Given the complexities of the solar cell and wafer value chain, will backward integration in these areas prove to be a successful strategy for Indian solar companies? Companies expect margin improvement, but is this likely to be a smooth or volatile journey?

Majority of the countries are trying to build their own solar PV manufacturing facilities for energy security, the policies are also supportive of this.

Given that currently, non-Chinese manufactured components like polysilicon, wafers, cells and modules trade at a premium, we believe if the current sentiment persists the prices of domestically made wafers and cells will be higher and will support the IRRs of the companies.

How long does it typically take to stabilize solar cell manufacturing operations? Regarding the visa restrictions for Chinese experts, is it realistic for Indian engineers to acquire the necessary skills by visiting Chinese factories, or will this hinder the learning curve?

Solar cell manufacturing stabilization depends on the type of equipment ordered, if the order is given to a single credible vendor, stabilization can be as fast as a couple of months.

However, if the order is given to multiple vendors who in turn have given orders to other companies, stabilization can take 6-9 months due to coordination efforts required and resulting back and forth.

Currently, Chinese engineers are required to stabilize the cell line, over time as more cell capacity comes in India, domestic engineers might be able to learn the relevant skills. Also, the visa restrictions to Chinese experts have been withdrawn.

What are the key technologies being used in solar module manufacturing globally? Which companies or regions are leading in terms of technological innovation, and can Indian companies access and adopt these newer technologies?

Global Transition to N-Type Solar Technology- Even in China and globally, n-type solar cell capacity is still below 50%. Is this transition happening smoothly, or are there unexpected challenges that could disrupt the shift from p-type to n-type technology?

Challenges of Transitioning from P-Type to N-Type Solar Technology- What are the costs and challenges involved in transitioning manufacturing facilities from p-type to n-type solar cells? If India has an apparent oversupply of p-type capacity, is this truly the case if p-type technology is being phased out? How quickly can manufacturers shift from p-type to n-type technologies, such as TOPCon? Who are likely to be the winners and losers in this transition?

The Indian Institute of Technology (IIT) Madras has developed low-cost, high-efficiency solar cells using N-type Czochralski silicon wafers. Do you foresee such homegrown technologies helping propel India to the solar industry’s forefront?

It seems like India’s rise in manufacturing capacity is benefitting Chinese equipment manufacturers/ consultants, and India has become part of their product lifecycle, wherein we’re concentrating more on Mono PERC because of its price advantage and ease of production. On the other hand, the Chinese have moved on to TOPCon and HJT completely in terms of production because of the superior technology and their efficiency in producing these now. In a few years, India will be scaling TOPCon capacity when the Chinese move to HJT/ newer technology. Given this trend, how can India ensure it stays competitive in the global solar manufacturing race, rather than constantly trailing behind China?

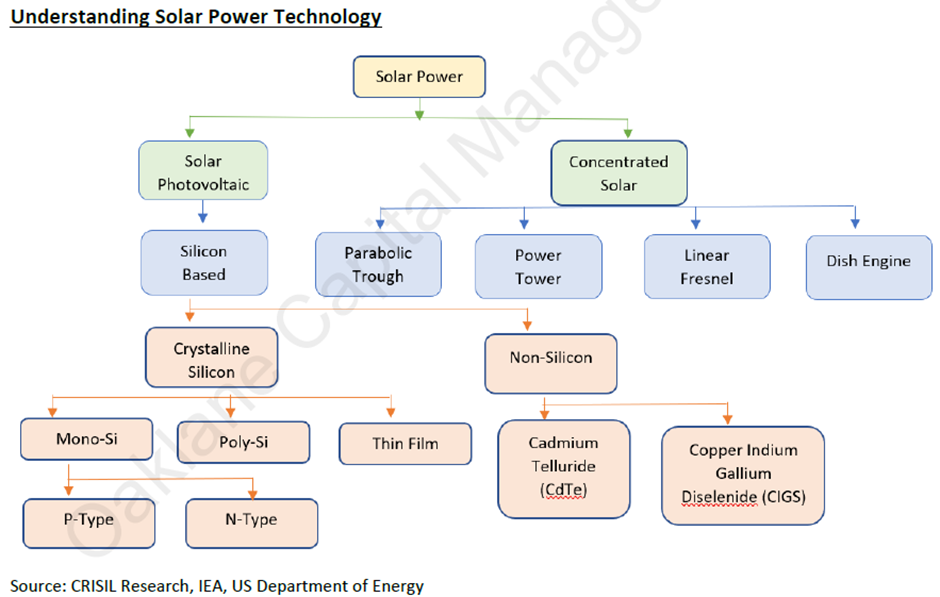

Before delving into solar PV basics, it is crucial to note two primary solar power manufacturing technologies: Photovoltaics (PV) and Concentrated Solar Power (CSP). PV, being more cost-effective, is the prevailing choice for solar power generation.

