Company ROIC & Rolling ROIIC has been going very low from past 2 years , is it because of there capex in factory and not been to utilise the factory ?

1 Like

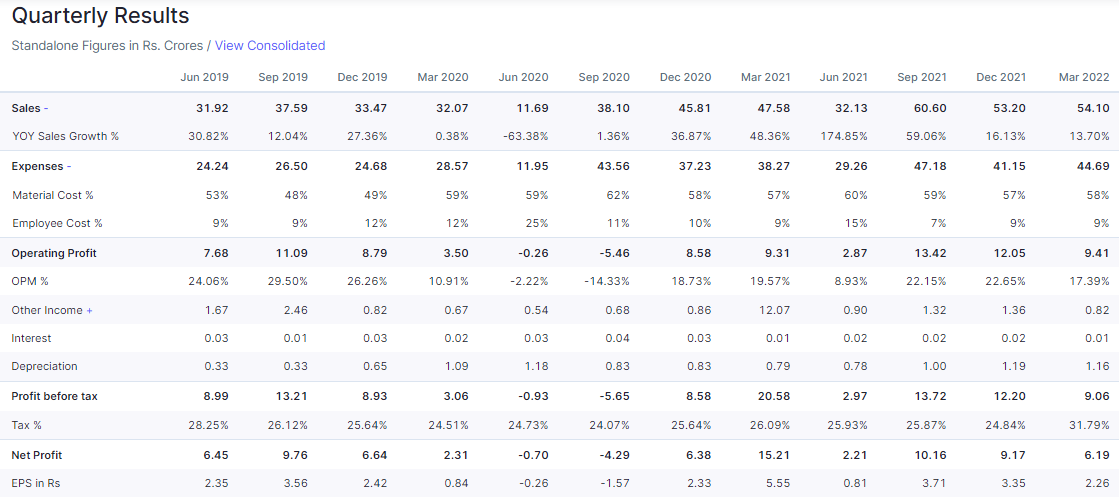

pls anyone explain about weak margins in this quarter,thanks in adavance,

invested in tracking position.

Today Sirca Paints has declared results. These are outstanding Q2 results and huge jump in revenues, PAT and EPS.

1 Like

@sameernics thank you so much actively posted about sirca regularly on this thread, invested at low level and still avgup.

Just had a quick look at Q2 investor ppt. Impressive information and I liked the positive management commentary. So we can expect capacity expansion / new manufacturing units in South before the end of FY 22.

Q2 FY 22 investor ppt.pdf (2.9 MB)

3 Likes

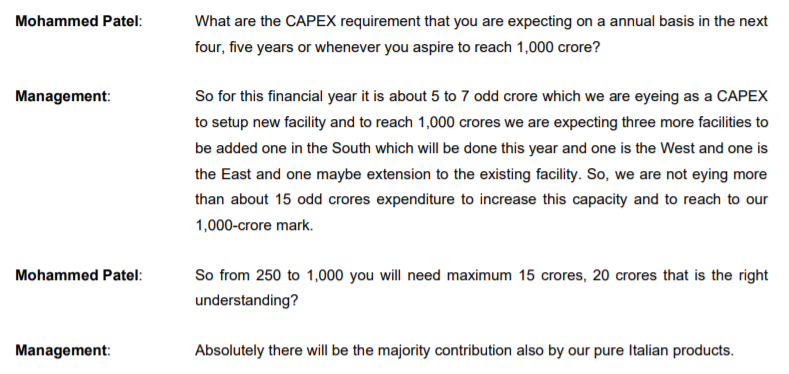

Isnt the 1000 crore number looks far fetched, it is currently averaging 50-60 cr per quarter. When can it achieve a top-line of 1000 crore ?

With no major capex required, if it can achieve that mark in the next couple of years and maintain margins, it could easily be 8-10x candidate from here on ?

Thoughts?

1 Like

I am assuming 1000Cr target is for next 4-5 years. This year they should do some 215 cr. I think with more manufacturing units in other locations (as they announced already) it should be doable as it translates to 35-40% revenue growth YOY also considering the revenue contribution would come from Italian premium and also their exports to Nepal, Sri Lanka, Bangladesh and Middle east.

Also this time, I see a new addition to the top management, Mr. Narinder - President (Sales). He is ex-Nerolac Paints with over 30 years of experience. He mentioned that his target is to increase the dealer network from the current 2000 to 6000 in the next 6 months or so.

3 Likes

1000 Cr is aggressive target, but certainly doable over the 4-5 year horizon. Specifically given that the management has been planning well ahead and has already laid down a strong foundation for the same.

Their current manufacturing capacity which came on stream in late 2019 / early 2020 itself can deliver about 225 Cr at peak utilisation. Even prior to that, the company was doing roughly about 125 cr annually, most of it through resale of products imported from Sirca, Italy. So just these two streams can deliver about 375 Cr over next 2 years. Simultaneously, in 2019 / 2020, the company had been spending lot of efforts on expanding their distribution footprint nationwide, very aggressively, expanding from 500 dealers in FY19 to over 1500 in FY20, adding 15 depots / warehouses, setup 14 Sirca Studios (Experience centres) and almost doubled its sales force from about 83 to 140+. They also enrolled 1200 contractors for their partner program. So, operationally, all the levers are well-positioned for a smooth scale up of revenue.

