Skipper Limited:

Market Cap: 1519.40 Crores

Current Price: 149.5

Book Value: 29.70

Stock P/E: 16.41

Dividend Yield: 0.88%

Face Value 1.00

Return on capital employed: 30.11%

Debt to equity: 1.13

Interest Coverage: 15.09

Skipper is the market leader in power and water sectors, is among the fastest growing companies in the power Transmission & Distribution area, which offers huge potential that the management is confident of exploiting. Its all-encompassing presence in the value chain from angles to tower production and fasteners to EPC enhances cost efficiency, which coupled with market leadership will lead to better returns. The company plans to scale up each of its businesses with an asset-light model, and focus on increasing tower exports. It also plans to gain a strong foothold in monopoles, EPC and PVC pipes.

Skipper has strong presence in North East India in Power T&D and have 5 plants across India ( 2 in Howrah, 1 in Assam, 1 in Telangana, 1 in Bulandhshr).

Recently company has ventured in Water Distribution (PVC) as well. Currently, 80% sales is from Power T&D and PVC has 7% share in share. Company is expecting to increase PVC share in sales to 20% on expanding the PVC pipes business.

MY VIEWS:

a) Given thrust of government to increase power and electricity across India, Power distributors like Skipper will be benefitted and Hence, increase in sales.

b) Third largest capacity of TLT towers: Skipper by April’2015 will have total capacity of 1, 75,000 TPA (up from 1, 51,000 TPA) of tower manufacturing capacity. It is the third largest capacity post KEC & Kalpataru in the domestic space. It has three manufacturing plants in the state of West Bengal and assam. Given the huge capex plans in TLT infrastructure in the country, the demand for towers are expected to grow at rapid pace and Skipper is well placed to capture the opportunity. All the three manufacturing plants are approved by PGCIL. Also it will have added cost advantage due to same.

c) The Government’s thrust on water, irrigation, river management, improving sanitation, sewerage and urbanization the PVC pipes and fittings markets is expected to grow at much higher pace then its historical 8-10% CAGR rate and reach ~391 bn in FY19. Skipper’s PVC business will also increase with recent investment in Ahmedabad for same.

PS. I am tracking the stock and do not hold any share.

Thanks for sharing this new story. I have been tracking this Company from past one week. Don’t know much about the Company but read its latest annual report.

Some of the important extracts from the Annual Report are the following:

The Company has become the manufacturing partner of Sekisui a Japanese Company which is one of the world’s leading manufacturers of CPVC compound, for manufacturing premium quality CPVC pipes.

Secondly the Company has entered into tie up with WAVIN, a Netherland based Company, which is one of the world’s most renowned plumbing technology companies, for launching in India, the most advanced plumbing systems in the world. With these the Company is hopeful of becoming a Pan India brand in the PVC piping space in the near future.

The Annual Report seems to be of Standard Quality and carries the following vision statement:

“To be a billion dollar company by 2020 that is focused on producing industrialised, market oriented and finished products and services, with an increasing affinity to customer-centricity.”

Important Points Noticed:

1600+ Employees as on date and growing;

Largest player in eastern India with unrivalled leadership for all T&D projects announced by the Government of India for east and northeast India.

30 years+ Domain knowledge across towers and pipes industry.

OUR MANUFACTURING FACILITIES We have three state-of-the-art manufacturing facilities - two at NH-6, Jalan Complex, Jangalpur, Howrah and a major one at NH-6, Uluberia, Howrah.

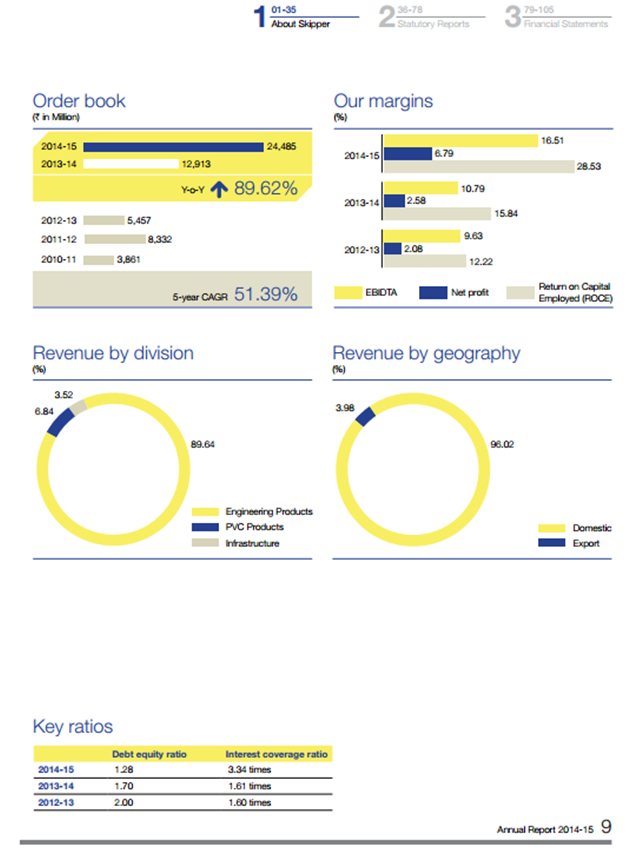

51.39% 5-year CAGR

Trading and Deliverable Data indicates that day in and day out the deliverable of total shares are > 75% coupled with rise of share price is really noticeable for such small cap Company (Please verify with the link and search- Stock Prices)

Positives (Views)

Numbers and Margins are improving year after year;

Huge deficit in India for Power and opportunity to tap with New Government (The per capita consumption of power in India is around 90 kVA per person, compared to the global per capita consumption of 313 kVA per person and China’s 447 kVA per person);

Negatives (Views)

Power Sector is highly regulated in India and it is not very often that we see multibagger in this sector;

High Debt sitting in Balance Sheet.

Questions:

In the Annual Report “asset-light approach” is mentioned . Unable to get to know about the dynamics and model.

Does anybody have any idea about the promoters? Basically want to know about integrity and shareholder friendliness of the promoters?

Lets discuss this Company in detail, this might be a great story in the making which will truly unfold as time progresses.

This stock came under my radar a few days ago and started reading about it. I was about to start a thread on the same so thank you @hssodhi198 for taking this initiative.

Now coming to the company, I have a few points to add:

In the power transmission sector, the line of work is as follows:

a) PGCIL or one of the state discoms come up with a tender for a line which is generally an EPC project. The tender is on L1 basis after come technical requirements are fulfilled. This company is new to the EPC part of the business although they have been the suppliers for a long time. So for them to expand in this space they need to get sufficient experience to participate in tenders. Some companies generally take the JV route if they are not qualified, so we need to know how is the management planning to do this.

b) The EPC business is a very slow process with many extensions and delays in payments from the discoms. This is effect the working capital of the company if they plan to expand further in this space.

General procedure for finalizing a tower for full fledged manufacturing consists of a on ground test where in the actual tower is made and forces are applied on the tower to know if it can withstand the loads. I donot what capacities are present with this company. This is also the area where companies like KEC have an advantage i.e. they have manufacturing, testing as well as EPC business and they have been running for a very long time. So if we are bullish on electrification of India why not invest in market leaders, where the scope of additional capex is also limited.

The segment of PVC pipes for water and angle sections for power transmission are totally unrelated. What is the rationale for selecting this combination of businesses?

To whom does the company currently sell their power transmission sections to? I have had a rough go through the annual report but couldnt find any names. If information is present on this please share.

Cheers!!

Disc: I do not hold any stocks of this company. Currently tracking it closely.

Following are some key points from the latest concall July 30, 2015 (for better understanding of Skipper as Business):

Going forward we also are in the process of setting up three more units of PVC pipes. The first one will be in Sikandrabad near Delhi, second one will be in Guwahati in North East and the third one will be in

Hyderabad, Telengana. (In my view, clearly indicates Nation-wide rolling of plans)

CPVC is a product that was missing from Skippers range for a long time primarily because we were

not finding the right partner for supplying us the raw materials for this product. As you might know,

CPVC is a product which is produced, the raw material is basically produced by only four global

manufacturers, one in America which is Lubrizol one in France which is Arkema and two in Japan

which are Sekisui and Kanika, so recently Skipper tied up with Sekisui for support of this raw

material and now Sekisui has started supplying the raw material to us and we are manufacturing the

pipes in India, which is the same model followed by Astral and Aashirvad with Lubrizol of US.

Interestingly Sekisui is the only other company apart form Lubrizol which is NSS certified so this is a

certification which is received by the company, this is a US certification and that carries a lot of

weight in the water segment. Because Lubrizol and Sekisui are the only two manufacturers of NSS

certified raw material our product also automatically becomes that much more respected in the

market. Now going forward with the addition of CPVC we will be looking to penetrate the plumbing

market in India in a big way. This is going to complete our basket of sorts which apart from CPVC

will also have UPVC and SWR pipes so now we will be able to bid for complete projects basically

which we were not able to earlier. On top of this the Wavin tie up that we have entered for

polybutylene pipes which we have also recently done that is the most advanced plumbing system

which is available in India right now, in fact in the world right now and Wavin has chosen us as its

partners in India and initially they are going to be supplying us this complete system from the UK

plant but the idea is that going forward will be manufacturing that in India itself under Wavin

licensing.

