Dilution due to fund raise

3 Likes

Above article is more informative and talks about short to medium term plan of Solex Energy.

2 Likes

Anyone knows is there any specific reason for the fall in share price? It could be just because of broader market sell-off if nothing specific.

Management providing latest updates and guidance in the below Investor connect:

FY25 revenue guidance is 800cr, more than double from FY24. Also, the 1.5GW module line will be running on full capacity for Q4’25. By June next year, they are aiming to bring online the entire 4GW module capacity, and by mid CY26, the cell line should also begin which will be entirely captive for their own modules.

As per management, 4GW module line can translate to 4000cr of annual revenue runrate (given prices don’t fall). Their target is 9-11% margins. Cells will boost margins once available.

Disc: Invested and biased

6 Likes

Solex has released it’s unaudited financial results today for H1 FY25.

Revenue : 274 cr. (YoY 3x) (HoH flat)

Net Profit : 13 cr. (YoY 13x) (HoH up 50%)

EPS: 15.5 (YoY 15x) (HoH up 50%)

Extrapolating these figures according to management’s 800 cr revenue guidance for full FY25, Netprofit can come out to be 40cr if margins remain same.

At today’s mcap of around 1800 cr. the FY25 PE comes out at 45

But since the incremental revenue of H2-FY25 will be coming from new ~800MW TOPCon module line (operational Q4-FY25), better margins are definately possible.

This coupled with the possibility of another 100% revenue growth next year should mean good upside for the scrip.

Despite this, it must be taken into account the effect of Trump slowing down renewable energy projects in the US. If Solex’s (or any other Indian PV manufacturer) upcoming module capacities are to be fully utilized (that too at good margins), the export market to US is very important to monitor.

3 Likes

If things comes out as planned, (ie 4GW by end of first quarter next year), FY 26 top line can be 3X or 4X, not double. Lets see how the fund raising process goes on.

2 Likes

Company gave some guidance in their concall:

If they are able to make it happen it would be commendable.

Concall brief generated using NotebookLM:

Solex Energy Ltd. H1 FY25 Post Earnings Conference Call Briefing Doc

Date: November 13, 2024

Attendees:

- Solex Energy Management:

- Chetan Shah, Chairman & Managing Director

- Piyush Chandak, Executive Director

- Vipul Shah, Director

- Investors/Analysts

Main Themes:

- Strong H1 FY25 Performance: Solex Energy reported robust financial results for the first half of FY25, despite extended monsoon season impacting project readiness. The company achieved significant growth in revenue and maintained healthy EBITDA margins.

- Ambitious Expansion Plans: Solex outlined its Vision 2030, targeting 15 GW of module manufacturing and 5 GW of cell manufacturing by 2030. This includes a near-term expansion to 4 GW module capacity by June 2025.

- Focus on Technology and Innovation: Solex emphasised its commitment to adopting cutting-edge technologies, including N-Type TOPcon, back-contact, and HJT solar technologies. They are actively working on improving production line efficiency through AI and machine learning integration.

- Global Market Strategy: While prioritising the rapidly growing Indian market, Solex is also actively pursuing export opportunities in Europe and the U.S. The company believes it is well-positioned to leverage its strong relationships with both domestic and international brands.

- Financial Prudence: Solex is committed to a balanced approach of debt and equity financing for its expansion plans. They are actively engaging with investors and maintaining a healthy working capital cycle.

Key Highlights and Facts:

- H1 FY25 Revenue: ₹270 crore

- Target Revenue FY25: ₹800 crores (₹650 crores from modules & ₹150 crores from EPC)

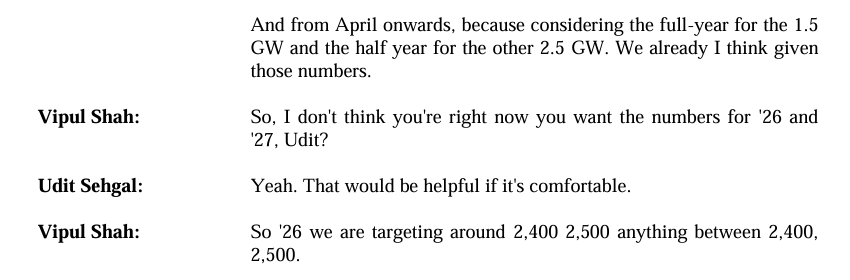

- Target Revenue FY26: ₹2,400-₹2,500 crores

- Target Revenue FY27: ₹3,400-₹3,600 crores

- EBITDA Margin Target: 9%-11%

- PAT Margin Target: 5%

- Current Module Production: 50,000 modules per month

- Target Module Production (December 2024): 125,000 modules per month

- Total Assets (estimated): ₹415-₹420 crores

- Total Debt (estimated by end of FY26): ₹300 crores

- Working Capital Requirement (for ₹1,300-1,400 crores revenue): ₹200-₹250 crores

Key Quotes:

- On Indian renewable energy opportunity: “Currently the Indian RE target is 500 GW, but India can do even 1 TW, which is 1,000 GW also.” - Chetan Shah

