Thanks Spiderman for the inputs. To add to your points, just over a year ago i was told by an employee of a restaurant chain running on eggs theme based out of India, Malaysia and Singapore (i remember the name as eggfactory or similar) that SKM was trying to buy a stake in the restaurant chain. However, they were put off by SKM asking for a controlling stake.

Company is a commodity play. From the approach of the manamgnet it looks like Entire B2C Benefit will go to Unlisted Entity.

25 Years of Excellence in the making

3 Likes

Falling egg prices has come as good news for SKM Egg Products, which makes value-added goods such as egg powder, pasteurised egg liquids and bakery mixes. It procures 700,000 eggs every day in addition to its in-house production of one million daily. But the stock price of Asia’s largest producer of processed egg products is down by 14.6% from 31 on February 20 to 27 on March 24. Besides the pandemic scare, the stock has been under pressure over the past three years owing to inconsistent earnings growth. It fell from levels of 180 in January 2016. SKM promoter and MD Shree Shivkumar explains, “Our average price realisation and margins have come down due to the heavy duties we have to pay in Japan as an Indian-origin company. There is a stark difference in the duties paid on eggs produced in EU and India. This has affected our bottomline.” Since Japan and Russia are the company’s largest markets, its net profit fell from 226 million in FY16 to 17.9 million in FY17, further falling to 9.6 million in FY18 (See: Sunny side up).

Now that the bottom line is once again on an uptrend — at 60 million FY19 and 40 million for 9MFY20, Shivkumar is optimistic that the current crisis will not dent its financials. He maintains that there hasn’t been any decrease in demand, since most of the business happens through prior contracts for three and six months and one year, on rare cases. The company accounts for over 50% of the processed egg product exports from the country. “Around 70-80% of our export business happens on a prior contract basis. Only 20% of it is on spot. At present, in Russia we are covered up till December, and till June next year for Japan,” he says. In fact, exports makes up for 95% of its total revenue. SKM Egg has a market share of around 10% in Japan where the dominant suppliers are from Italy, so he is expecting an additional demand from this quarter since the Mediterranean country has been severely affected by the pandemic.

In India, the largest share of its sales comes from whole-egg liquids, which are supplied to big bakeries and hotels chains such as Taj and ITC. After GST, margin from these sales has improved with the tax coming down to 5% against the earlier 20-23%.

SKM Eggs will be investing more into expanding its in-house egg producing capacity to at least 70%, over the next seven years, with a capacity of housing two million birds. To protect the business from fluctuating feed prices, the company recently received the necessary clearances to import feed.

Manish Srivastava, equity research analyst at Pace Stock Broking, which is one of the top ten shareholders in SKM Eggs, says, “The company can eventually be a good alternative to Venky’s at a cheaper price.” Currently, SKM is trading at a PE of 14.74x against the 10-year highest of 309.24x in April 2018 (priced at 112) and the lowest of 13.12x in July 2019 (priced at 30).

3 Likes

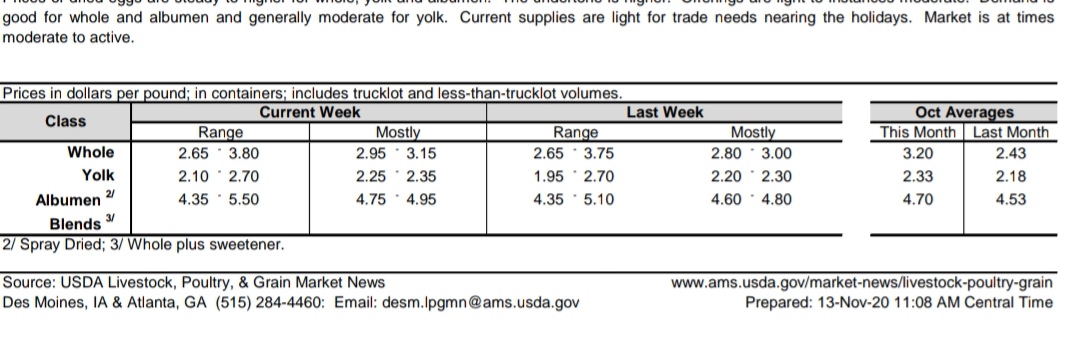

Eggs prices from NECC website. Oct prices up by 20-25% against the avg.

https://www.e2necc.com/home/eggprice

and so is Soya prices which is one of the key raw material

Ovobel Foods Peer group company of skm eggs is getting acquired at 50 to 60 Crore valuation

https://www.bseindia.com/xml-data/corpfiling/AttachHis/54239E3F-F4D2-4CC4-98D0-84F47DD601BD-201208.pdf

SKM which is doing sales of 300 Crores (Ovobel 100 Cr) getting lower valuation because of lack of transperency. Ovobel doesnt own Poultry farms & Feed but still performs better than SKM.

