I have started that thread, but not got any response on it ![]()

Had created a thread on this at SG Finserve - is this birth of another Bajaj finance? - #2 by ShareFarmer however it was closed.

I am betting more on the promoter and their almost guaranteed customer from APL Apollo distributors and vendors. The other big opportunity is anyways there as they are targeting the complete supply chain ecosystem for their lending.

Disc: I am invested

1 Like

It passes most of my checklist points. Considering it but dint buy because of the subdued revenue growth. While their direct competitor Gravita is growing at 25%, POCL is forecasting a 10% growth for 2 years running. Although they have big plans and targeting a 30% CAGR growth in revenues till 2030.

Will look at it again based on Q1 results or if the Lead cycle reverses and it impacts the margins.

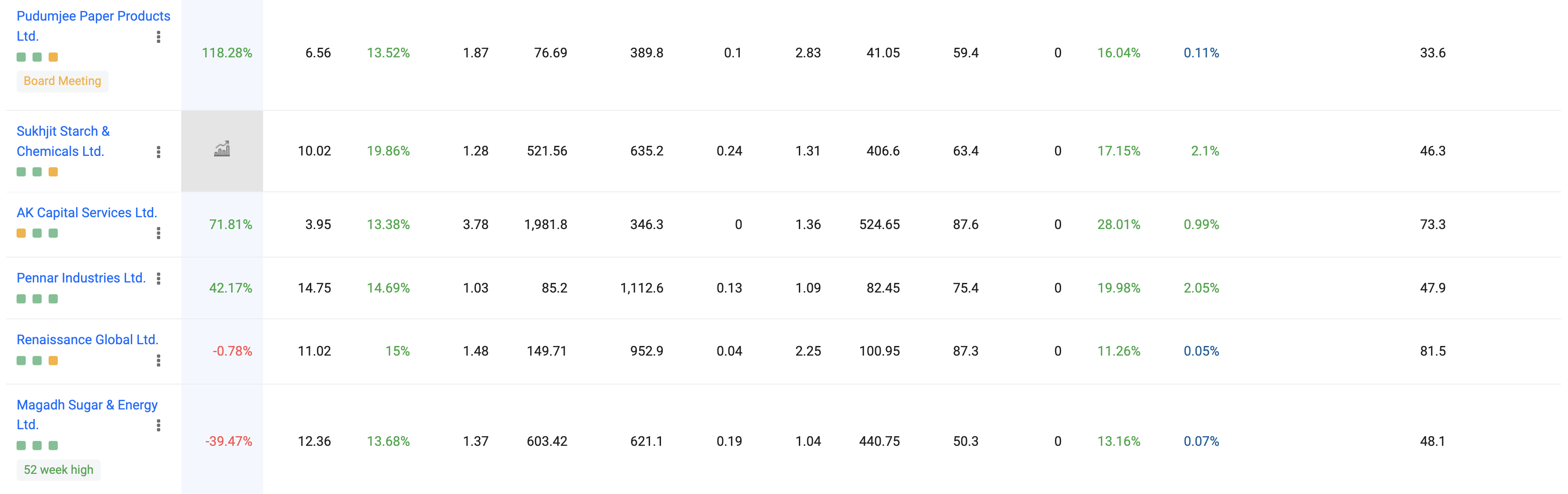

Make sense, what interested me was that I was running a small-cap screener for companies with the

following filters

`

Long Term Debt To Equity Annual < 0.5 AND PE TTM Price to Earnings < 15 AND Promoter holding pledge percentage % Qtr = 0 AND Market Capitalization in Cr < 1500 AND ROCE Annual % > 10 AND Promoter holding change 8Qtr % > 0 AND NetProfitAnnualAveragePrevious5Year > 30 AND FreeCashFlow4YearAverage > 0 AND Market Capitalization in Cr < Total Revenue Annual avg 5Yr Cr

`

This gave me some interesting names, and Pondy seemed the most interesting.

DISC: Invested.

