Question

While there is widespread anticipation for high demand for solar modules, what is your perspective on the supply side of the equation, particularly with many players establishing production capacities in India and the U.S.?

Answer

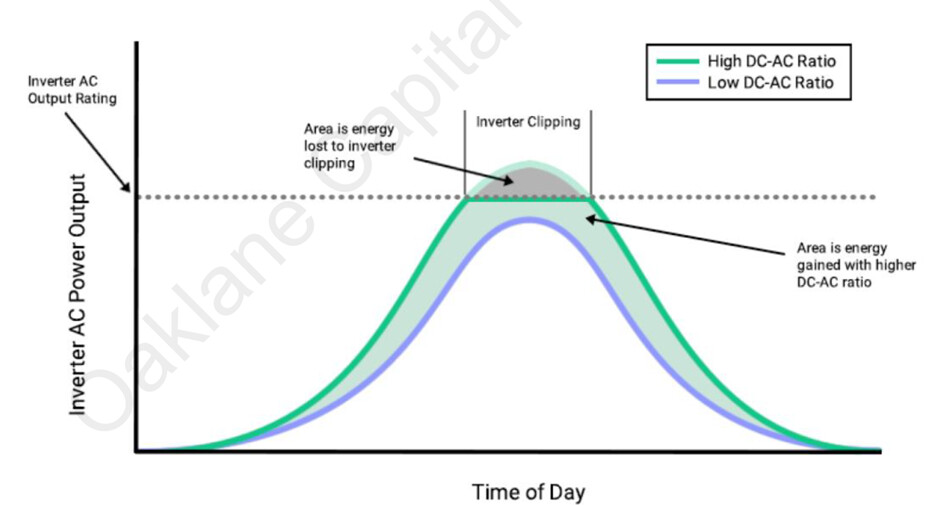

- The demand for solar modules is expected to be higher than the government’s capacity addition plans due to the practice of pairing inverters with oversized DC module capacity.

• To reduce the levelized cost of power, it is common industry practice to pair inverters with oversized DC module capacity. A 1 MW DC solar plant typically does not produce a full 1 MW of power, as solar modules operate at peak efficiency primarily during noon and only in select months. By employing DC overloading, plants can enhance generation during non-peak hours. Globally, DC overloading is implemented at ratios ranging from 1.2x to 1.6x, depending on geographical and other contextual factors.

Supply

China dominates the global solar PV manufacturing value chain, accounting for 80% or more of most parts of the production process.

In 2010, China held only around 30% of the installed polysilicon manufacturing capacity, but today that figure has surged to approximately 94%.

The wafer manufacturing stage, the most critical step in the process, is almost entirely controlled by China.

In China, for modules the effective capacity is 95%+ of the rated capacity. However, for smaller capacities like those in India and US, the effective capacity is between 70-80%, as the companies can’t have dedicated production lines for modules with different specifications.

- Due to overcapacity in China, capex plans worth $ 25 bn have been cancelled till now, however Chinese companies are setting up Polysilicon and Wafer capacities in Middle East to supply in US.

- US- We are more confident in the near-term outlook, largely due to the lead time required to build additional capacity. However, this makes the long-term forecast more uncertain.

- The upcoming election will play a significant role, as the Inflation Reduction Act (IRA) subsidies and tariff structures could be subject to change. If tariffs increase, prices will rise, potentially incentivizing additional buildout—either in the U.S. or abroad, as companies seek to circumvent anti-dumping and countervailing duties (AD-CVD).

- However, in the near term, higher prices may negatively impact demand. On the other hand, if future IRA subsidies are reduced alongside higher tariffs, the anticipated U.S. buildout may not materialize, which would likely keep prices elevated and limit demand growth.

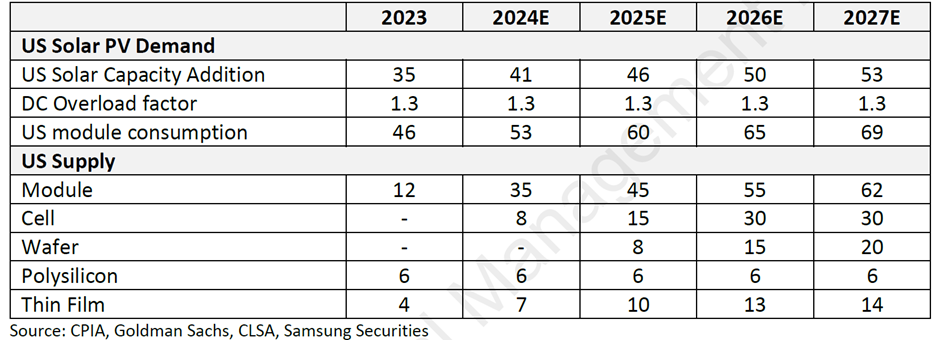

- The expected demand and supply for solar modules in US over next few years is as follows:

• While there have been numerous capacity announcements for both modules and cells, many have not yet begun construction, and some are likely to be cancelled. Any facility breaking ground after the upcoming election is expected to take approximately two years to complete, meaning new capacity would likely come online no earlier than 2027.

Additionally, some manufacturers have officially cancelled plans for wafer and cell facilities, citing financial non-viability. Notable cancellations include Meyer Burger’s 2 GW cell plant and Cubic PV’s 10 GW wafer plant.

• The solar module industry, comprising an assembly of various components, is projected to face overcapacity in the Indian market. In contrast, solar cell manufacturing is more capital-intensive, and technology driven. Current players in the solar cell sector are likely to experience higher returns over the next few years; however, by 2028, this segment is also expected to encounter oversupply challenges. At present, it seems like vertically integrated companies involved in polysilicon, ingot, and wafer production are poised to differentiate themselves and gain a competitive advantage over their peers

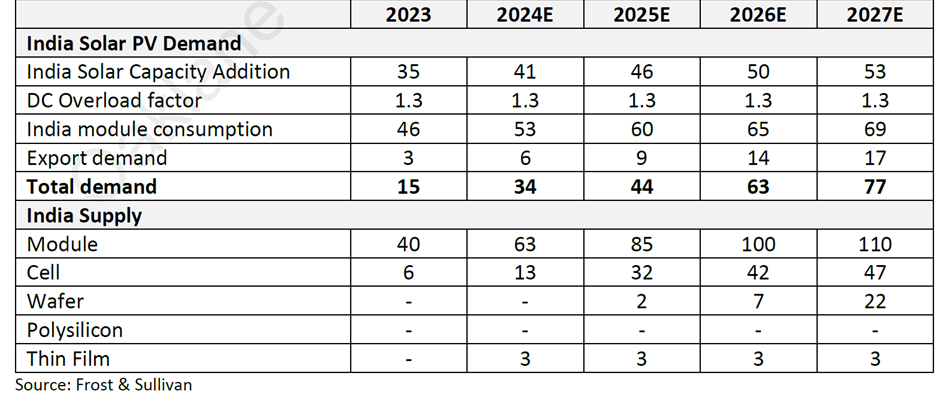

• The expected demand and supply for solar modules in India over next few years is as follows: