Skipper expands its exports market by bagging Rs 100 Cr of orders from several new geographies

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=47a83830-1785-436a-8264-89b162408880

Skipper expands its exports market by bagging Rs 100 Cr of orders from several new geographies

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=47a83830-1785-436a-8264-89b162408880

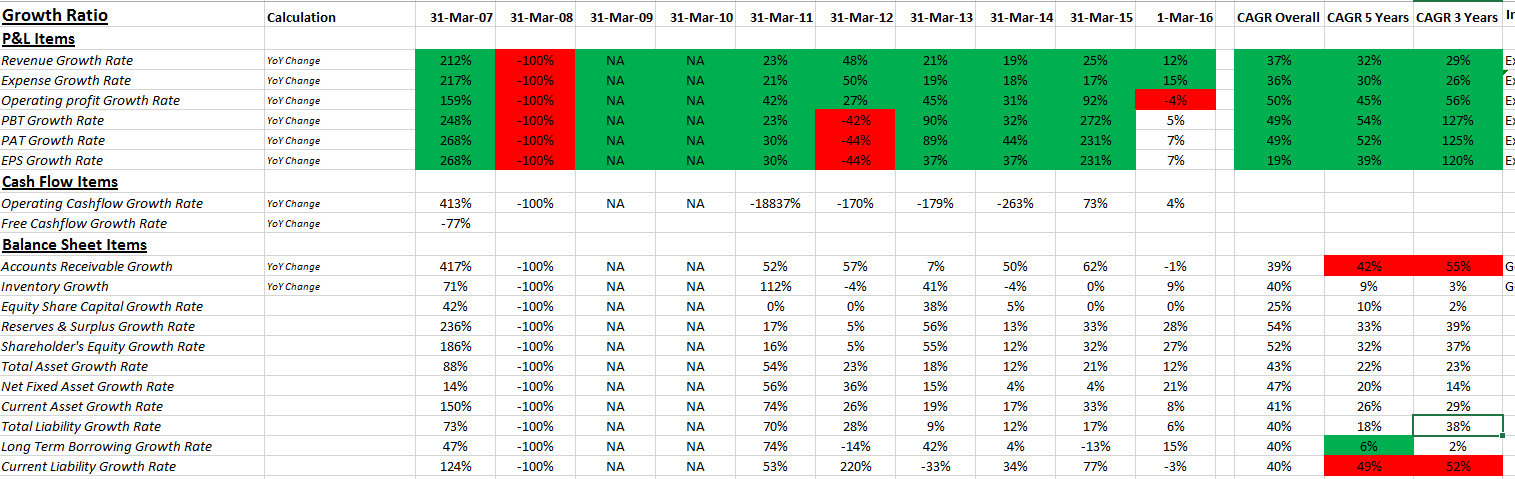

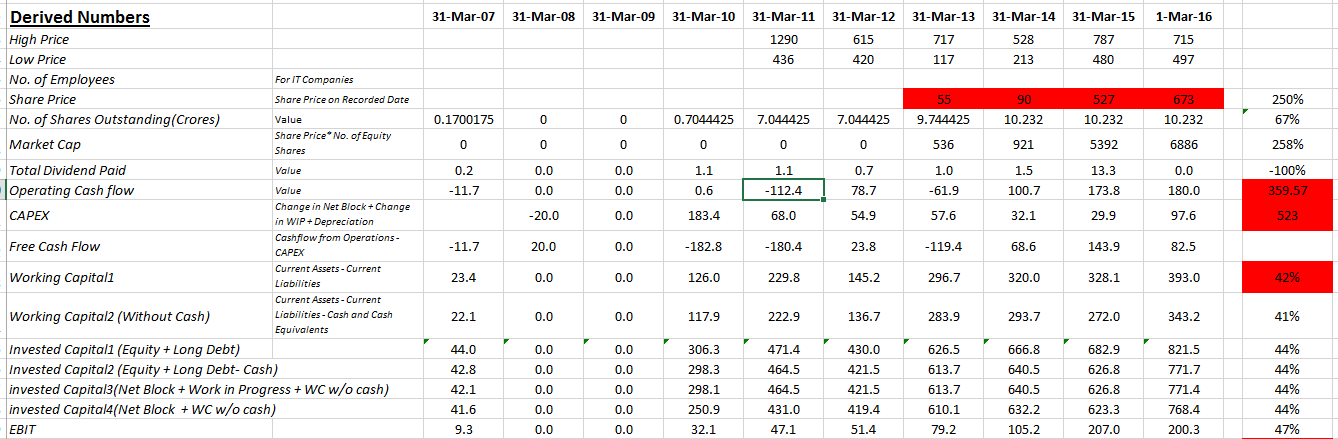

I am invested with approx. 3 % of my portfolio. Do not see any risk from revenue growth perspective but I have few concerns of financial quality of business. Few points I would like to highlight about financial quality of the business (data collected from screener.in and 2009 & 2010 data was missing, hence, those years ignored as of now)

Disc : Invested with 3% of portfolio and evaluating further as a portfolio concentration exercise

My quick notes from the con call - Possibly missed some points.

Highlights:

Highlights of the PVC Business:

T&D Business:

On the PVC Business - Management seem to be very focussed on expanding capacity to 100,000 T by FY 18. However, with capacity utilization levels quite low just now – and no immediate signs of an up-tick I am a little circumspect with respect to their want to keep the pedal pushed firmly to the floor.

Additionally, what is evident is that in the PVC business their margins lag the big boys (Astral/ Ashirwad etc.) quite substantially. They are attempting to use price as a ploy to wrest market share from them and in the long term am not sure if that’s a great strategy. With Sekisui partnering with Astral earlier this month Skipper is going to have its work cut out … Regionally, particularly in the NE the brand will do well – however, their entry into the Southern market may take time to show rewards.

