I think Kotak allows USA investing through partnership with interactive brokers

1 Like

Word of caution on US investing, factor in exchange rate and transaction charges, unless you invest one lakh or more in one transaction it is not worth it.

If you want index exposure there are some good funds like MOSL S&P fund

3 Likes

In addition to transaction charges that @Rafi_Syed mentioned. Please do note that investor will have to pay withdrawal charges that ranges between 10-30$.

It’s not even nickel and dimed out of your profits, if at all; it’s straight up extortion rates

I don’t have a target if something better comes I’ll sell to convert

Currently I am looking closely at another company, I can’t say the name yet

If I had money I would keep it in both but I now have investment in 16 odd companies and it’s difficult to keep track of all of them

Besides I am keen to keep holdings in highly liquid stocks as I am closely monitoring macro factors

While I understand one cannot know when the market has made a top, once macro factors give a signal of bubble territory I want to be in companies with zero exposure to debt, in consumer staples companies and probably some money in bonds. I don’t invest in banks as even Bank auditors don’t understand what they audit but near bubble I would get completely out of banks.

I am sorry, not an easy answer but for vipul most of the gains will come between now and until next result and possibly a few weeks after result, if they are good

If anyone is looking to sell I’d say end of May would be good time if results are good or immediately after results if results are poor and only sell if you find something better as they have a large capacity that will slowly be utilised over the years

1 Like

My big bet for 2021 is MMP Industries. Very attractive at current levels. Sharing rough notes below.

Aluminium products - pyro and flake aluminium powders, atomised aluminium powders (AAP), aluminium pastes, aluminium conductors (all aluminium, alloy aluminium and aluminium steel reinforced). - pyrotechnic aluminium powders in technical collaboration with A. Van

Lerberghe nv, Belgium (now called AVL Metal Powders nv) -

Capacity Atomized 12,000 MTPA / Flake powder 10,000 MTPA, Paste 1500 MTPA, Conductor 7200 MTPA, Manganese Oxide 4800 MTPA, Foil 5000

joint venture with Toyo Aluminium K.K. of Japan - for specialty aluminium pastes - 26% share

Star Circlips & Engineering Limited - 26% - manufacturer of Circlips, retaining rings, washers, shims and formed components mainly used

in auto and auto component industries

Aluminium Foil - Hindalco is India‘s premier foil and foil laminates supplier in different variants – plain, laminated, lacquered and printed which are used for various packaging applications - 5000 MTPA - pharma, food

Aluminium powders (pyro, flake and atomised) are used in many industrial sectors like construction (AAC Blocks) and mining (aluminised slurry explosives), agriculture (pesticides), defence (ammunition), fire crackers, railways (thermit portions) etc. aluminium pastes are used in automotive, decorative and industrial paints. Aluminium Conductors are consumed by the power sector for laying of overhead transmission lines.

The principal user segment in India for aluminium continues to be the electrical and electronics sector followed by the automotive and transportation, building, construction, packaging, consumer durables, industrial and other applications including defence.

Aluminium powder made by the Company is also used as fumigant in warehouses where grains are stored. With all government warehousing overflowing with grains, demand for this product is expected to double in 2-3 years specially with the favourable monsoon in the current year

Siporex, HIL, Ultratech (for AAC Blocks), UPL & Excel industries (for aluminium phosphides), Solar industries & gulf oil (for explosives), Coal India to name a few.

These are Europe, Africa and the Middle East. The Company’s products are now expected to be sold in Japan through it’s JV , TMI.

RM prices are passed on almost immediately, i.e. 10-15 days."

2 Likes

Current Portfolio

MMP Industries

DHP India - half of market cap in Investments

S Chand - contrary bet, positive commitment from management in Q3

NDR Auto

KRBL - catching a falling knife

2 Likes

@dn2017 – thanks for sharing your ideas. I did my independent research on MMP and it does look lucrative given the tailwinds for construction and mining sectors. The management (Mr. Bhandari) sounds very seasoned and credible – watched his IPO presentation from 2017. BTW, KRBL’s falling knife is something I too am playing with – Mr. Gupta’s bail should bring some relief.

My big bet for 2021 is Asian Granito Ltd. (AGL) – here is my thesis on AGL – I’d love to hear an unfiltered critique of my thesis:

2 Likes

I think mmp industries price already factored near term growth considering this is cyclical business

@dn2017 Hi… Could you please share your rationale behind buying NDR Auto?

I am not an expert on commodities but apparently we are in the beginning / middle of the metals rally. Steel is the darling of the market now. MMP capex is done and new commercialisation activity around foils. Could easily double from here in my view but let’s see Q4 results first.

Please do some analysis and let me know if I am wrong but I think at 120 Cr mkt cap this company is free + huge credibility of founders. The company has been setup for the next generation and so has to succeed in my view.

NACL (run by Rohit Relan and 3 sons) is a dedicated supplier to Bharat Seats Limited and is engaged in manufacture of Seat frames and Seat trims for passenger as well as Utility Vehicles.

- mcap 140cr? Cash 130 Cr - NP 20 Cr - Bharat Seats 28% worth 80 Cr - demerged from Sharda Motors - Other Income 9 cr a year (interest / FD)

- demerged from Sharda Motors (now controlled by Ajay Relan) - owns 28.66% stake in Bharat Seats (Rohit Relan and Maruti JV - Bharat Seats Ltd is a joint Venture of Suzuki Motor Corporation Japan, Maruti Suzuki India Ltd, Rohit Relan and Associates with the aim to manufacture complete seating systems and auto components.) / - has 95cr cash 0 debt + 30 Cr Investments

- 73% promoter stake. No pledge

- 2 plants - has 50% in JVs with Toyota and Toyo

7 Likes

Cash & equivalent as per last AR was arnd 95 crs. only. The stake is arnd 60-70 crs & NP inclusive of other income was 6 crs. only. Frm whr did u get 20crs. net profit & 130 cash?