Polybutylene will probably not happen this year that will probably be part of the capex plan for next year.

Our order book is pretty much split 50-50 right now, 50% for exports and 50% for domestic and

where domestic ordering is concerned as of now almost we can say 90% of our domestic order are

from PGCIL. (In my view, there is too much dependency on one buyer- Power Grid Corporation)

We are qualified for the highest range possible in power grid. In fact in Power Grid Skipper is the

single largest tower supplier right now.

Our capacity utilization is 90% plus.

We require marginal capex because every year we increase capacity by about 20% in our T and D

division and so that’s doesn’t require much capex because most of the fixed infrastructure is already

available with us. Approximately between 20 to 25 Crores.

Because typically the order inflows generally happen in Q3 and Q4, Q1 and Q2 in fact we are just

happy to maintain the order book level even then the company has secured approximately 150 Crores

of new order from export market even in Q1 which is generally not seen in regular Q1 and Q2.

Yes, we have already started delivering on export order which is in fact, this year we should see

significant, export being a significant part of the top line, last year was only below 15% but this year

we expect at least 30% to 35% top line coming from export business, definitely share of export

revenue is going up and in terms of the order, you asked about the cycle of the order I mean how long

the order is….

The delivery period typically for export order is between two to two-and-a-half some of our orders are

already in the second year one which we have recently secured they will be delivered over the next

three years.

PVC as I mentioned earlier we have already commissioned a new plant in Ahmedabad with a capacity

of 10,000 tonnes which will augment the existing capacity of 12000 in Kolkata and we expect that

with further three new plants which we are adding in this financial year our capacity will be close to

about 40,000 tonnes by the end of this financial year; this is in line with our target to reach One Lakh

Tonnes by FY’18.

Typically what happens in the infrastructure project, all infrastructure projects including transmission

project they see a reduced activities during the monsoon month so from April onwards basically

project contractor starts reducing their inventory at site which is why the offtake becomes very low in

Q1 and Q2 but towards the end of Q2 really the requirement, the push starts coming from the project

site for the material, so typically that is what happens every year but even if you compare the quarter

numbers to quarter of last year there is a significant improvement.

You also need to account for the fact that PVC as a product has a lower working capital cycle also as

compared to our T & D products, so while this might happen to some extent wherein our engineering

product business commands an EBITDA of more than 15% and this might look at somewhere around

13% -14% but because of lower interest impact, we will definitely see the pact being maintained and

bettered going forward.

In a consolidated basis the company is growing at, the plans to grow at more than 20% to 25% every

year and while there is absolutely no dearth of orders in the T&D business the PVC business with its

rapid expansion on a pan-India level we do not see really any major obstacles in getting the numbers

that we are looking at.

Yes, in fact the company is very conscious about increasing debt so for our expansion plans over the

next two to three years we do not envisage adding to the long term debt of the company at all. So

really whatever debt we have will be in line with the existing debt repayment schedule, so we are not

looking to add any kind of debt for future expansion.

Yes, as I mentioned approximately 50%, 1200 Crores is from export business and another 1200

Crores odd is from domestic business, out of which you can assume 1000 Crore plus from PGCIL.

We also export certain portion to Europe as well as Africa and also Nepal so those countries also form

part of our export order book. Of course the lion’s share goes to South America and approximately

you can assume it to be an even split between the three countries as of now, so I would say between

30% and 35% for all three countries.

So the monopole capacity which is expected to be commissioned in Q2 of this year, the initial starting

capacity will be somewhere around 15000 tonnes for being a engineer fabricated product the capacity

can vary slightly but then tentatively around 15000 tonnes will be added to our overall capacity of

175000 tonnes of T&D capacity and we are at discussions with many of these utilities and they have

shown keen interest in this, so we expect good response for it once the unit comes up. The products are already across being used in various utilities in the transmission side as well as in the telecom

side. That market is already there.

PGCIL follows a policy that whatever projects they win on in the TBCB route those projects they

split the contract between supply and construction, so if you look at a Lakh Crores in total the total

basket approximately 40,000 Crores is expected to come upon TBCB route. Now in that going by the

past trend PGCIL has been securing 50% of all contracts that have been there in the TBCB and also

some of the private developers like Sterlite and Essel even they sometime adopt the policy of towers

purchases separately and construction separate. If I assume 75% of the TBCB route business to be

split up with tower separate and construction separate then perhaps 40,000 Crores 75% we can look at

30,000 Crore of transmission business to be coming up on this split model basis.

No in fact we have witnessed that due to flat demand for the last couple of years we have seen

actually lot of non serious players going out of business, so competition scenario as of now I would

say less competitive than what it was may be perhaps two year ago.

