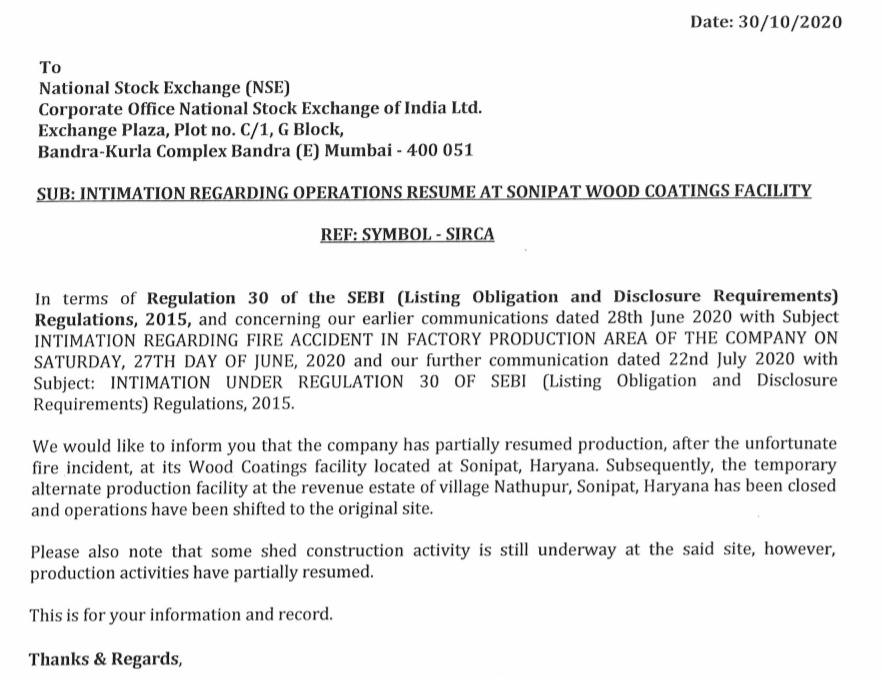

Company has today updated the exchange that they have restarted the production at an alternate site on 16th July, 2020. For more, pls visit the NSE.

Hi…Have been the VP reader for long time, may be 5 years. But this is my first comment.

Some of my observation from the screener data of this company are as below.

- Continuous equity dilution in last three years not good for existing shareholders.

- Increasing reserves and increasing trade payable, which means they have cash in hand and still not paying to their suppliers.

- Inventory and receivables on rise. Which means they are not selling what they make and they are not recovering money from what they sold.

- Till last year they were giving some loans to external entity. Not sure what it is. This year it has come to zero. Need to see if its recovered or written off as i don’t see a clear entry in cash flow.!!

- Don’t understand why they raised money from equity when they are showing good cash in hand. Is it to make themselves look cash rich at the cost of investors ?

- Inventory turn over on decline year after year.!!

- From available 5 year data, cumulative PAT reported is 98 cr whereas cumulative CFO is only 23 cr. And FCF is (-)14. Looks like they have hard time collecting money from existing buyers.

8.Exponential rise in franchise is bit of worrying to me since I have seen a similar trend in vakrangee !! - Recently started to pay dividend. But looks like this money came from shareholders themselves and not from their business!!

- Debt is reduced to near nil.

Overall, All theoretical parameters are on rise and practical parameters are on decline.

I think too many red flags for now. But Anything can happen since this is a small company and controlling by a bigger owner can change things fast… Lets see where it goes.

For me, its a no no company.

Dicl : Just studied numbers.

8 Likes

Hi @shridharbshenoy,

-

Equity dilution in FY19 was because of the IPO. Not sure about FY20 need to wait for the annual report.

-

The trade payables of Sirca India are mainly to Sirca italy and as a percentage of purchases has remained roughly the same and this isn’t necessarily a bad thing, this actually helps the company’s cash conversion cycle.

-

Their main business is the distribution of the products from sirca italy, hence they need to have high inventory at most times, regarding their receivables they have mentioned in the calls that they are trying to reduce this by collecting payments sooner, this can be checked in the balance sheet when the Q2 results for the year come.

