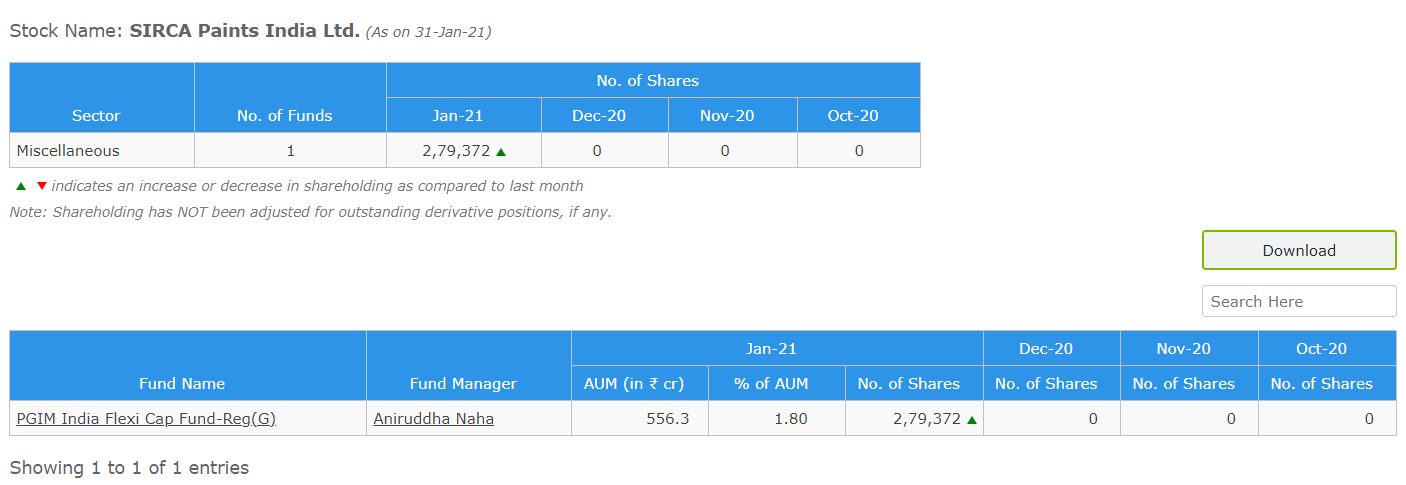

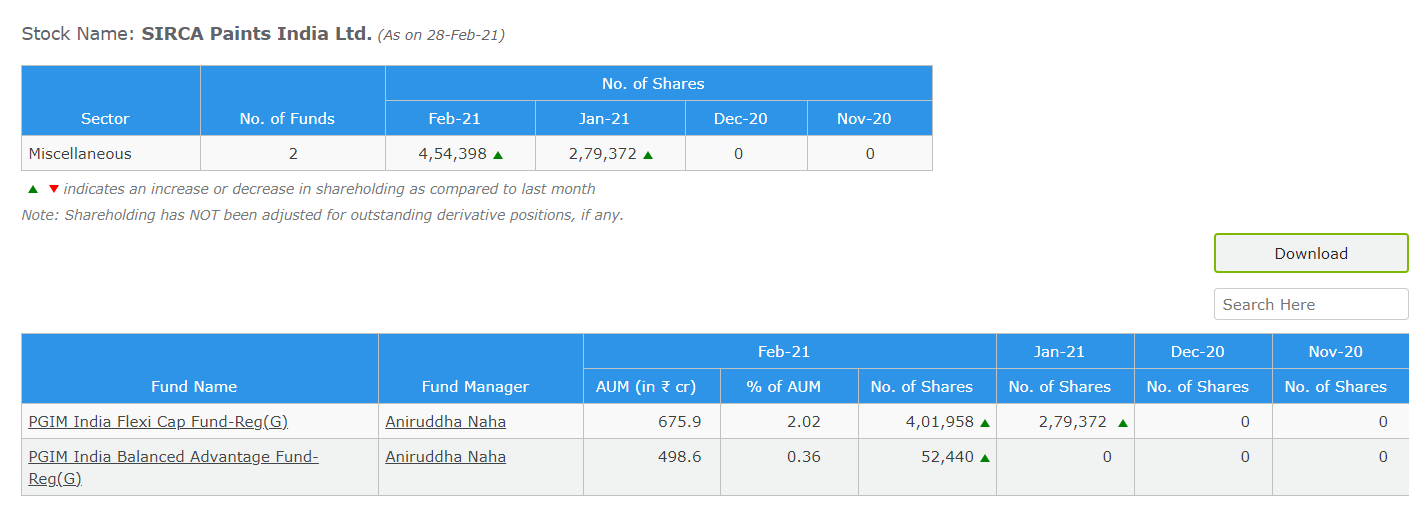

It appears a new fund has bought Sirca Paints in Jan 2021. We will come to know in the Q4 shareholding data.