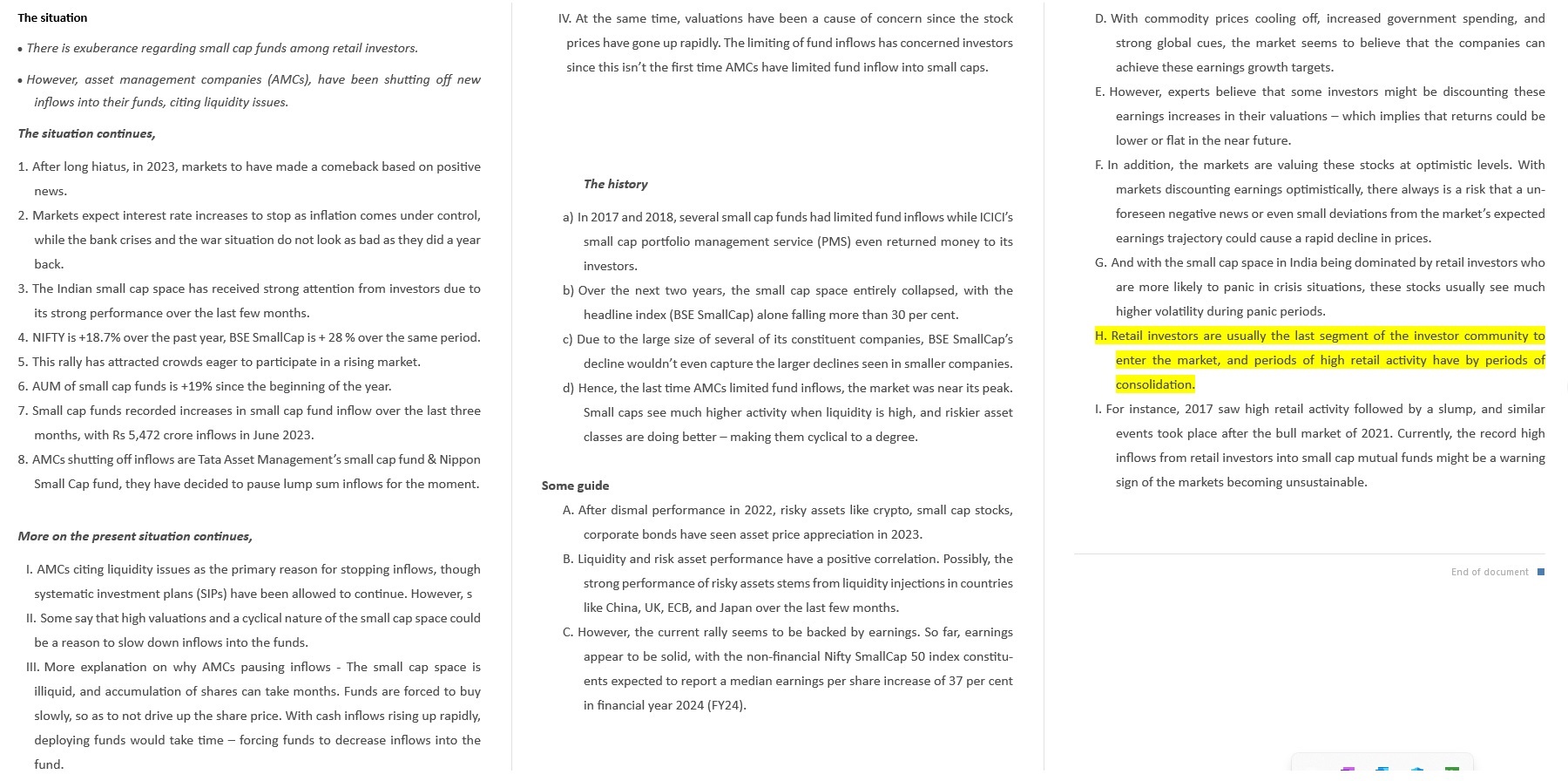

I have tried to summarize the article IsaacAsimov mentioned, pls pardon my summarizing skills.

I would be curious what experts make out of it , I can only relate myself to “H.”

How hot is small cap space and if it is time to shift to large caps ?

2 Likes

Why can small caps still keep rising?