Promoter has sold 2% of stake to L&T.

But, stock has increased about ~12%. I think promoter selling in bulk is not a good thing.

Any views?

Looking at the capital management of the company we find that in last 7 years (from FY11 to FY17) the company has earned cash flow from operation (CFO) of Rs 521.7 crore. Capex done by the company in that period is Rs 421 crore, giving us the free cash flow of around Rs 100 crore. Out of this Rs 100 crore company has paid total dividend of Rs 86 crore leaving us with cash flow of only Rs 14 crore. Between FY11 and FY17 company has paid total interest of around Rs 340 crore and total bank commission of around Rs 46.4 crore. To pay for this cash outflow company has taken debt of Rs 87.4 crore between FY11 and FY17. Now since there is no fresh equity is infused by the promoters, it raises the questions from where the company is paying for the cash outflow of around Rs 140 crore. In the balance sheet company have cash and cash equivalent of ~Rs 25 crore out of which ~Rs 23.5 crore is pledged to the bank for bank credit facility, and cannot be used freely by the company. It is advisable that the investors should clear this before investing in the company. Report-skipper.pdf (298.2 KB)

Very elaborate. Just to learn, from where did you get the data for Metric analysis?

All the data I have compiled from Balance sheets of previous years. Rest is from various resources like company concall and investor Presentation. If you want I can share with you the excel sheet for reference.

@mykb Please share!