-

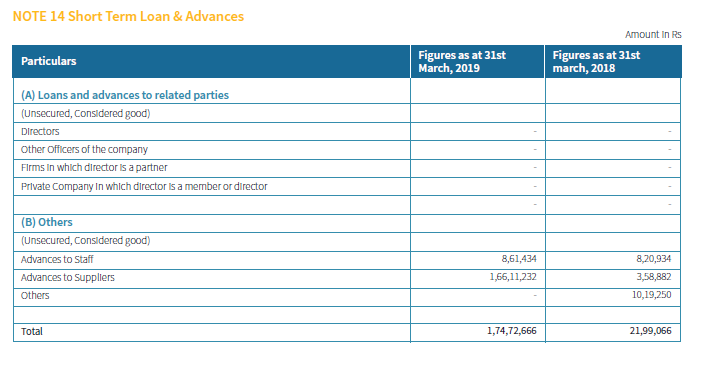

The loans they have given are mostly to suppliers. PFB the note from annual report

-

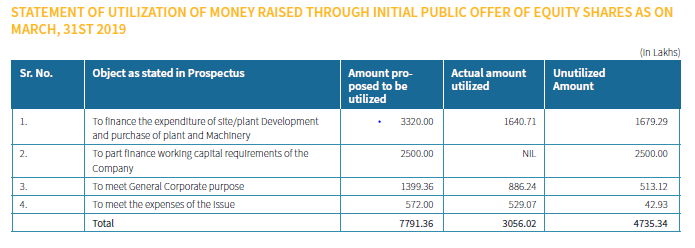

They have given the reason for raising money from IPO and even the utilization details

-

Inventory turnover has been reducing from FY15-FY19 only in FY20 it has increased possibly because they stocked up due to COVID19

-

Their CFO is less than PAT mainly due to the huge inventory.

8.They are trying to become a PAN India player which explains the rise in the number of dealers. -

I don’t quite understand what you mean here.

-

Having zero debt is really a good thing, especially in uncertain times like this and there is low risk of company going Bankrupt.

Disc: Invested

8 Likes

Hi Hemendra.

I agree that as a business, they will have to do a lot of difficult things. Just that right now they are walking on the tight rope and pose high risk as an investment. It’s just my opinion. I think a business will take lot of time for organic growth. So I would like to watch their performance in times to comes rather than jump with high hope.

Regarding equity dilution, I would be happy when they show growth with money they have in hand instead of taking additional money by way of dilution. I think they could have very much sold inventory and earned money and created wealth for shareholders instead of wanting to have more shareholder with pre existing concerns. Anyway, it’s my way of seeing it. As you said, the management may have other plans , and need to see how it unfolds.

Payables, in my opinion, is healthy when you keep your suppliers in good health. Starving them always in not really good. But here more or less the payment to parent company I guess. I don’t know to what extent the shareholders of parent company would want to tolerate it.

Infact I see receivables growing quite consistently, but as you said, let wait for upcoming report.

Hand holding suppliers would be a good thing. But I think it poses a risk of default in uncertain times. Hand holding with good performance will surely be a good thing. Here performance is when suppliers gives back money from sales.!!

Regarding inventory, I saw it from last year annual number. So I’m not sure if last few months lead to such huge inventory and if so, why they wanted to do it pile it up with looming pandemic. I’m concerned if their product have defined shelf life and can render useless after certain duration. Not sure about the shelf life. I assume 2 years time.

Point 7 which is about CFO and about growth is covered in above points.

Point 8, I meant to say that I see piling up inventory and receivables and even then they paid a dividend. Since they raised money from ipo, It seemed to me that the part of money raised from ipo got paid back in the form of dividend.  I covered my point regarding this dilution.

I covered my point regarding this dilution.

And debt, surely it’s a good one and I just mentioned it as I expressed whatever I saw.

Overall, I see more risk as a company and investment. Let’s hope their parent would want to take them on solid growth path by supporting.

(Disk: There may be typing errors)

1 Like

It sounds you haven’t looked at their management investor con call transcripts. You should find most of the answers to your assumptions.