-

The current rally in smallcap space is too strong. If you look at BSE Smallcap Index, it started rising from 29 Mar 2023. Till now, it never has touched 20EMA once. It is not even taking minor corrections to take some rest.

-

The current PE ratio is 27 which is not too high from the perspective of smallcap index. It was trading at 114 PE in Jan 2018 peak. Maybe there is still time before we see some heavy correction.

Reasons to worry:

- The AMCs have stopped taking money. They are running out of ideas to invest in.

13 Likes

NPST

Established in 2013 Network People Services Technologies Limited (NPST) is a Fintech Company focusing on Digital Payment Solutions like UPI, IMPS, Mobile Banking & Wallets to Banks and Payment Companies. NPST operate as “NPCI Approved Merchant PSP” digitizing Merchant acquiring space under the brand name of "TimePay”. Currently, the company is providing its services under two verticals i.e. Technology Service Provider (TSP) and Third Party Payment Application Provider (TPAP).

Technology Service Provider (TSP) (For Banks & Financial Institutes)

- Switch Products IMPS | UPI | Mobile Banking Solution (Revenue model: Licensed model)

- Super App – integrated Mobile App for Banking services (Revenue model: Pay per transaction)

- Qynx – Merchant switch (Revenue model: Subscription): Qynx is a Digital Merchant platform for banks that provides a complete suite of services and products to manage and operate Merchants of various sizes and categories. The solution provides an end-to-end product stack to digitize your merchant network and increase revenue potential through digital offerings. A must-have product for banks & fintech to create merchant stickiness to acquire new business.

Third Party Payment Application provider (TPAP) (For Payment Aggregators and Merchants)

- EVOK - UPI (API) engine (Revenue model: Pay per transaction): TimePay Evok is an API-based Payment platform empowering businesses with the flexibility of real-time UPI transactions and innovative payment channels integrated with the reconciliation module. Delivering UPI payment solution being one of the approved TPAP.

- UPI plug-in

- Payout solution

Even if you don’t want to invest please go through its latest presentation once. It looks like an amazing company with an exponential profit growth model.

Latest Investor Presentation

Problem: Since it’s an SME, can buy only 400 shares. The minimum investment is 4Lac. Most of the time stock is in UC. Current MCAP: 650 cr.