Ovobel ratios are very good.

More important is egg powder cycle is turning good. in next 2 to 3 Years skm should deliver strong number. (cyclical play)

3 Likes

Prices continue to rise. Lets hope skm delivers in H2 also

H1 eps is around 3.7 rs. Full year eps should be 8.

Based on previous experiences and commodity cycle we can consider 10 PE alone…

Fair value can be 70 to 80

2 Likes

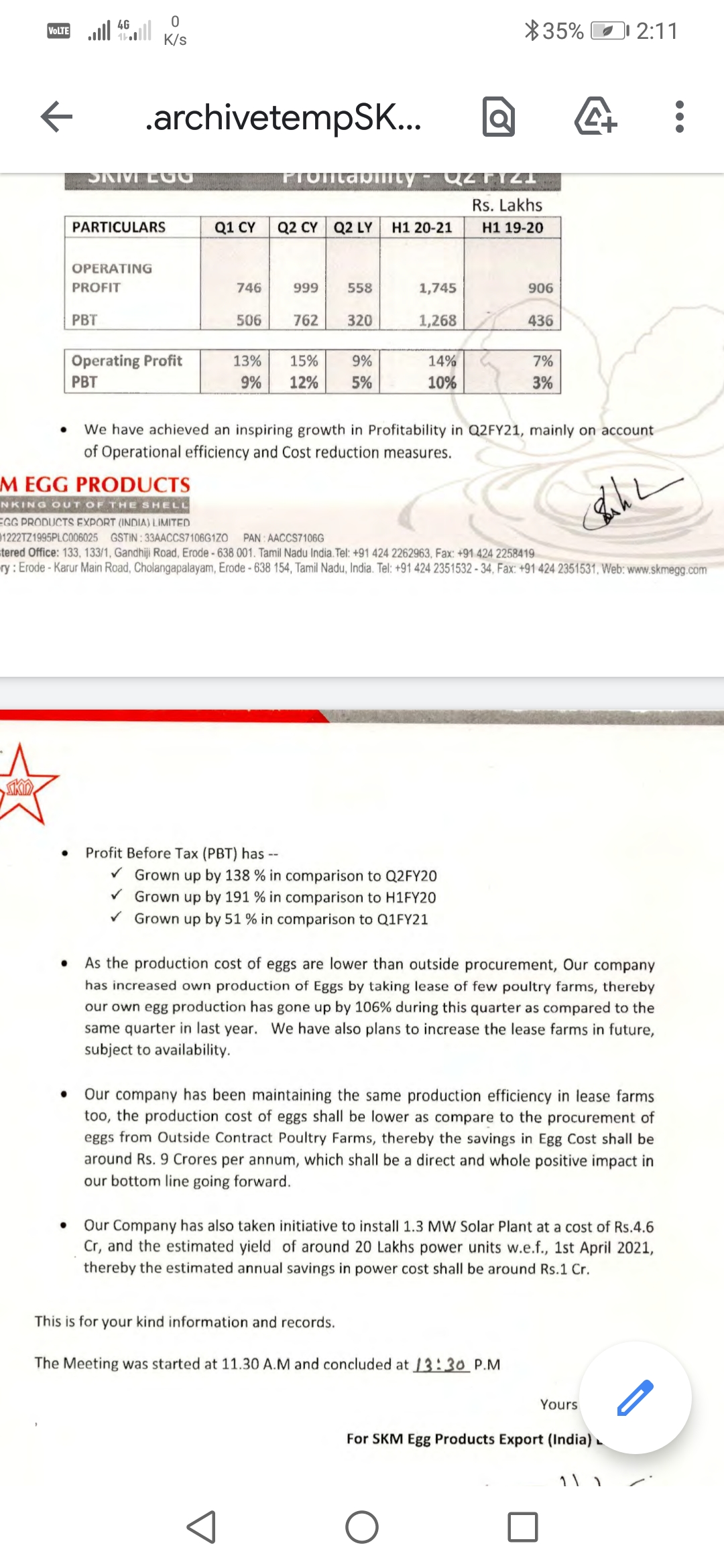

Results are good,Dont understand why depreciation figure is so High (4.12 Cr).Else PAT figure would have been much better . Going by the OPM 10% , looks like egg cycle is on the upmove & next 1 year’s gonna be great ,provided the Management doesn’t play spoilsport. Q1 FY22 again looks like there will be lockdown impact on Sales but they seem to be holding good inventory.Technically also chart looks great on Daily & Weekly,above all moving averages & RSI moving up.Golden cross awaited on Weekly post which it’s gonna blast.maybe in 2 weeks

1 Like

promotors are not Honest.!!!

8 Likes

Big order from Russia.

1 Like

Export to UAE

Egg powder prices in USA, Russian market should trade at some premium. Skm tend to benefit

Promoter Integrity is a big question

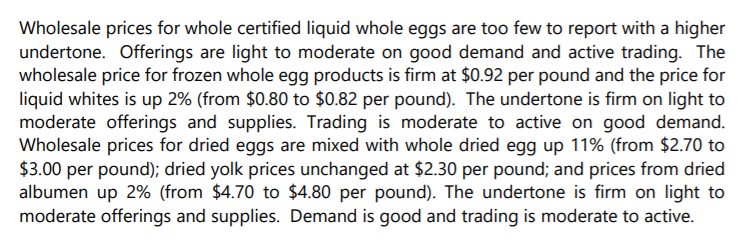

whole dried egg rose $0.25 to $4.50 per pound,

dried yolk gained $0.20 to $4.00 per pound,

dried albumen were up $0.10 to $5.25 per pound.

1 Like

M/s SKM Egg Products Export (India) Limited (Scheme for Creation/ Expansion of Food Processing/ Preservation Capacities – Unit scheme)

The unit has been established in an area of 137835.93 sqm (34.06 acres) in Erode Tamil Nadu for modernization/expansion of the existing facilities for manufacturing of egg products with a total project cost of Rs. 19.99 crore including grants-in-aid of Rs. 5.00 core and private investment of Rs. 14.99 crore. The processing capacity created by this unit is approximately 7500 MT per Annum. This unit will generate employment generation 250 direct &740 indirect and will benefit 20 farmers

Limited, (Erode,TN)")

4 Likes

19 crores PAT in H1. There has been good demand during world cup for eggs and also USA and europe are seeing life high cost for eggs.

Surely on the way to beat 26 crores PAT done in 2016. Stock has median PE of 16 for last 10 years and 11 p.e for last 16 years.

.

3 Likes

.

Such a strong set of numbers. I hope in time corp governance issue also gets resolved here.

.

Market looks good.

Thanks to all boarders for contributing to this thread. Only VP can have so much information about a sub 500Cr MCap nano-cap company that doesn’t do concalls ![]()

A few open questions for me based on my reading of the thread.

-

Are there any updates about the IT raid in Nov '21 where news reports claimed unaccounted income of 300Cr was detected by the IT Dept? I could find nothing online, but maybe somebody from this forum was able to get in touch with the company for an update?

