We are sharing this analysis as part of the ValuePickr.com community discussion. The intent is to exchange perspectives, identify blind spots, and test investment theses collaboratively. Fellow members’ inputs on risks, margin sustainability, and growth visibility will add immense value to the discussion.

SJS Enterprises is engaged in the business of manufacturing decorative aesthetic products primarily for the automotive and consumer appliance industry such as automotive dials, overlays, badges and logos.

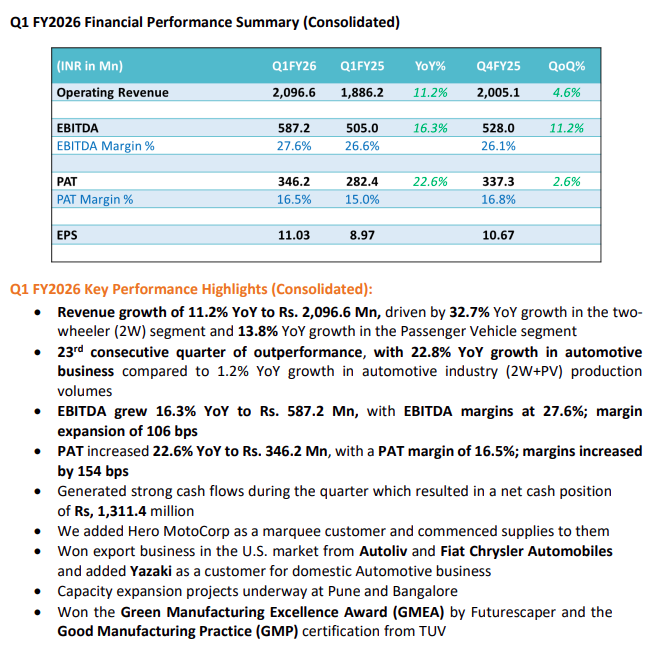

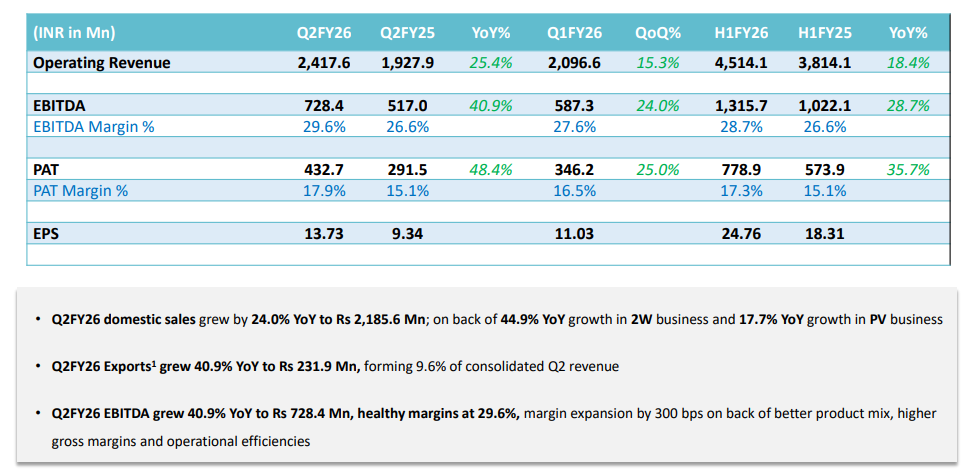

The Q1 FY26 results of SJS Enterprises illustrate how a mid-cap auto ancillary company applies financial discipline and strategic foresight to drive long-term value. 11.2% Y-o-Y revenue growth, coupled with 27.6% and 16.5% EBITDA margins and PAT margins, respectively, reflects pricing power and judicious cost management. Prudent leverage management is reflected in the net cash balance of INR 1,311.4 million. Both ROCE at 29.5% and ROE at 19.1% indicate good capital allocation, as would be the case with value creation sustained in the long term if returns are more than the cost of capital.