• Solar PV technology bifurcates into two primary categories based on the primary raw material: crystalline silicon-based and non-silicon-based. The predominant share, exceeding 95% of global capacity, is held by crystalline silicon, with First Solar being the only large contributor in the non-silicon-based module sector.

• Within the crystalline silicon domain, the developmental trajectory has transitioned from polysilicon to multi-crystalline and presently to mono crystalline. Mono-crystalline, particularly in N-type cells, is gaining traction due to enhanced efficiency, especially on a smaller scale, superior performance in lower light conditions, and a higher Internal Rate of Return (IRR).

• CdTe (cadmium telluride) ranks as the second-most prevalent PV material post-silicon and finds application in thin film PVs. Another material, copper indium gallium diselenide (CIGS), is utilized in the same context. Despite their cost-effectiveness, these alternatives do not parallel the efficiencies achieved by silicon cells.

• Another material which Is gaining prominence is Perovskite which is also used in thin film cells. Though the efficiencies have matched silicon-based cells in labs, it is yet to become commercially viable for large scale usage.

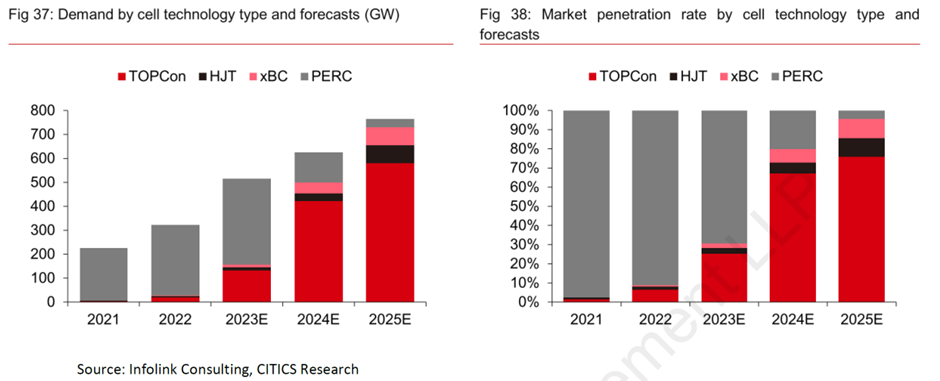

Within crystalline silicon N-type technology continues to upgrade, with opportunities in cost cuts and efficiency gains- TOPCon may swiftly become a mainstream technology in the industry, the industrialization of HJT will likely accelerate and xBC is poised for a breakthrough in the higher-end market segment.

Historically, a new technology has come every 3 years and companies have had to tweak their plant & machinery accordingly. In 2022, with super normal profits for Chinese companies, this technology cycle was faster, and they moved swiftly from Mono PERC to TOPCon.

Currently, CLSA believes solar technology innovation is progressing slower than anticipated due to reduced willingness to invest in solar capital expenditures during the sector’s down-cycle. Among the key technology introductions for 2024, only laser-enhanced contact optimization (LECO) is on track, while the adoption of 0 bus bar (0BB) and HJT technologies may proceed more slowly than expected. This situation could benefit Indian players, as capex planned around a three-year technology cycle may be extended by one to two years.

Chinese companies are the technology leaders along with First Solar for Thin Film, currently Indian companies have been doing tech tie-ups to get latest technologies. Research institutes in India are focusing on developing new technologies, however this may take its time. Waaree Energies has collaborated with IIT Bombay for R&D.

Transition from Mono PERC (P type) to TOPCon (N type) is at solar cell level, which can be done with an incremental capex of 100-150 cr. At solar module level there are no changes in the manufacturing process.

Can we expect significant improvements in solar module efficiency in the coming years, or have we reached a plateau? What emerging technologies could drive the next wave of efficiency improvements?

Companies and research institutes are working on multiple technologies to further increase efficiencies. The below chart shows the efficiency of different technologies in lab conditions.

Of all the technologies, HJT, Tandem, Back Content and Pervoskite seem to be the most promising ones, however, none of them are commercially competitive today but hopefully with the Cost curve falling one can expect more adoption as usual with such technologies

What is the market’s perception of the quality of solar panels manufactured in India compared to those from China? Can Indian manufacturers match the quality standards of their Chinese counterparts?

The feedback from customers has been a mix of Indian panels at par with Chinese counterparts and some say Indian panels are a bit inferior to Chinese counterparts. The writing is not yet on the wall but if Indian OEM succeeds in gaining larger share of global markets via exports the same will be laid to rest.

As per our understanding, Waaree Energies has got repeat orders from the same customers in US, which makes us believe their panels are of acceptable quality.

For US customers certifications of panels are very critical, as the lender would check all the documents and certifications before processing the loan. Also credibility of OEM to deliver in timely manner and guarantee performance over the contract period would be in focus from purchaser end.

Thin-film Solar: with increasing efficiency and environmental advantages, will thin-film solar technology see wider adoption, especially in the Indian market? Considering its success in the U.S. as a “100% American” alternative, what is the potential for thin-film solar in India?

