Found this bizarre company which is trading at a Market Cap of ~16 cr and boasts metrics for a company that should be valued at least ~100 to 200 cr. Its a microcap and as such very little information is available. I will try to do justice by giving as much information about the company as possible.

About Solex Energy

History of the company

Solex Energy was established in 1995 as Sun Energy Systems and has been in the business of solar since. They started with manufacturing solar lighting systems and solar powered boilers for very niche and small customers.

The company transitioned to manufacturing of solar panels in 2007 and has mostly conducted business in the states of Gujarat and Maharashtra.

In 2014, the company changed its named to Solex Energy Limited (transitioned from a proprietorship to a pvt limited company) and then subsequently listed itself in 2018 on NSE via NSE Emerge platform (which enables micro cap and small businesses to tap into public markets).

Products of the company

The company’s main products are PV (photo voltaic) cell modules that are main constituents of solar plants. The company also produces solar water pumps and solar powered submersible pumps.

Apart from these main products the company also manufactures

- solar water heaters

- solar rooftop systems

- installation of solar power plants (they claim to have tie ups with European and Indian EPC players in this area and have installed 110 MW worth of solar power plants globally)

Promoter of the company

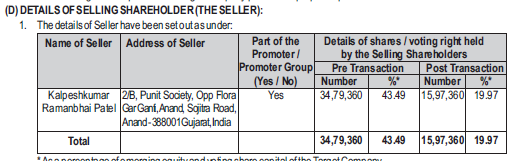

Mr. Kalpesh Patel is the promoter for the company and has been with the company since its inception. He currently holds over 70% of the company.

He seems to be exiting the company and become a minority shareholder. By virtue of open offer acquisition he has tendered a majority of his shares to the following people (who are in effect the new promoters of the company). This is likely done as the company is getting bigger and needs a more experienced team to manage it and take it forwards.

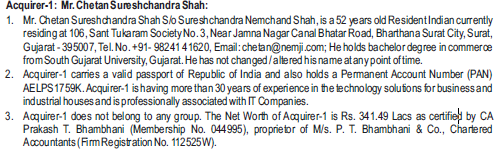

The new promoters are Nemji Solar group based out of Surat Gujrat. The group is on a solar consolidation spree and has deep pockets. The aim to invest half a billion dollars into solar PV manufacturing by 2025.

The new promoters have bought the share of the company at Rs 35 each which is more than the current market price of Rs 33 (as of 25th March 2021).

New Promoters for the company

(source: disclosures on NSE website)

Source: Leading Solar Panel manufacturing company, Anand | Solex Energy Ltd

By the Numbers

Sales: 138cr

ROIC: 16.3%

ROE: 22.2%

ROCE: 28.6%

Book Value per share: 44.8

Debt: 5.08cr

FCF: 1.95cr

PAT: 4.46cr

EPS: 9.01

Promoter Holding: 75%

Key Triggers for the company

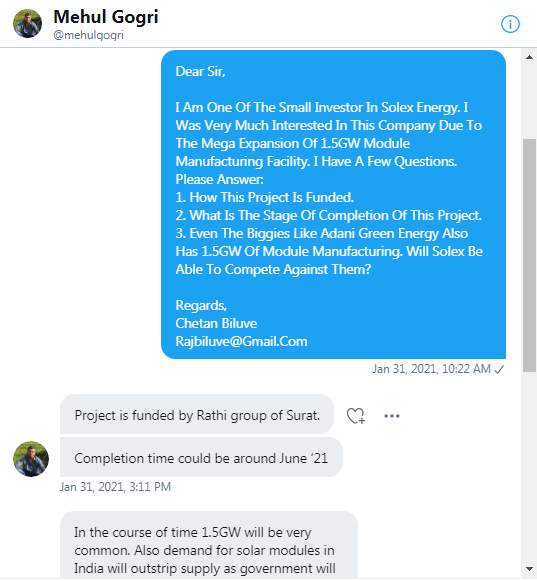

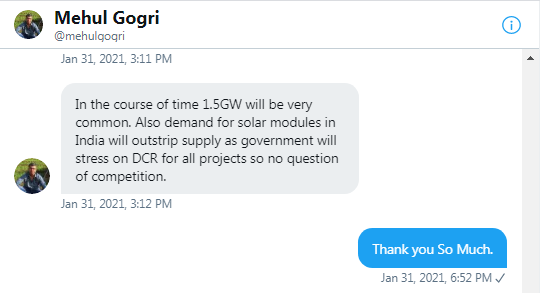

- The company has recently commenced building a solar PV plant in Surat with a capacity of 1.5 GW.

- Increasing sales (Sales have increased from 34cr in March 2017 to 138 cr in March 2020). They claim to have exceeded 200cr in sales for this year.

- Transition of PV manufacturing from import to domestic (import substitution)

- Change to a more competent management team

What I don’t like about the company

- Current Corporate Governance. Their annual general meeting was pretty much a joke (https://www.youtube.com/watch?v=5zxUNfzTBqo).

- Very little information is available about the company (I am unable to find how they are funding the capex for 1.5 GW solar PV plant). They do however share some good tidbits about the company on their website and social media (News | Latest Updates on Solar News | Solex Energy Limited)

- They are issuing a good number of preferential shares that, that need to be voted on by minority shareholders as well.

What I like about the company

- Extremely undervalued (The promoters were acquiring more shares with cash)

- Good portfolio of solar products

- New CAPEX into manufacturing of solar PV cells (1.5 GW plant)

I will keep posting more about the company as I research more.

Disc: Researching, do not hold a position in the company

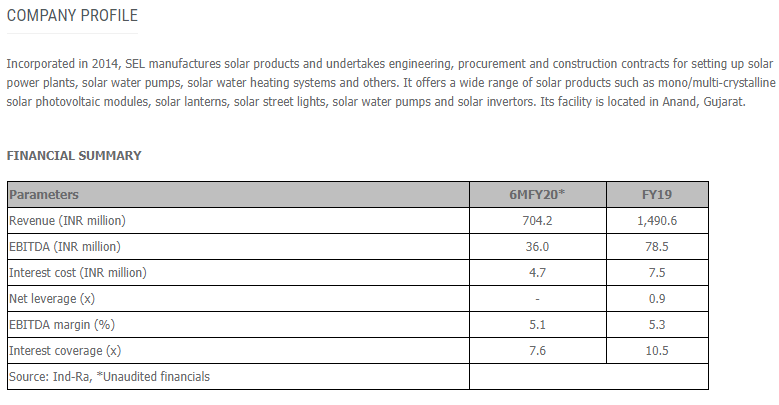

Extract from their credit report issued by India Ratings

Useful Links:

(Edit: Updated the management section of the company to reflect changes in new promoters)