6 Likes

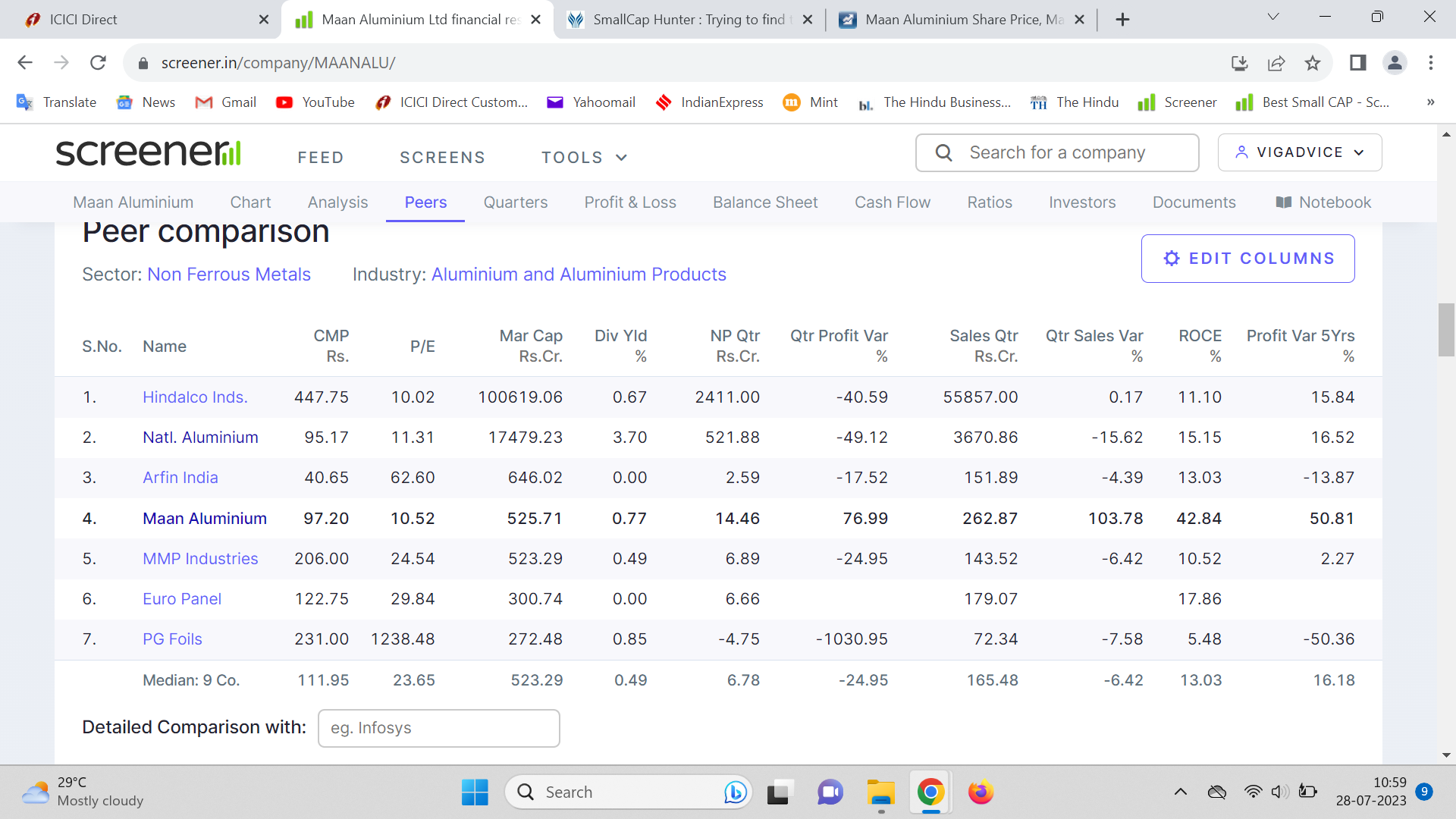

Maan Aluminium

In comparison to the other aluminium companies, its financials appear better. It has split the share and given a bonus a couple of days ago, practically dividing the stock into four parts.

Disclaimer: Have a small holding.