Thin-film CdTe (cadmium telluride) panels are made from cadmium which is a waste product from mining industry but is highly toxic and it must be recycled. Because of its toxicity, some countries in Europe have banned CdTe panels. Also because of toxicity and lower efficiency than crystalline silicon panels, these are not used in rooftop solar, as it can also become a health hazard.

First Solar, has also setup a 3 GW manufacturing plant in India for domestic and exports market, it is also enlisted in ALMM to be able to sell to domestic IPPs. However, because of limitations of CdTe and technology only with 1 player, we believe Indian manufacturing capacity will be dominated by crystalline silicon

R&D is happening to add certain chemicals and additive to the process and success in same could lead to addressing of above concerns.

Impact of US Circumvention Duties on India’s Solar Exports- The U.S. has imposed circumvention duties on solar products from Vietnam, Cambodia, Malaysia, and Thailand, primarily based on the origin of the wafers used in solar cell production, which are often sourced from China. Although India is not currently affected, there is a possibility of facing similar duties in the future. Given that securing domestic wafer production capacity is essential for maintaining access to the U.S. market, can India sustain its competitive edge in solar exports to the U.S.?

The world needs an alternative to China in the Solar value chain. India is one credible option that is led by a vibrant democracy and trade connectivity.

“President Biden and Prime Minister Modi welcomed the U.S.-India Roadmap to Build Safe and Secure Global Clean Energy Supply Chains, which launched a new initiative to accelerate the expansion of safe and secure clean energy supply chains through U.S. and Indian manufacturing of clean energy technologies and components.” – this was a joint statement made in Sept’24 and hence we believe anti-dumping or anti-circumvention duties on Indian players is highly unlikely.

Election are scheduled in the USA next month and policies of new administration are being eagerly awaited by the industry.

Given that the modules have a 30-year warranty, but the current products haven’t been in use for that duration, what is your perspective on the reliability of this warranty, and how might this uncertainty affect companies relying on such products?

All solar modules come with a 30-year performance warranty, typically following a degradation curve as applicable to that particular technology used.

When evaluating solar module manufacturers, it’s important to consider the warranty risk. However, this risk can be mitigated by insuring the products. Insurers assess various certifications before issuing coverage, so it may be reasonable to assume that companies with insured modules are producing modules of acceptable quality.

Historically, when warranties have been invoked, module manufacturers have often replaced the panels, which can be beneficial to them due to the declining cost of solar modules over time.

The solar energy production value chain involves several technologically intensive processes, including sourcing polycrystalline silicon as a raw material and producing silicon wafers and ingots from it. Currently, only Adani Group produces these wafers and ingots in India for internal use. Waaree has no solar cell manufacturing capabilities as on date(?). It plans to set up a 6GW capacity ingot-wafers, solar cells and modules manufacturing facility at Odisha and has earmarked ₹2,500 crore from the IPO proceeds for this purpose. It takes a company around 2-3 years to set up and operate technologically complex cell manufacturing facilities and uncertainties related to the efficiency and reliability in-house production. In this context, Premier Energies, which has set up a new 2GW solar cell and module manufacturing plant, is already way ahead of Waaree Energies??. Your comments, please.

Is it a fair argument when one says Waree’s only competitive advantage right now is its demand security because of its strong export capabilities and substantial government policy support and US’s protectionist trade policies against China. Despite such strong financial performance, industry experts think Waaree Energies does not have a strong enough moat to evince investor interest like Premier Energies because it does not yet have an operational solar cell manufacturing facility. And that they would need extensive funding to develop new moats in the long run. Your comments, please?

Waaree Energies is undertaking backward integration into cell and wafer manufacturing. The company’s 5.4 GW cell line is projected to commence operations by the end of Q4 FY25, with an initial 1.4 GW capacity expected to be operational by the end of Q3 FY25.

Additionally, Waaree is expanding into complementary sectors, including electrolyzers for green hydrogen and battery storage, to diversify its business beyond solar modules. Monitoring management’s execution in these new ventures will be essential.

Current Capacity & proposed expansion-

The current operational capacity stands at 13.3 GW, distributed across five distinct plants and 20 production lines spread across 136 acres of land. The company has strategic plans to augment this capacity to 21 GW by incorporating additional capabilities through the establishment of two new plants located in Odisha, and Texas.

The maximum capacity utilization can be 85%, as the production lines have to change specifications for different orders.

A 1.4 GW Mono PERC cell line is scheduled to begin production in November 2024, with an anticipated stabilization period of 20-25 days to achieve an efficiency of 23.5%. The company has deployed 40 Chinese engineers on-site to oversee the commissioning and stabilization process.

According to management, one of the competitors took 6-9 months to stabilize their cell line, as the machinery was originally designed for Chinese conditions and required reconfiguration to suit Indian conditions. This reconfiguration process was further complicated by the challenges posed by the COVID-19 pandemic.

4 GW TOPCon cell line is anticipated to begin production by the end of FY25. The capacity also features LECO technology which enhances cell efficiency by 0.3%.