-

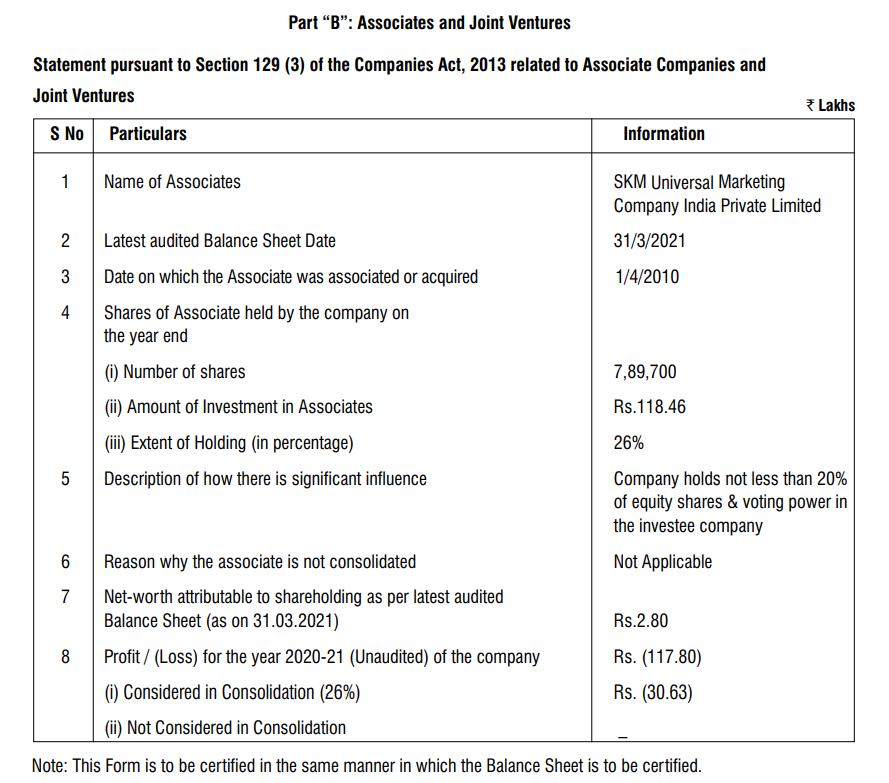

It does seem like SKM Universal (The associate company where the listed entity now owns 26% equity) is the company responsible for sales of the FMCG egg products. The products aren’t even listed on the listed entity’s website, but are listed on SKM Best eggs website (https://skmbesteggs.com/). The contact us section on the website lists the SKM Universal address, so safe to assume the unlisted entity sells the products.

Does anybody have any information on how well these products are doing in the domestic market? The domestic sale of egg powder and egg liquid has increased from 10Cr in FY20 to 17Cr in FY21 to 42Cr in FY22. Could this be due to value added FMCG products? (I don’t see a separate head for revenues for FMCG products, so assuming it would be reported under this bucket?)

Domestic sales increasing for the company would be good news because domestic demand would most likely be less cyclical than export demand and at more consistent realizations.

- In order to determine whether the Management has this arrangement (Mfg of FMCG products in listed entity and sales via unlisted entity) due to the listed entity being an EOU or in order to park profits in the unlisted entity, we have to access the financials of the unlisted entity. AR FY22 does mention AKM Universal’s net profit although it fails to mention its topline (These figures are for FY21). The entity made a loss of 1.2Cr in FY21. So prima facie does not look like a case of parking profits.

Company 360 has this to say about SKM Universal

Does anybody have the financials for SKM Universal? If not, I will purchase them from Company 260 and share them here (Don’t want to duplicate if somebody already has this)

- The unit has been established in an area of 137835.93 sqm (34.06 acres) in Erode Tamil Nadu for modernization/expansion of the existing facilities for manufacturing of egg products with a total project cost of Rs. 19.99 crore including grants-in-aid of Rs. 5.00 core and private investment of Rs. 14.99 crore. The processing capacity created by this unit is approximately 7500 MT per Annum. This unit will generate employment generation 250 direct &740 indirect and will benefit 20 farmers

This was posted a couple of posts above mine. While this excerpt suggests company invested 15Cr and got 5Cr in grants, the FY22 cash flow statement suggests that investments towards PPE was only 9Cr? What would explain the difference? Also, as a result of this investment what is the % increase in production capacity for the company?

4 Likes

Dec Qtr numbers have been great with all time high quarterly sales of 182 crs, but what stood out even more was that the operating margins have more than doubled to 25%. The last couple of years have seen these margins more in the vicinity of 10-12%. We need to ascertain what has brought about the increase in sales from the earlier quarterly run rate of 70-80 crs to the current 160-180 crs., & more importantly if this is sustainable. We also need to understand what kind of margins are sustainable.

The mgt had indicated in the last AR that the current year 22-23 would be a good one, so some credit is due to them as well. It has also been updating the exchanges about large & new meaningful orders that the Co. has been receiving from Russia, UAE etc., so maybe the increasing sales is not such a big surprise. There is a general perception about mgt. quality, but it would help if there are any specific instances of the mgt. short changing the minority shareholders. As mentioned by @nirvana_laha in the above post, the other marketing co. where the promoters hold a much higher stake is not making too much money. Well, times sure are changing & in these times of comparing market cap to determine who is bigger n better, it pays to be honest!

7 Likes