Their local capacity has been on stream since early 2020, so ideally we should have been the company scale up to 250 Cr range already by FY21, but a string of unfortunate events (Covid lockdown killed Q1 FY21, Fire incident hurt them in Q2 FY21, delays in relocating factory impacted Q3 and then again 2nd round of lockdown spoiled Q1 FY22) has prevented it from reaching there. So its only in Q2 FY22 now that the scale is beginning to be visible. From an average of 35 to 40 Cr, revenue this quarter has show a good jump to 60+ Cr, and they should only continue to improve from here on.

As mentioned on this thread earlier, the company plans to add more plants in other regions of India. Their capex in 2019 was in the 32-34 Cr range, so with a similar capex, company should be able to add capacity of another 200 to 250 Cr. While doing so, they will of course aim to keep growing their Italian wood coating product sales aggressively too. As of last year, 95% of their revenue contribution came from imported products. If I remember correctly, management projected a contribution of 30% revenue from locally made products and 70% from imported products. So about 250 to 300 Cr from local made products (capacity already on stream) and about 700 Cr from imported products (no specific Capex needed for this) can get them to the 1000 Cr target. Of course, this is likely to happen over next 4 to 5 years.

Recently, they have been adding new products at a fast clip, with wall putty and adhesives also part of the offering now. New planned plants will add capacities, the new sales head hire from a Tier 1 paint company with an aim to beef up the distributor count to 6000, all these are clear indicators that the management is already planning and laying the foundation for the next phase of growth to take them on the path to the 1000 cr target.

Disc: invested from lower levels, biased

7 Likes

Now a days manufacturing capacity is not a problem, it can easily be created. In paint manufacturing, it does not even cost a lot. The fundamental issue is sales- can you sell products at that scale, with intact margin?

Sirca sales has been going up at a compounded rate of 15% for last many years, doubling sales every 5 years. Even in covid lockdown, it has been maintained. Thus 1000 crores in next 4-5 years looks stretched, we can certainly expect 500 crores topline in next 4-5 years.

4 Likes

Fair point . Two points here. 1 They haven’t specified - what is few years - is it 4-5 or 7-8

2. The one unknown variable is how the other product segments of Sirca will perform. They are doing dist. of 2 more Italian/ MNC companies - one on adhesives and 1 on some wood/ wall coating, plus their own italian PU, Indian PU, wall paint etc, Maybe if all cylinders fire up, it can surprise on the upside. Having said that execution is very important here as only tie ups don’t give you revenue.

1 Like

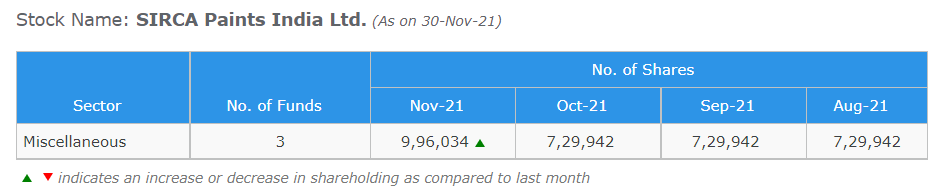

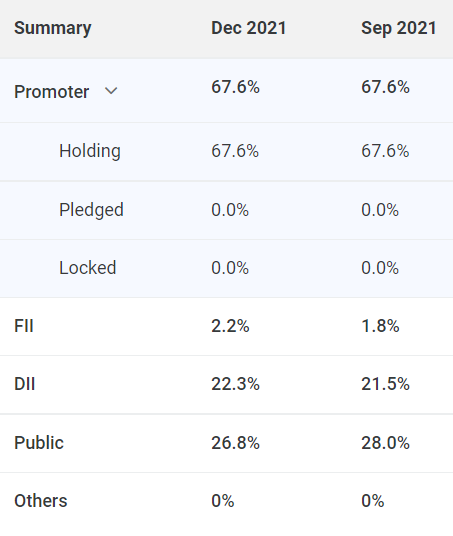

I was looking at the latest shareholding data and one may notice that FIIs and DIIs had hiked the holding in December quarter.

1 Like

Any view on Sirca’s Q4 results & concall?

Their sales is increased on YoY & QoQ, however margines are down due to cost increase.

1 Like

Looks like BGB Italia have sold out their share of the company.

SIRCA_18062022214636_Discl_Reg29_SIRCA_18062022.pdf (nseindia.com).

I’m not able to find any bulk deal, does that mean it was an open market sale?

Is it really possible to sell 18.8% of total shares in open market without crashing the stock in this kind of Market ?? The date of transaction is 2 months old - 18th April.The notification is from the depository ,not from the company . Is it posible to sell 55 lakh shares in 15 days ?

Does not seem volume reached anywhere near during those 18 days in April .Maybe its a intergroup transfer …onepart ofwhich has been notified by the depository .

the date was 18 april 2022, corect me if i wrong , what i missing, thanks in advance.

Yes its quite possible that its an intergroup transaction. From my understanding the announcement is from the company (https://www1.nseindia.com/corporates/corpInfo/equities/AnnouncementDetail.jsp?symbol=SIRCA&desc=Disclosure%20under%20SEBI%20Takeover%20Regulations&tstamp=180620222146&seqId=5047774). Will have to wait for the Q1 shareholding pattern for confirmation.