What Capacity Utilization you talking about? Italy Business or Indian Manufacturing Business?

1 Like

It looks like the commodity cycle is turning. It has been a common observation that at the time of low commodity prices [crude in case of paints], such companies do very well. However, at the time of high crude prices, the share price of such stocks flatten for a prolonged period of time. Crude is trading above USD 65 for quite some time. We need to examine this aspect.

If I am not wrong, traditionally paint companies have passed on (partially or fully) any hike in input costs to customers.

1 Like

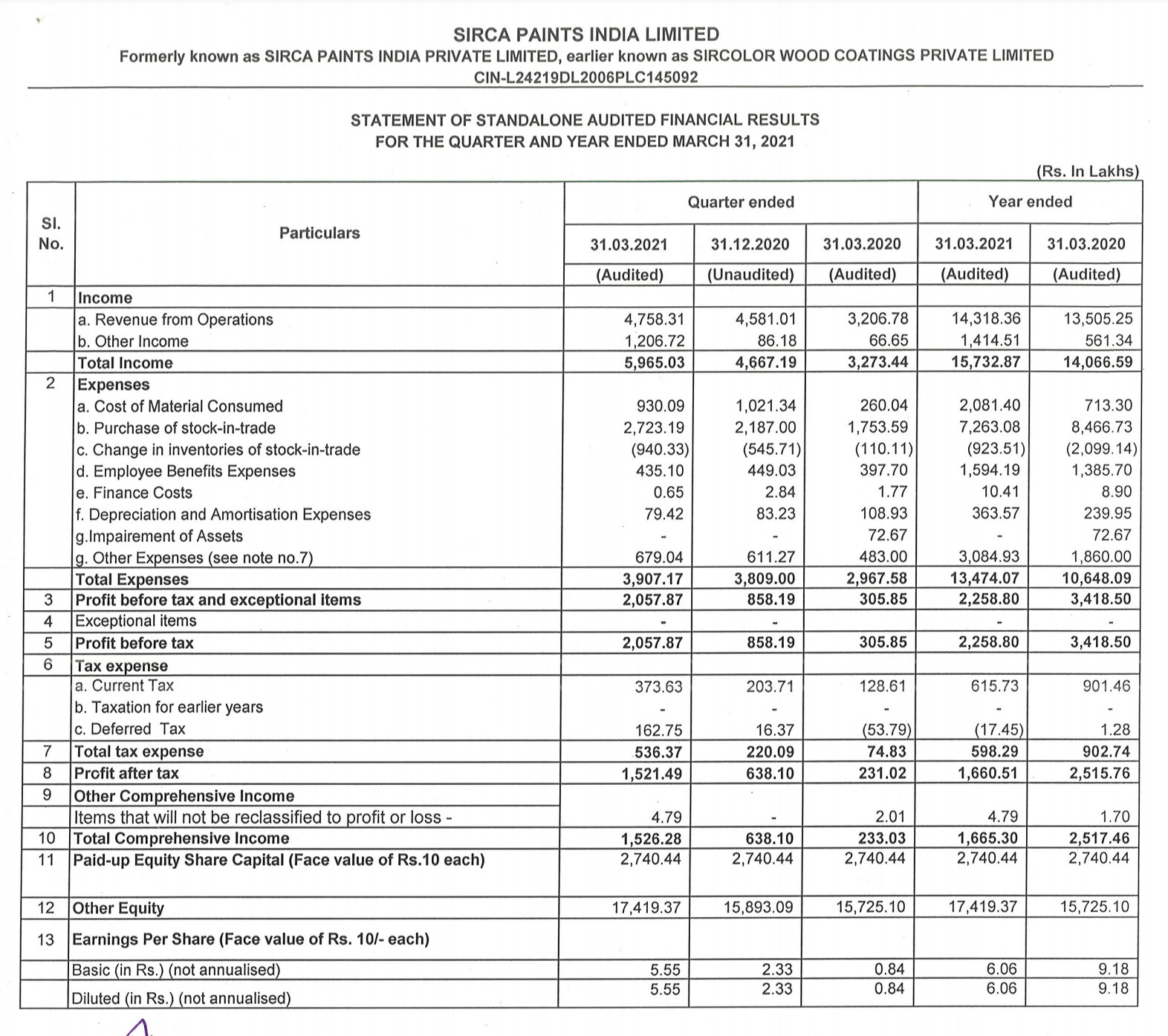

Q4 result declared

Key points:

- 1.5 Rs dividend declared

- Top line growth 6% [135 to 143cr] YoY

- PAT declined by 34% [25 to 16.6cr] YoY

2 Likes

My Comments:

- Profit figure is high due to the existence of other income. Without other income, PBT has reduced from 24 crores to 8 crores. The operating margin has reduced substantially.