- On Tapi-R module technology: “Tapi-R is a new product which is actually invented by the consortium of leading global brands… the modules dimension is not majorly different… and which generates better output.” - Chetan Shah

- On Solex’s unique strength: “We are very unique that way in terms of compared to any other Indian modules manufacturer those who are larger than us and those who are smaller than us.” - Chetan Shah

- On overcapacity concerns: “I’m confident that we are not into the overcapacity. And so, whatever that India demand is, we’ll be able to fulfil it, and we’ll be able to justify our installed capacity.” - Chetan Shah

- On N-Type TOPcon technology: “Now there is a lot of improvement which has happened in N-Type TOPcon technology for the Indian climatic conditions. So I think by the beginning of '25, you will have a better product quality…” - Chetan Shah

- On U.S. manufacturing plans: “As I said, like we are comfortable manufacturing right now at present in India and supplying to USA. Once we find any good opportunity, long-term sustainable because my focus is always on OpEx part of a setup.” - Chetan Shah

Analyst Takeaways:

- Solex Energy appears to be strategically positioned to capitalize on the robust growth in the solar energy sector, both domestically and internationally.

- The company’s commitment to technological advancement, coupled with its strong financial discipline, makes it an attractive investment proposition.

- Investors should monitor the company’s progress in achieving its ambitious expansion targets and its success in penetrating new markets like the U.S.

Disclaimer: This briefing document is based solely on the provided transcript of the Solex Energy Ltd. H1 FY25 Post Earnings Conference Call. Further research and due diligence are recommended before making any investment decisions.

2 Likes

Sinovoltaics updates PV module manufacturer financial stability ranking – pv magazine International

Solex among the four Indian cos in global top 10

2 Likes

Solex Energy : Dawn of a Surya Putra ( Solar child )

Background on identifying Solex

I was researching on Solar Panel Manufacturer space due to huge capacity expansion across players and I came across Solex Energy as one interesting bet from the SME space. With so many players coming across and with each one of them announcing big expansion plans it has become difficult to identify the real winners in the space.

Recently Niveshaay posted a good decision from their Dhandho Valley event on Youtube

During the entire interview , across all the panelists what stood out was the clarity of thought process and how level headed was the promoter of Solex Energy ( Chetan Shah ) who was taking about quality / processes / technology / backward integration as the pillars for having a sustainable business.

Also Mahesh Ramanujam who in some capacity is linked with Goldi Solar , seemed to share a good relationship with Chetan Shah which further fueled my interest

**Initial Research on Solex Energy **

Couple of months back , the first media event was conducted by Solex showcasing their latest Tapi-R ( Indias first Rectangular Solar Cell with TOPCon) which claimed an efficiency of over 23%. It also unveiled the news of their Vision 2030 with plans of increasing Solar Panel manufacturing capacity to over 15GW and cell manufacturing to 4GW with an investment of over 8000 cr.

The first question was doubting the execution capabilities of the promoter ( Chetan Shah ) . From 2021 onwards , having established a currently operational capacity of merely 700 MW till FY24 we are talking over 15GW by FY30 alongwith 5GW of backward integration .

The size looks great but can Mr Chetan Shah turn this business 20x was the 1st question which came to my mind ? Whether we should stick with leaders like Waaree or move to the SME space to a promoter with unknown execution capabilities

**Industry Research on other Solar Manufacturers seeing interviews on REI Expo 2024 **

Happy realization , Solar PV Panel manufacturing is no rocket science its more of a trading business dependent completely on technology / machines from China . In the expo , what can be identified there are so many players which are introducing similar TOPCon based solar panels . So there is minimal to low technical moat with any panel manufacturer . This makes it even more essential for a company to focus on latest products / tech / ensure processes and material traceability / certifications for sustaining in the long run.

Also the promoter integrity / his ability to identify to time the cycle and ensure sustainable growth becomes all the more important.

**Back to drawing board for Promoter scuttlebutt **

- Read the Linked Profile of Chetan Shah https://www.linkedin.com/in/chetan-shah-solex/

The surprising part was he was the founder and director at Goldi Solar from 2010 to 2019 . He had grown Goldi Solar from 10 MW manufacturer to 500 MW back in 2019 before resigning from the BOD to handover the control completely to Mr. Ishwar Dholakia and family . If someone of the forum knows the reason would be great

Then he was working with Nemji Solar his own company which to my knowledge was working on EPC Projects

2020-2021 : Chetan Shah took control of Solex Energy from the erstwhile promoter and decided to start the Chapter 2 of his career with Solex. Whether the NSE Emerge listed Solex Energy was an easy way to access the capital markets is something I can only guess. But after taking over , he has increased the capacity to over 700MW by FY 2024 .