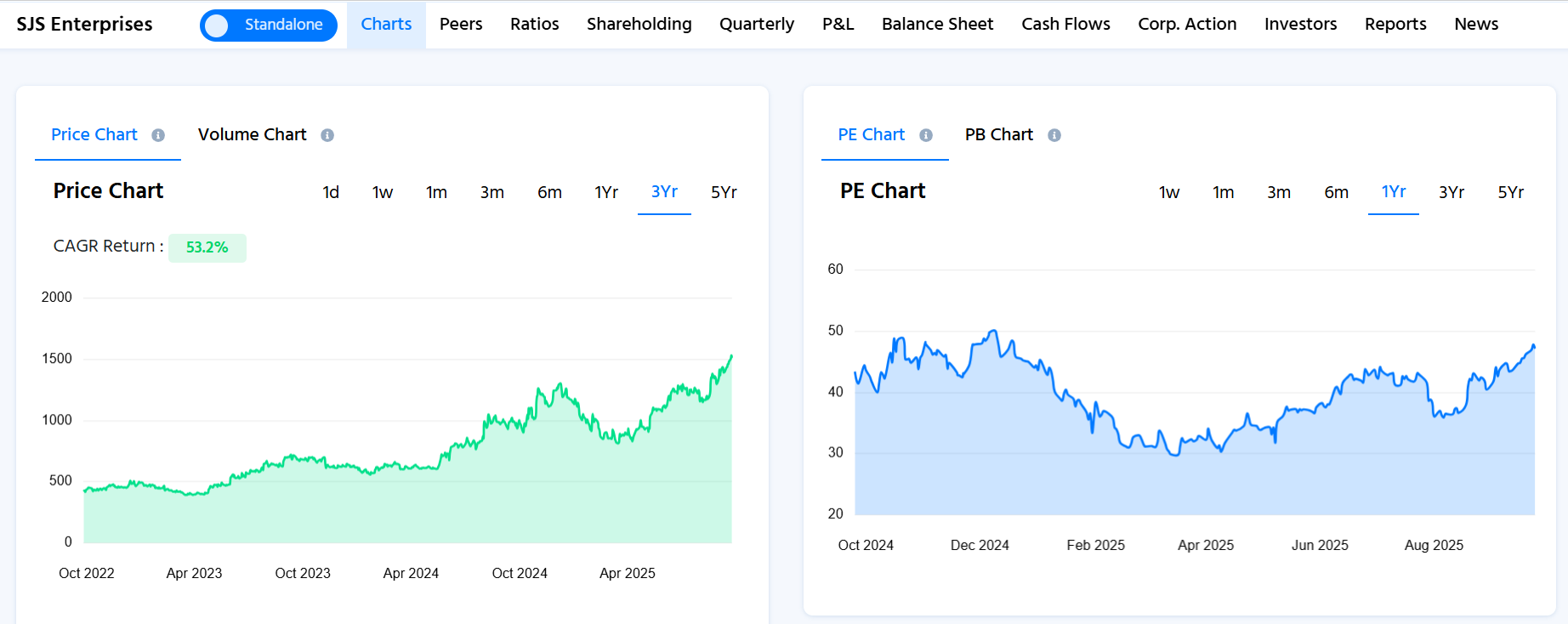

CAGR captures smoothed annual growth in a metric, excluding short-term volatility. At SJS Enterprises, the 1-year CAGR of 53.7% and 3-year CAGR of 52.9% represent high short- and medium-term growth rates, whereas the 5-year CAGR of 24.2% represents stable long-term performance. Overall, it indicates the contrast between short-term acceleration and long-term consistency, emphasising the need to measure both horizons when evaluating financial health.

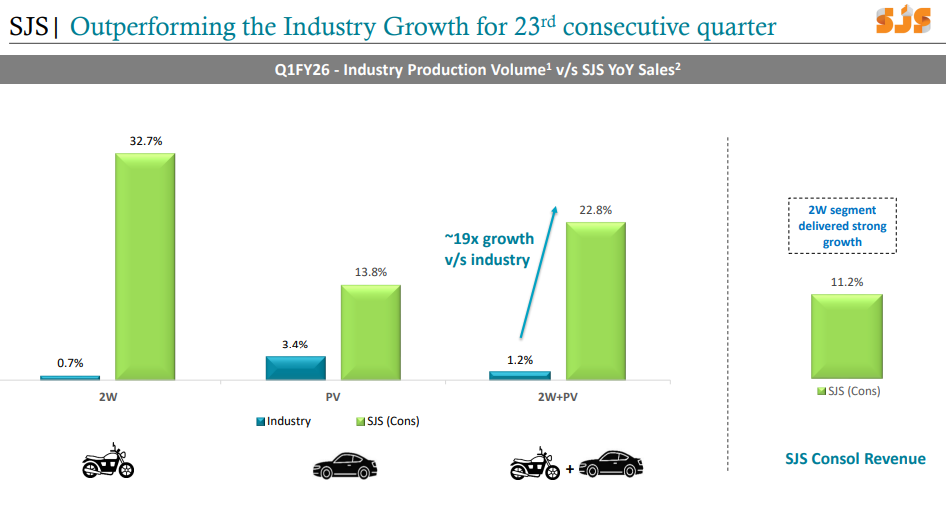

SJS Enterprises has outpaced the auto industry for 23 consecutive quarters. In Q1 FY26, whereas the 2-wheeler industry recorded just 0.7% growth, SJS reported 32.7%. In passenger vehicles, its growth was 13.8% compared to the industry’s 3.4%. On a combined 2W+PV basis, SJS recorded 22.8% growth compared to the industry’s 1.2%, nearly 19 times greater. This good performance enabled the company to achieve 11.2% consolidated revenue growth with the 2W segment being the major contributor.