Thanks

Grwth 3 skipper.xlsx (76.9 KB)

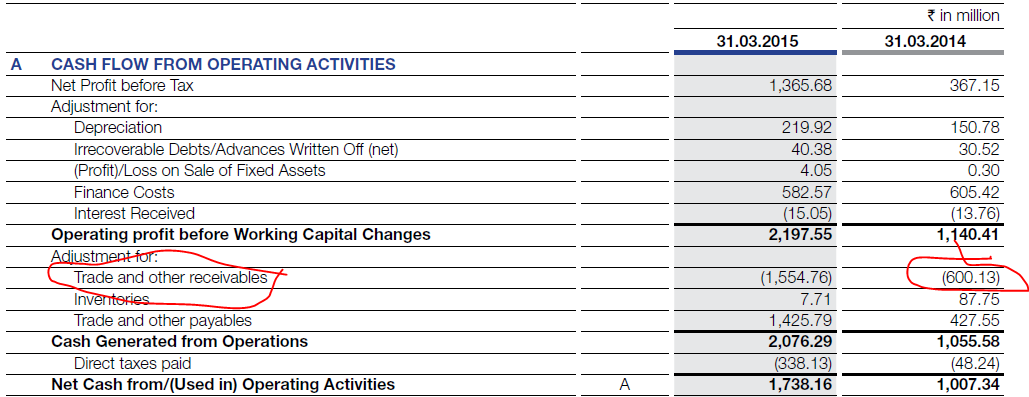

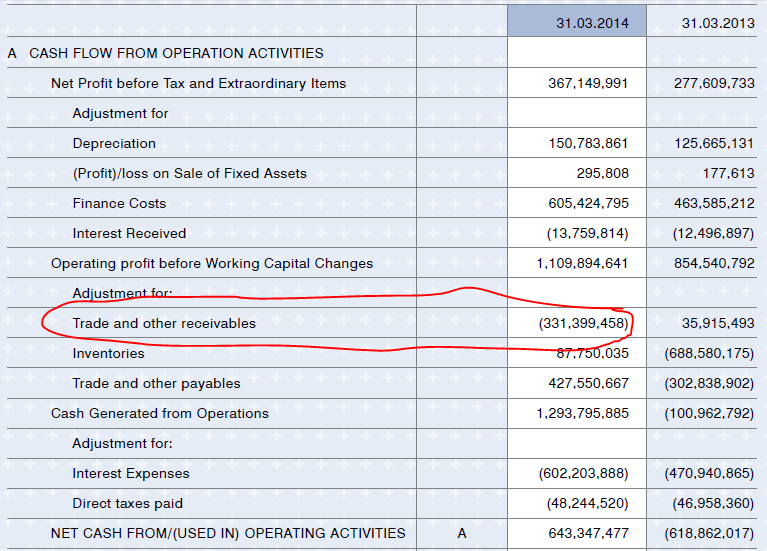

Dr. Malik has raised pertinent questions regarding Skipper on his blog - need to investigate these going forward. I did the numbers myself and there is some discrepancy for sure.

Disc: Invested 5% of portfolio and might reduce stake in light of these concerns

The cash flow reconciliations with regard to trade receivables, trade payable etc. have been covered in finer details in the Q&A section of the blog…

Sanjoy Bhattacharya is betting on Skipper Ltd. I believe this company will be a huge beneficiary of power sector policies.

Trying to understand what could be the reason for such a steep fall of Skipper? At current price its available at a PE of 16 (with TTM EPS can come down further if Q4 EPS is considered).

The company is showing early signs of deteriorating balance sheet quality. The working capital days is showing a really bad trend with Inventory levels at abnormal levels. While the order book is encouraging - i guess the management needs to really work on getting some of its basics right.

Disclaimer: Had a small position from February 2017 and exited after current quarter results. Will look for a reentry if this falls to more attractive valuations.

Investor presentation from the company:

They believe working capital cycle of 83 days is manageable. No word on the inventory.

Does anyone have a summary or the key points discussed in the earnings con-call for Q1 FY 2019?

Wow. These guys sure have put a lot of money and effort making investor presentation. If only they put such effort in marketing their PVC products, maybe it would have not seen such bad days ( Siddhu as a brand ambassador? come on!! )

Insider has bought 250,000 share on 14th August.

SKIPPER SHARAN BANSAL 250,000 BUY

Another Insider bought today …

SKIPPER SHARAN BANSAL 250,000 BUY