2 Likes

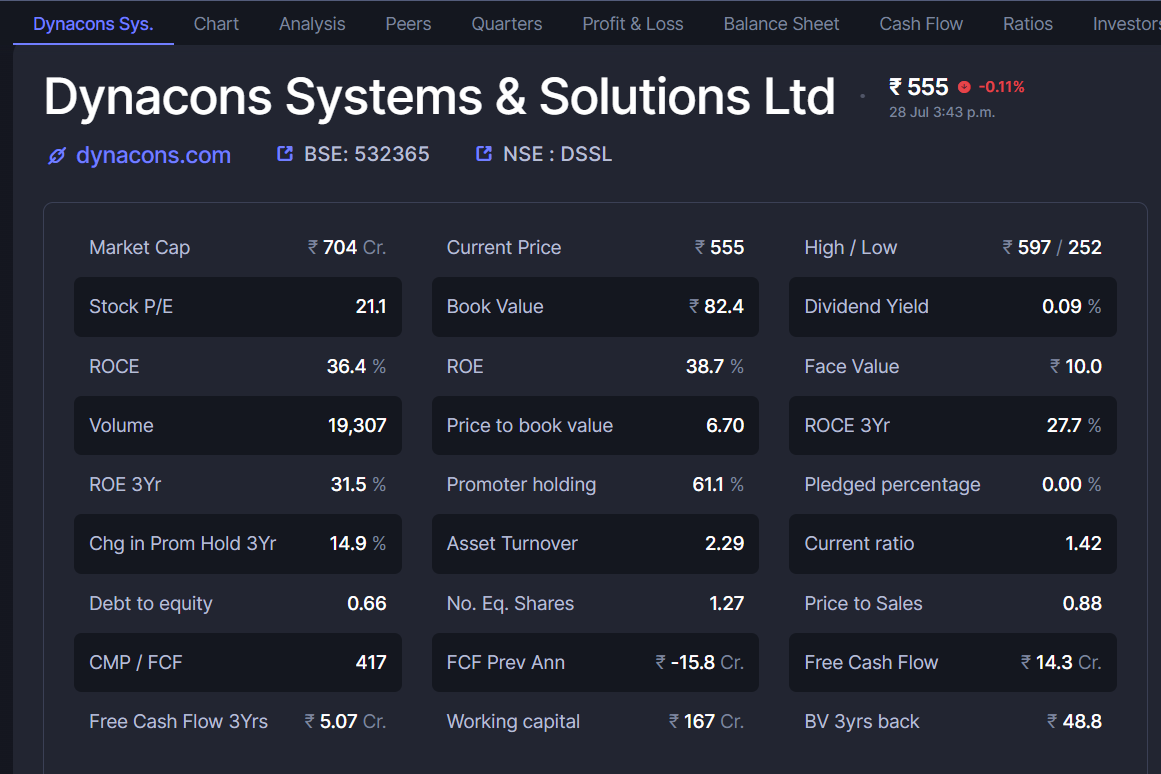

Has anyone looked into DSSL ? Dynacons ?

Sharing a screenshot of the fundamentals.

There is a thread for the same here on VP.

Did not see this name being talked about, hence I shared it.

Disc : Invested.

1 Like

While Dynacons operates in an interesting sector and the topline and PAT growth have been impressive, I had the following concerns:

Low margin business

Receivables makes up 75% of assets on the balance sheet

Cash from operations has been consistently poor

Hence didn’t invest.

5 Likes

Yes, those are indeed the stand out points when looking at the company.

But that all broadly makes sense when you consider 2 major points :

- Small Company.

Almost all names are bigger, Im guessing at least double in size of this name. - Legacy Business but Private Clients + projects are long term.

Now, what made sense to me what how the company is winning deals. You can check the frequency of deal wins, and its a good flow for a small company, and the clients a huge.

I have no idea what the management does to win these deals, but they do win them.

And don’t you think they’d want to keep winning them ?

So, as long as they keep winning and improving on their client interactions ?

It is good. The company can grow.

Receivables, for them to be good, the company’s position in the value chain matters, small companies do suffer this way. Big inventory, Big Receivables, Big deal win timings etc.

“You need me, more than I need you” mentality is anyways prevalent in the Indian business environment (I have other businesses, hence speaking from experience). This also impacts the margins, but they have been growing. It was ~3% and now its ~5%.

The more it grows, the more it has a say in terms of pricing power, receivables and more.

For me its about the management. I keep seeing those "Deal Win’ updates ? its nice.

I AM INVESTED.

3 Likes

Isn’t its PE at 61.1% rather disconcerting?

NPST, PE at 61

Yes, currently it’s overheated. It’s best to wait for a correction. But what I could understand from their Presentation is once the software is sold, revenue will go directly to the bottom line. In pay per transaction model the increase in UPI payments won’t require additional investment/infra on their part. It might be valued as a software product company rather than service based company.

2 Likes

https://www.screener.in/company/542753/#shareholding

Modus operandi: Management announce some short of tie up or differed tie up (https://www.bseindia.com/xml-data/corpfiling/AttachLive/8034b696-6cbd-4ba6-bbc7-c0384fe4e348.pdf) < sale their stake < retail buy it in search of multibagger.

Disc: Retail investor - not sebi registered. Not buy sale advise.

3 Likes

Any idea why Lykis still falls? I have invested here. Seems results of Q1 are not that bad as it is beaten even after a 50% fall.

1 Like

I think more than their quarterly results, ever since the stock was placed in ESM restrictions (which I never understood SEBI’s logic), the stock has been swinging up and down.

1 Like

Any thoughts on promoter stake reducing from Sep 22 onwards? Rohan Gupta has sold 385000 shares on 31st Jul also. Thnx

0.1% is too low to move the needle, waste of time and effort…atlease 2-3% is good otherwise at portfolio lever nothing will change…

due to Q-Q comparison, however Q1-Q1 it has done well, give one more Qtr and see.

i’m very optimistic on the counter.