On the face of it, Q4 results look disappointing. However, when we get into the depth of each figure, it looks like the company is making a deliberate attempt to make its number look disappointing by re-grouping & stating numbers without providing any explanation in the notes. More credibility is for Standalone numbers as the Consolidated numbers basically include numbers for subsidiaries in Japan, Europe & Russia. They have margins to manage their expenses and some surplus. The numbers of that will make more sense in Annual Report. Purchase of Stock-in Trade is a mystery. If we look at FY 16-17 Annual Report on page 65 and note 12 on page 72, the figure is just 3.91 Crores and it only mentions Customs clearance & logistics expenses. I fail to understand the logic in showing Customs Clearance & Forwarding Charges of Russia Branch as Purchase of Stock in trade. However, if we look at this Q4 results, the Purchase of Stock in trade for last Financial year (FY 16-17) is shown as 15.51 Crores. The notes fail to mention anything about how are the numbers regrouped to change the Annual Report figure from 3.91 crores to 15.51 crores. The figure for current year is 62 Crores. Is it that the company is getting the B2C goods manufactured from private entities for sale in Indian Market? There is no break-up for Other Income. So we do not know how much of MEIS & State Subsidies have been accounted for and how much is held back for bringing on book in the next year. Even after this, the company has reported highest ever Annual revenue of 299 Crores. The earliest best was 287 crores in 2014-15. Working Capital Cycle has improved drastically. Inventory has come down from 80 Days last year to 50 days. Receivables remain steady as 21 days and payables has come down from 22 days to 20 days. So Net working capital cycle has come down from 86 Days last year to 51 Days now. A reduction of 35 days. This is reflected in low Interest outgo for the quarter. Tax payment as percentage of PBT stands at 77%, if we include differed tax. If we look at only current year tax, it stands at 42%. Contingent Liability has come down from 4.51 Crores to 3.30 Crores. This is the lowest since FY 2012-13. So the company is cleaning up its Balance Sheet. All in all, we could reiterate, the company is making a deliberate attempt to make numbers appear weaker than they actually are.

May be the management wants proxies to accumulate at lower levels? How do we get the management to answer the profit sharing ratio for the value added products in domestic market?

Egg white qube dishes in top hotels@chennai

Egg white qube dishes in top hotels@chennai

Some quick thoughts from the FY18 annual report:

- MD&CEO hiking compensation to Rs 13.5 L/ month - seems excessive in a down cycle

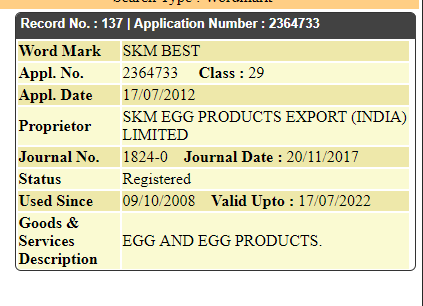

- I couldn’t find a mention of the B2C business or the brand “Best” at all in the AR.

- Interesting to see Madhu Kela’s Singularity Ventures has picked a 0.5% stake in the Company

- The big jumps in sales (stand alone) have come from India (~3x from 30 cr to 88 cr), Russia (~1.5x from 32 to 44 cr) & Europe (~3x from 7 cr to 21 cr). Japan was flat - MD&A says reentering Korean market now as well as in Africa

- Related party transactions continue to be difficult to understand (for me at least)

- Subsidies (classified as other income) upto Rs 9.4 cr from 9 cr. Not sure who the subsidy is from and for what.

Good snapshot on the company. B2C is where the company will be focusing. Company is betting on Egg White Cubes to be a game changer. Doing business in Japan, Russia and Europe is tough, competitive and unpredictable.

When you mean company is it skm egg or best egg ?

Why egg white is not listed as a product on the skmegg company page ?

I mean the company SKM Egg

Egg White is a recently added product, it could be listed on the SKM Egg website in the coming days.

Patience is key if you are invested in SKM. For decent gains one must be willing to wait 2-3 years for the next leg of the company’s growth.

Disclosure: Invested. Offloaded half the investment at 100+ levels and holding on the rest.

SKM Universal Marketing owns the Best brand and distribution is the understanding in this thread. This entity is related-party, promoter owned company and stands to benefit from the FMCG foray and not SKM Egg products, the listed entity which appears to be more of a contract manufacturer for SKM Universal Marketing.

SKM Egg products own less than 20% of SKM Universal Marketing. I would love to get hold of SKM Universal Marketing business as it definitely would command some sweet margin!

Also, is this why Venky’s ROCE (from screener.in) is more than that of SKM?

After hitting three lower circuits since posting a presentation on company from AGM, company submitted a revised presentation to exchanges with amended correct figures for both export and domestic sales.

Circuit limit revised to 5% from 10% effective 3rd October.

Export sales is around 61.5Cr from the link above dated May 4 adding new destination like Afghanistan. With the increasing contributions from domestic front, it should be a good Q2.

Article says broiler chicken prices are on the rise due to killing of birds but egg prices are softening in March, compared to February prices. Not great news for SKM.

Low egg prices are a good thing for SKM. Eggs are the RM for SKM. Broiler prices and SKM’s product prices are not essentially co-related.