1 Like

Thanks for bringing this up i did a detailed analysis to the best of my knowledge and skills , it definitely is undervalued at cmp but i want it to be a value buy and not a value trap .

what i learned

It is a newly incorparated company so past records are not available but one can see the track record of bharat seats of which Rohit relan was M.D to get a rough idea about the promoter , auto being a cyclical business is not doing very well ATM but there is strong recovery and bottomline back to precovid even all time high of 2018 in the last quarter for bharat seats but one has to observe if this can be maintained .Also the fact in annual report (page 37)one can see contracts which are repetitive in nature but all are from the associate or holding companies roughly amounting to 100 cr eyery year (out of which 96cr are from bharat seats )at current 7% margins gives 7cr of revenue from operation for 33 cr value of plant according to the latest balance sheet which is pretty high as mentioned by you is a company setup for new gen. So one has to track how is bharat seats doing , how the company utilises cash ,can get new customers other then the only existing associate company.

company also mention of reducing cost and getting new customers through bellsonica but google shows belsonica has same customers(maruti etc )which bharat seats has.So one lso has to track how belsonica is doing .

One thing which is i dont like is the salaries of 2 sons Pranav and Ayush is 4.5 lakhs per month each amounting to 1.08 cr no mention of salaries of Rohit(father) and Rishabh(3rd son) which is pretty high for company with expected net profit of 7cr and there are other salaries and 10% increment every year as well.Which imho is not a very good sign as it doesn’t inspire confidence for small retail investors like me.

the company does seem pretty undervalued with 5cr in cash in hand ,91 cr bank plus 9cr intrest income(assuming all other income as fd intrest),then there are investment in holding companies .i might just get a tracking position but i will wait for 2 more quartes for results and annual report ,how bharat seats , ndr auto and auto sector as whole is doing to decide whether to invest or invest if there is more market correction and the stock becomes more undervalued.

7 Likes

Both of u guys did gr8 wrk to uncover this idea. Kudos…  . Its rare to find a co. selling for less thn cash + investmnts in this roaring bull mkt. 1 more kicker here is the probabilty that majority of spin-offs outperform the mkt.

. Its rare to find a co. selling for less thn cash + investmnts in this roaring bull mkt. 1 more kicker here is the probabilty that majority of spin-offs outperform the mkt.

However, wat r ur views regrdng the customer concentration risk? 100% of revenues cm frm one customer. Wat r the plans, if any for customer diversification?

1 Like

Excellent analysis on NDR autos. I started to read about the company and it’s associations with a stake in Bharat seats. A simple yet complex question which raises is that of the same business. Why would a company already having a stake in Bharat seats open a parallel company with the same business model. Is it not a conflict of interest case scenario?

Thanks in advance

4 Likes

Hello everyone. There is one interesting small/micro cap called Raghav Productivity Enhancers. Please do have a look. In case any one is interested in doing collaborative research on this company, please send me a message. Thanks!

7 Likes

Hi @edwardlobo

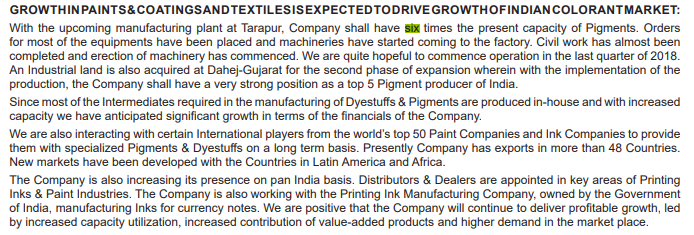

Just wanted to discuss Vipul organics expansion here, looks like 6X capacity expansion is just related to “pigments” and not the entire suit of the products which they offer.

In AR FY20, pigments contribute 45% of the total turnover. This shall effectively mean ~3x total capacity expansion? Is my understanding correct here?

3 Likes

You’re probably right

Any expansion if utilised is good use of funds, there are some companies that go into expansion just because their competitors are expanding

However, I have reduced my exposure in vipul organics and have increased my exposure of vinati organics as I like vinati’s better margins and probably higher utilisation of their new capacity after a recent interview by vinati ceo

Vinati also seems to be a forgotten company in the recent bull market as there was nothing extraordinary in their quarterly earnings. That might change this quarter report and my bet is on that possibility.

If it doesn’t give a good quarter I know the share price won’t go much down as most of the sellers seem to have finished their selling.

The thread on vinati on this forum also has a lot of negativity or absence of ramping

Buying a stock when no one wants usually is rewarding although it was more unloved when I first highlighted it a few weeks back on this thread.

It’s since up around 20% but another interesting feature has been in this mini selloff vinati has been holding up well and actually advancing

So possibility of good quarter as per ceo, expansion not priced in, making ath during market weakness are all positive signs and gives me a confidence to add to my position

Vinati margins are very good and the markets usually don’t want to see a big improvement in numbers to give the stock an over average price increase compared to stocks with low margins, markets like to see a much higher performance increase in quarter numbers.

This also makes fundamental sense as a company with better margins has a better moat and hence a better ability to protect that growth going forward. A lower margins company might lose the growth to a competitor.