- Proportion of “purchase of stock in trade has reduced”, from 62% to 50%. Thus, the proportion of manufactured items in the sales basket is going up. The company is being transformed from a trading company into a manufacturing company.

2 Likes

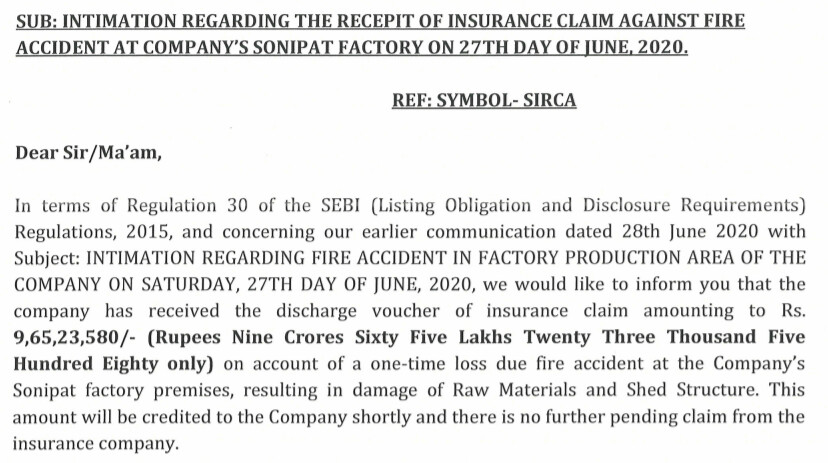

As per my assessment, Q4 results are great both on Y-o-Y and sequential Q-o-Q basis even after excluding other income that they received in insurance claim (9.64 cr).

1 Like

What could be the sources of other income as it looks bigger? One positive note is even if they are able to maintain 6 eps per quarter, we are going to have this company with a pe multiple of 15 for fy22. But I feel they would clock an eps of approx 30 this fin year which looks attractive

EPS of Rs 30!!! Please recalculate.

This year they have done an operating income of approximately 8 crores. Corona effect, accident in factory. Its understandable. It is also possible that manufactured items have low margin.

In the best case scenario, if they do 200 crores sales in current FY, they can have around 40 crores PBT [we are taking 20% PBT]. Thus PAT can be around 30 crores, eps of Rs. 11. The stock is trading around 35 times best case scenario. If by chance, margin is not maintained, p/e derating is possible.

1 Like

sorry, my mistakes. insurance part was there when i calculated. you are right

if I am reading Cashflow statement correctly, they had 1130lakh INR of property/plant sale which should be against the insurance claim. Based on my estimates excluding this impact, their total EPS should be 2.5 for the quarter. March is relatively softer quarter and Q2 & Q3 are the stronger ones. Based on it the annualized EPS of 11-12. Definitely not a cheap stock based on PE but has never been…

1 Like

Key Takeaways from the management call:

- Eyeing a 30% CAGR growth over next 5 years maintaining the margins at 20% plus and a possible improvement 100bps YOY.

- On expansion side, A couple of toll manufacturing plants is on the cards for south and west markets.

- Also a couple of M&A activities is on plan for wall paint and PU products in south / west markets

- Exports to Nepal soon, whilst Srilanka and Bangladesh is still work in progress. However expect some business to happen in Srilanka & Bangladesh in FY 22.

- Management aims to be visible as pan India brand in <2 years through aggressive marketing and distribution.

- Company is passing on the increase in RM costs to customers from time to time.

- Company is planning to install tinting machines at dealer network starting from north markets where it is very strong.

- Company has tied up with IKEA for their Adhesive range of products.

- Currently 90% of the revenues is coming from the premium imported Italian products, but going forward the revenue contribution will be 60 - 40 between Imported and Indian made.

- Eyeing a 5-10% revenue contribution from exports in the next 3 years.

6 Likes

from where can we check this ? @sameernics

1 Like

i cant find the reason company inventory as compared to sales is increasing from 23% to 46% it has come (inventory/sales)

That is because, they import a lot from Italy and stock here. Also note that the Indian manufacturing unit has only started operations last year and gradually ramping up. Whilst 90% of their business is still on the imported Sirca products. So this year onwards, you will see that mix (Import Vs Domestic) changing.

1 Like