How is B2C Products response ??? I heard there is delay in launch of pro-drink mix.

Mgmt earlier told listed entity will manufacture and skm universal marketing company is distribute. In last Investor Presentation company has done investment in B2C and AD Expenses.

they started a feed mill under private company… they are moving all profitable business models to private concern and cyclical ones to investor. very disheartening to see this kind of approach from skm group whose chairman is Padmashree Awarde

as members said, no mention of this brand their annual report. Brand is owned by listed entity.

From the annual report, domestic sale still remains at less than 2% of the total revenue so the B2C product range doesn`t seem to be doing that great

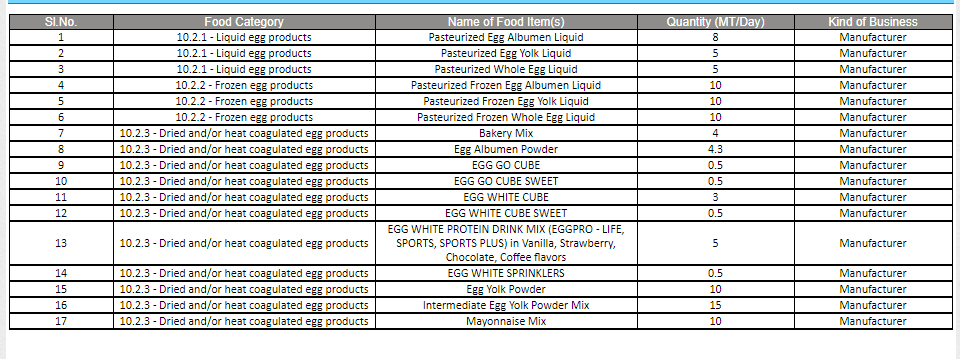

New Product Developments: Frozen Egg Liquid - Products with extended Shelf life of 9-12 months stored at -18 C Frozen Egg Albumen are being exported to Thailand. Developing Frozen whole egg and egg yolk with additives for different markets In process of developing flavored Egg Liquids for domestics market Developed salted egg yolk with an enzyme for mayonnaise industry. The product can withstand higher temperatures

Exports around 60% of Egg Yolk variants to Russia New products of Chilled Egg Liquid & frozen egg liquid are highly acceptable in Europe, Middle East & South East Asian Countries. Continuing Egg Liquid Exports to UAE and the Middle East. Two main customers in Oman have accepted the product and have started buying 3 containers per month. A new customer in Thailand has approved Frozen Egg Albumen and have placed orders to buy 2 containers per week till December 2019. Re-entered Saudi Arabia market and started exporting from July 2019 Re-entered Korea market and expect to build up good volumes later this year

SKM Universal incurred a loss of 3.84 Cr in FY 18-19. SKM Eggs holds 26% in SKM Universal and hence approx. 1 Cr. of this loss reflects under OCI head in consolidated Accounts

Company spent nearly 2 Cr. on Advertising & promotion in last FY as against 30 lacs in year prior to that. Not sure, how much of this is for B2C products

Company sold 6420 Tons of material in FY 18-19 for an export revenue of 228 cr. This shows an average realization of about 3.65 lacs per Ton which is the best after FY 15-16 where the average realization was 3.86 Lacs. In that year the company had made profit of 23 Crores. Looks like Maize price increase ate into the profitability big time in FY 17-18. The numbers could have been lot better otherwise. With good monsoon and reducing maize prices, we can expect good Q3 numbers for current financial year…

Company has Term loan of 4.43 Cr. @ 9.20% p.a. and working capital loan of 39 Cr, which is in foreign exchange bearing interest rate of 3.5% p.a. The company also maintains Bank Balances and deposits of 23 cr on which it earned interest income of 2.28 Cr. It paid Interest of 4.24 Cr on Term Loan and working capital loan. so the net borrowing is 20.43 Cr and net interest cost is approx. 9.6%

On a positive note, we can say that per ton realization from their exports are at the highest level since 2015-16, so we can witness one more cyclical uptrend for them in this year and in next year. We should not be buying more at that time thinking it as a turnaround story in anticipation of higher returns though. This is a cyclical business just like any other commodity business. If we buy at peak of the cycle, chances of us making money are very low

I recently attended their AGM

I talked with officials over there, MD didnt attend the AGM as he went for Exporters meet.

- Best Brand is not owned by Company it is owned by MD Skm Shree Shiv Kumar.

- There are planning to covert this food company but not in near future that’s their long term plan.

- They have gone for the soft launch for Skm Egg pro powder

( Kishore has been appointed as dealer for this in chennai, he is ( 6 times Mr. Tamilnadu and 2 time Mr.South India) Kishore mobile number 996294930 for more details. - They are exploring some more products in food segment but not anything in immediate future

- They have JV with Happy Hens (small venture) for supplying cage free eggs organic hens.

- Company is very conservative and don’t want to take risk in B2C joint venture.

- There are improving on their cost structure and breaking capacity and there by increasing efficiency.

Over all B2C is totally ruled out for next 2 to 3 Years. May be this year 5 crores of sales is expected. Their Traditional Business is stable and should improve in next year.

Since there is no major debt any upswing in bottom line is good for the company. I would be happy if B2C division is run by someone who is younger and can understand today’s life style changes.