Green Flags : Experienced promoter - > built Goldi Solar from 10 MW to 500 MW till 2019 - > built Solex Energy to a capacity 700 MW in 3 years . Look at the others in the industry , most players have entered the industry after FY 2017 and here is a man who has seen the industry grow from 2009 till date successfully creating 2 big solar companies in the process . Promoter integrity and capability check

Unknown : Reasons unknown from exit from Goldi and setup of Solex after just 2 years . But in my opinion this does not count much as we do not know the motive behind the move

- Going through the Concalls

The company held its first concall on June 2024 & second in Nov 2024 . The concalls gave quite a good insights on their plans. Infact the management at Solex went at length to answer a lot of points in the first concall held in June 2024 .

However interesting point was from 1st concall of June 2024 Chetan Shah and Faruk Patel of KP Group have been industry friends for the last 10 years or so . In addition Faruk Patel participated in the preferential allotment in June 2024 with a 1% stake . Also they said that Solex was in talks with the KP Group for using Solex modules as much as possible for KP Group EPC projects from Oct 2024 onwards

Is there any basis to validate this tall claim from Solex . Lets look at the OEM & own brand sales over the last year

March 24 : OEM 70% Own Brand ( Solex ) 30%

April to Sept 24 : OEM 50% Own Brand ( Solex ) 50%

Oct 24 Onwards : OEM 20% Own Brand ( Solex ) 80%

The rapid growth of Solex own brand from 30% to 80% could indicate that Solex is now selling much more from its Own Brand rather than being a contract manufacturer . A calculated guess could be that KP Group could have started giving the business to Solex already and this has resulted in increase of the own brand sales

- Capacity Expansion Plans

Existing : 700 MW

Dec 24 : 800 MW

June 25 : 2.5 GW

- Projected Revenues & PAT

FY 25 : Rev 800 Crs ( 650 + 150 EPC ) PAT 40 cr ( 5% projected )

FY 26 : Rev 2400 -2500 Crs PAT 120 cr ( 5% projected )

FY27 : Rev 3400–3600 Crs PAT 175 cr ( 5% projected )

Asset Turnover for entire 4GW would be 3200 ( Rev from Solar Cell ) / 415 ( Fixed Asset ) approx 8 times

- Investors in their preferential allotment which took place in May after adjust of 1:4 Bonus shares which would come around 800 to 900 per share

https://nsearchives.nseindia.com/corporate/SOLEX_20072024131611_Solex_BM_Outcome_Final.pdf

1% Faruk Gulambhai Patel ( KP Group )

2% Akshat Greentech Private Limited promoters of Mytrah Group Acquisition of 1.75 GW of Renewable Portfolio of Mytrah Energy

0.22% Niveshaay Hedgehogs LLP

- Other details

Going to soon list on the mainboard . Probably Jan to March 2025 .

Summary

- Execution is key . Promoter integrity seems good : Backing by Mytrah and KP Group ensures safety as they are strategic investors who would be most likely be customers of Solex

2.Promoters participation in last fund raise gives confidence.

3.For future expansion capex planned of Rs. 280 cr with 75% debt and equity planned. Would be interesting to see the participation

Disclosure : Holding and opinions can be biased

12 Likes

Great work, You have covered everything.

280Cr is for the next 3GW module alone. Investment for celline has not discussed so far.

Adding few points…

They are on track to complete the 800MW capacity addition. they have released a video yesterday.

Solex is the cheapest solar manufacturing stock available at the moment, considering its base and growth prospects. Dont look at the PE alone. Hence, the downside risk is also minimum.

Holding but actively monitoring the demand and capacity additions in the industry. I believe the demand will top out within 2-3 years.

3 Likes

Any reason for today’s 4% fall?

SMEs can be volatile if someone sells even a few lots which should be the case. Nothing justifies the fall . Be patient

According to the management the technology partner for 2GW Solar Cell Manufacturing should be disclosed by December so probably this could be the news which comes up in Dec / Jan with the QIP which would also probably raise funds for the Solar Cell Manufacturing

2 Likes

What would be impact of ALMM list being implemented for Solar Cells for Domestic use and US imposing a tariff on modules with cells procured from China on Solex’s margins?

1 Like

The target sales till FY 26 is only with the module capacity which is planned to be scaled up to 4GW by Jun 2025. Cell line wud become operational only by mid 2026. Hence the benefit of ALMM on cell would kick in only by FY 27. The company does not derive much revenue from US as of now. Further the mgmt has clarified that thier business model insulates the company from the policies of the US govt, as they even manufactures for thier competitors as well. Hence US policies donot worry the mgmt much

1 Like

https://nsearchives.nseindia.com/corporate/SOLEX_28122024173937_Disclosure_SPRNG.pdf

150 Crore Order Received to be delivered by June 2025 for TopCon Modules

This order also implies that their new 800MW capacity due for Dec 24 , has begun or is about to begin commercial production as to my knowledge currently only the latest line is capable of manufacturing the TopCon modules

4 Likes

I believe its 15 cr, not 150:

10 million = 1 cr , 1500 /10 = 150 cr . Gemini still needs way more machine learning and proves humans are still better in calculations

3 Likes

Yeah, my bad as well. Thanks

Achieved manufacturing of recotd 65000 modules in December .

6 Likes