So the new units which are coming up in Sikandrabad which is UP that would have a capacity of

roughly around 8000 tones per annum to start off with in phase one. The Guwahati unit we are

looking at a capacity of about 4000 tonnes per annum and the Hyderabad unit in Telengana that is

going to come up with a capacity of about 6000 to 8000 tonnes also. The idea is to reach capacity of

about 40,000 tonnes by the year end and as you can imagine in the PVC industry adding on capacity

is not very difficult because all you need to do is add extrusion line, so these are the first phase

capacities that we are looking at and then going forward we would start augmenting further capacities

in these units as and when required. In fact in all probability we will be able to commission all three of them or at least two out of them in Q2 and the other last one within Q3.

I hope above points will provide some understanding of Company’s business and give base to dig more about the Company.

Thank you @Value_Investing and @ramakanth for interesting posts. @ramakanth with below comments i am trying to answer your concerns :-

a) The sales from direct EPC projects for Skipper is just 46 Cr (>1% of total sales). (In-fact they have recently completed their first EPC project but do have few other in progress).Which only shows that Skipper is majorly supplier in T&D sector. Also there major sales is from manufacturing various engineering products (89%of total sales) which are used in T&D as well as others such as manufacturing telecom towers, LPG cylinders and Tubes. Although they are looking to expand in EPC projects in high power transmission towers (>400KV). the EPC tenders which they have to my knowledge is in high power transmission only.

b) Power Grid is the major buyer (~50% of total sales from engineering products). This is two way sword. Benefit is that they are suppliers. Companies winning Powergrid orders provides them orders for supplying various products which enhance chances of money recovery. Disadvantage is that its overly dependent on Powergrid. They are into same business from past 30 years and have good reputation which helps them getting tenders as material supplier so somewhat this disadvantage do not impact much. Also they are due to same reason have asset light model ie. do not require capex as much as companies taking EPC tenders.

c) Incomparison with KEC or Kalpatru whose major business is securing Tenders of EPC projects and delivering them. In a way both these companies model is different from Skipper.

With regards to why PVC pipes, I need to further look for the reason but on the onset, it seems to add another engineering product which is going to be in huge demand as indian economy progresses.

@Value_Investing, regarding “asset-light approach”:

" Skipper is the only company in India to have complete value chain control

from angles to tower production to fasteners to EPC resulting in control of over 80% of the

cost on any tower line. The company has done backward integration through angle rolling

which is the main raw material for towers and is also horizontally integrated with

manufacturing of fasteners and accessories for towers. The location of Skipper in Eastern

India allows it access to raw material at a competitive price leading to cost competitiveness

and it enjoys ~400-500 bps of cost saving by way of economies of scale, lower freight costs

and sources its raw material, mainly billets, from SAIL"

How Value Chain Control can result into Asset Light Approach? The understanding which I have of Asset Light Model is that Company’s take lease approach for its business for several years and don’t undergo any Capex. Ex. Indigo in Aviation, Byke in Hospitality etc.

Can you elaborate more on strategic approach of Skipper using Lease based model? What I have understood of Skipper is that majorly they are into Tower making business. What is the way in which they are using lease based model in this?

Board Meeting on October 05, 2015 | 26/09/15 19:11

Skipper Ltd has informed BSE that a meeting of the Board of Directors of the Company will be held on October 05, 2015 inter alia to consider acquisition of a PVC plant and approving Employee Stock Option Plan.

Further, the Company has informed that the trading window of the Company will be closed from September 28, 2015 to October 07, 2015 (both days inclusive).

Thanks for your post on Board Meeting. From the lens which I see the agenda items to be discussed in the upcoming BM are of significant importance:

To consider acquisition of a PVC plant (Inorganic growth reducing the learning curve in PVC business) and 2) Approving Employee Stock Option Plan (Big Sign of good management).

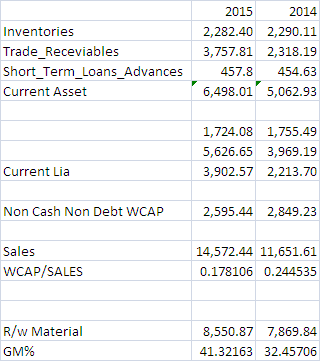

Excellent working capital management, Advance from customer increased from 26 crore 2014 to 76 crore in 2015 (this reminds of eicher from 2009/8 onwards advance from customers increasing), company getting 70% repeat customers and increase in gross margin indicates customers accepting price hike which speaks quality product and after sale services.

WCAP/Sales from 0.24 to 0.17 speaks of asset light in my view.

Can you please let me know from where you have drawn the following conclusions:

Advance from customer increased from 26 crore 2014 to 76 crore in 2015; and

Company getting 70% repeat customers and increase in gross margin indicates customers accepting price hike which speaks quality product and after sale service.