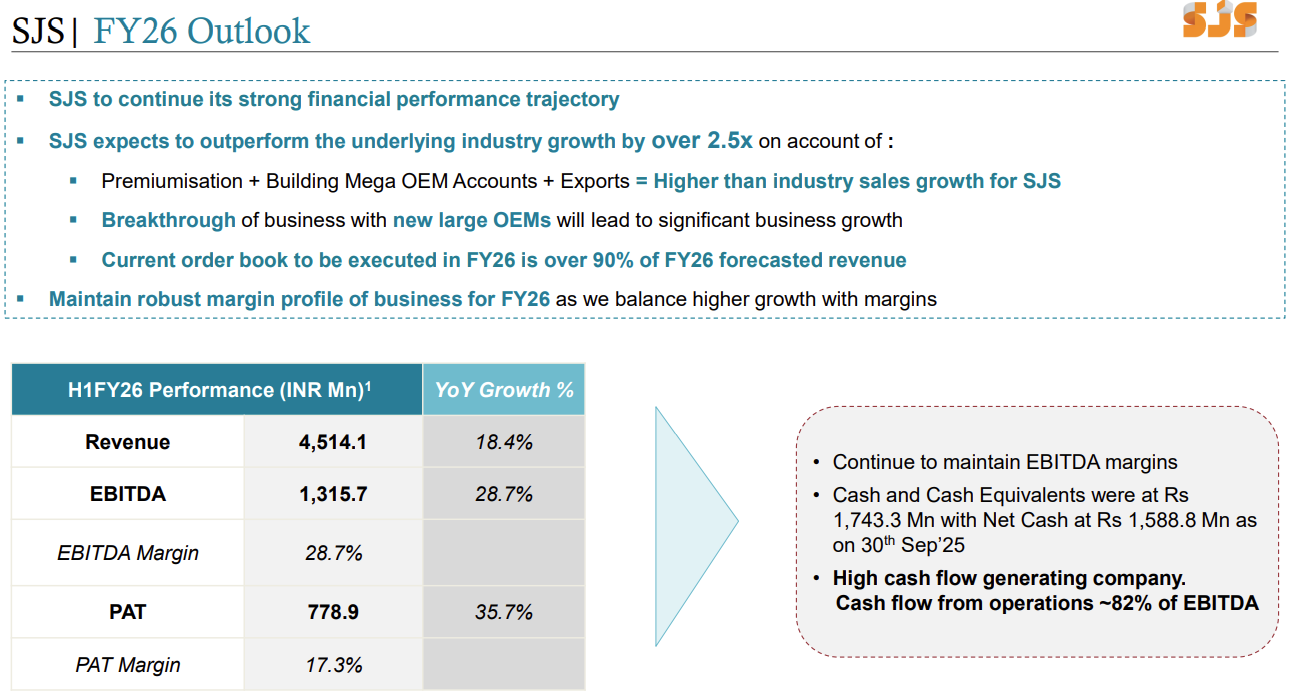

The firm’s 22.8% automotive revenue growth against industry growth of 1.2% is a proxy for competitive advantage by differentiation. Its premiumization efforts increase kit value per customer, and the acquisition of clients such as Hero MotoCorp bolsters the resilience of customer relationships as a strategic resource. Aspirations to lift export contribution to 14-15% of revenues by FY28 are international diversification aligned with market development strategies.

