefore cannot be the sole reason for the dip in profits. The material cost seems to have been up for this quarter which has resulted in lower margins.

When the stock is trading at > 20 PE in these markets, the results should be consistently good. One weak quarter and the markets will punish the stock. This looks primary the case here.

Besides, whole of H1FY19 has been sub-optimal and therefore no surprises that stock has taken a beating.

Disclosure: Invested

Need to have deeper look before concluding things.

Looks like they shifted some of the manufacturing to Subsidiary plant. Now subsidiary contributes 16% of the consolidated sales. There can be some increase in fixed costs due to subsidiary. Same is evident if you compare Standalone & Consolidated numbers, Standalone margins are almost stable at 15%+ but consolidated margins are lower at 12.8%

Actually, sales including excise duty increased by 12.5% YoY, however there is an increase in the percentage of excise duty paid on Sales.Excise duty paid in this quarter is 30.5% of sales compared to 24.8% previous quarter and 21.2% same quarter last year. On standalone basis Excise duty paid is 24.8% compared to 18.14% last quarter and 21.2% same quarter previous year. Need to understand why there is sudden increase in the excise duty and is there any lag to pass on it to consumers.

Looking at balance sheet, there is an increase the inventories by 17%. Based on the seasonality of the business, I would expect inventories to decrease.

Is management expecting higher sales going ahead or this increase is just due to new subsidiary ?

Disclosure: Invested.

1 Like

Subdued performance was due to higher depreciation provision for Woodpecker subsidiary.Going forward, management is bullish on ramp up in IMFL sales and soft launching of their brands in lucrative Mumbai. let us see whether the management will walk the talk.

But depreciation in financial statements is not higher.

In consolidated statement , depreciation is 190 Lacs against 89 Lacs in the corresponding qtr last year.and there is an increase of 2 crores in the H1 FY19 vis-a-vis H1 FY18. But for this Net profit would have been 4.14 Cr and 16.34 Cr for Q2FY19 and H1FY19 respectively. Historically second qtr is always subdued . The only solace is their Beer brand Hunter is well received in the market and Mumbai inclusion will have additional benefits. We may expect improved results in Q4FY19 and Q1FY20 as Dec results may not be good going by the past trends.

2 Likes

Just saw Mr.Arora’s interview on BloombergQuint.

Random answers and stories with no proper explanation of why the sub-par performance. Instead, he was trying to point out that they had good performance this year compared to last year (don’t know which metric he was looking at). Despite the anchor’s several attempts to get better clarity and information regarding outlook, the guy could not answer any question properly with numbers and rather diverted these questions towards market perception about products. Guidance of about 425 Crores (Down from about 470-520 earlier) with no EBITDA margin or profitability numbers is as vague as possible.

Given the several red-flags I had found previously (already shared above in previous posts) and now two quarters of sub-par performance, lost all the conviction that I had. At > 20 PE, don’t think its worthy of risk at the moment, specially when so many quality mid-caps available cheap.

May be it is a mistake, only time will tell. But when you lack conviction, the best is to get out.

Disclosure: Sold all my holdings, so views may be biased

1 Like

Observed a very peculiar and a disturbing trend in SD.Form Jun18 Q to Sept 18Q, all shareholders,promoters plus public, having more than 1% stake, reduced their stake.It is very uncommon to see such a “united” action by key shareholders to jump out of a sinking ship.Look everyone A huge red flag.

No of shares haven’t changed but percentage holding has changed due to increased share capital.

As per today’s management note…Hunter is already available in 30% of point of sales in Mumbai and the brand is received well. Lets see how the numbers fare in next quarters…

1 Like

Beer is a volume game. Margins are less but surely with gain in the market share volume, margins can grow gradually.

there is an entry barrier in the liquor industry. But , we already have enough number of competitors in India with more foreign companies particularly in beer products. On average only 10-125% of the population would prefer to have imported drinks due to huge price gap. Hence, certainly, they are not competitors for SOM. I strongly believe, if there is a price advantage in retail price, then surely market share will be gained. Do anyone have any listing of prices in SOM’s market to check retail price for SOM’s product.

Disc. Not yet invested but may pick some tracking quantity shortly.