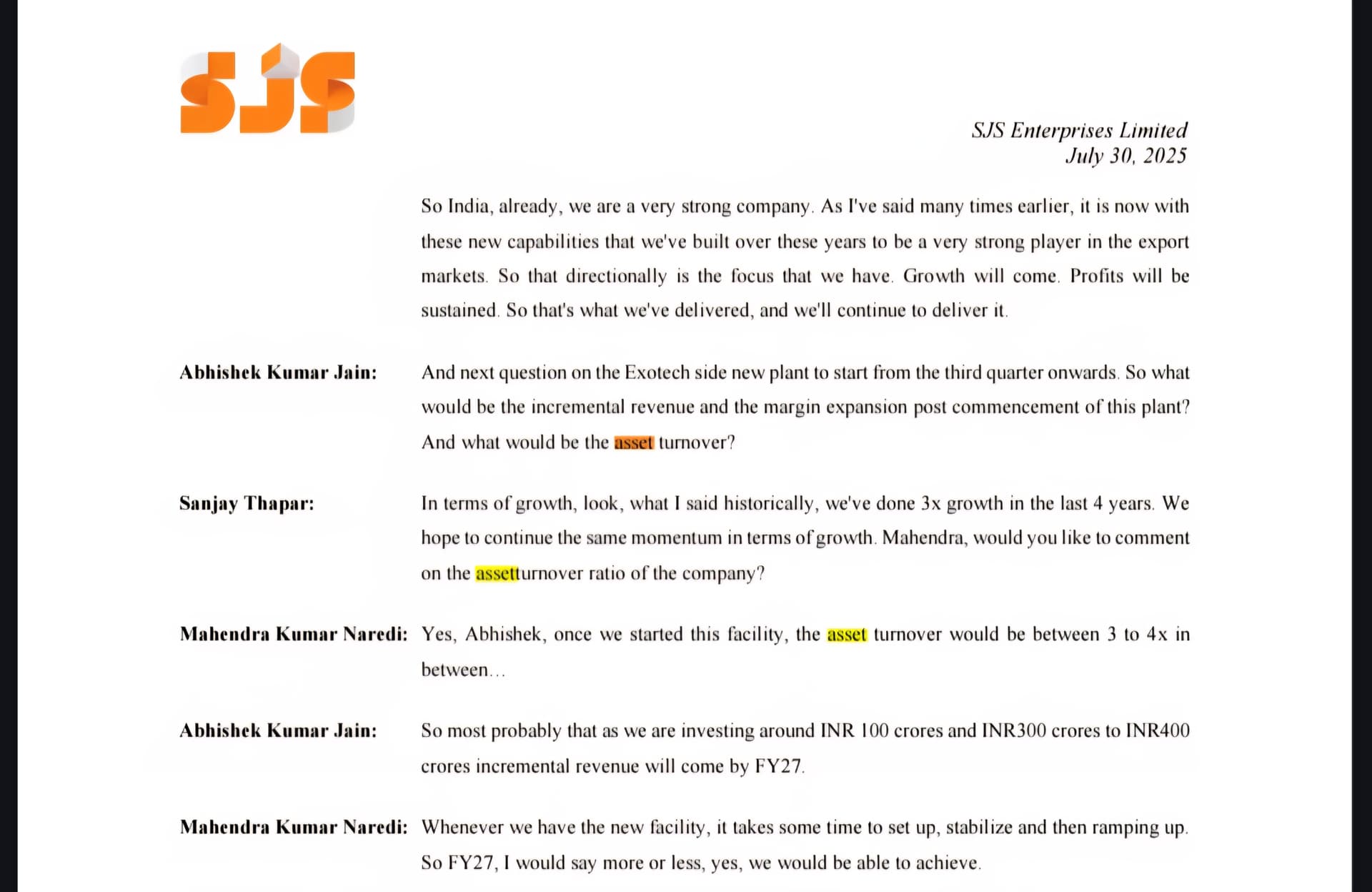

Exotech’s capacity expansion through a new plant is informed by economies of scale and disciplined investment, with a projected turnover of 3x-4x and a ROCE target of at least 20%. This demonstrates application of investment appraisal techniques such as IRR and NPV, though the execution risks are still there.

The display glass and display program is a case of adjacency diversification, whereby fundamental design skills are pushed into more advanced technology segments. Although the potential upside is large, the timing until FY27 and absence of definite orders underscore the tension between opportunity for innovation and execution risk.

Overall, SJS Enterprises demonstrates how innovation, customer diversification, and prudent financial management can build long-term value. The main questions are whether margins over 25% can be maintained with internal funding of expansion, whether Walter Pack India can materially recover, and whether slowdowns in display technology will improve long-term positioning or lose ground.

Would appreciate hearing members’ views on these issues:

-

Can SJS sustain >25% EBITDA margins while financing both organic and inorganic growth internally?

-

To what extent is timely recovery of Walter Pack India important to overall growth potential?

-

Do you view the cover glass/display initiative as a true long-term differentiator or a risky diversion?

-

With Hero MotoCorp on board and exports projected to increase, is customer concentration risk declining significantly?

-

At what stage should valuation multiples account for the optionality of new technology projects, in spite of risks of execution?