3 Likes

Yes…I have not seen. I just wanted to put the not so comfortable parameters are seen from financial numbers only.

I think a growing business will give enough opportunity in long time to come. So I tend to like the past record. Hoping for future performance gives some additional risk to investment as many conditions in world are really uncertain today.

For now, I do a wait and watch on this one, though I agree that this can be a good opportunity if outcomes are there in future.

3 Likes

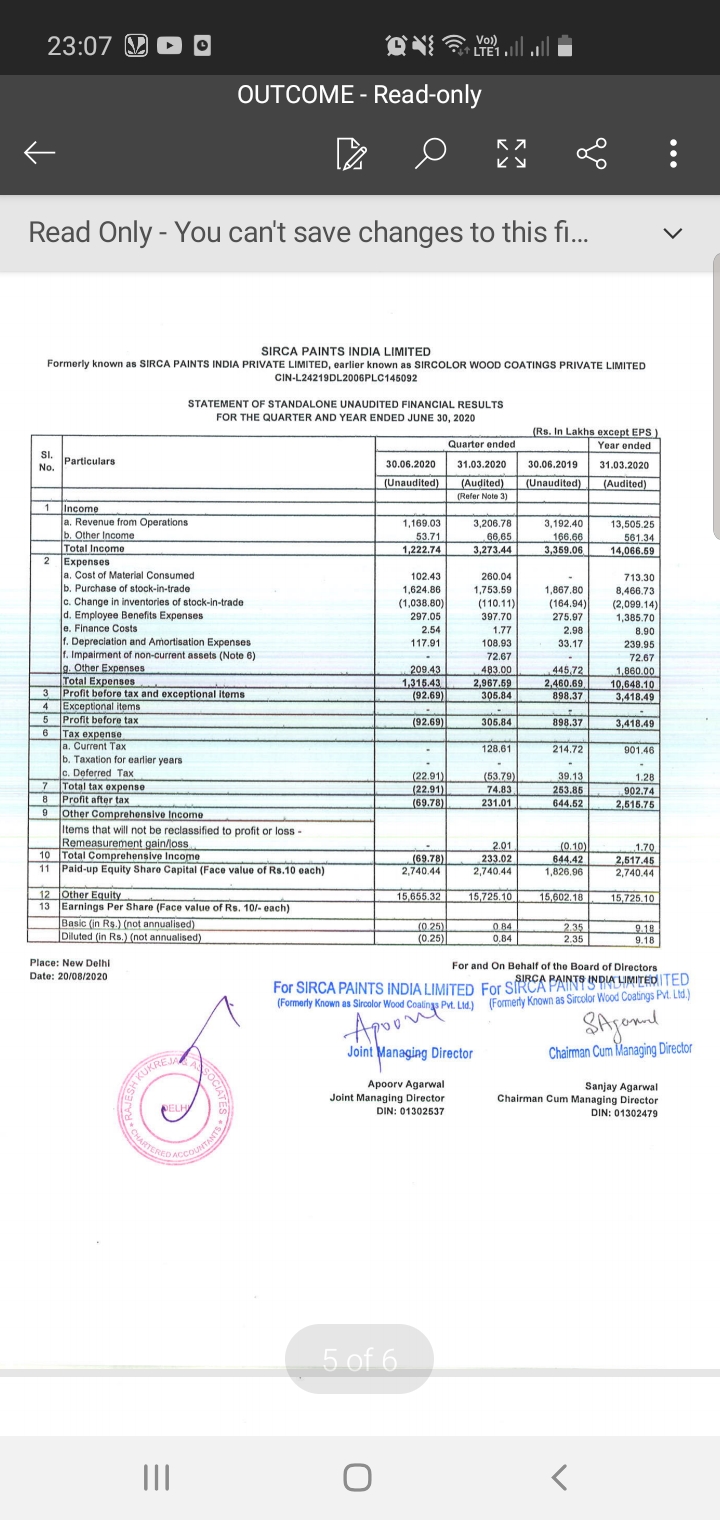

Not so bad considering the situation and how the industry is doing? Views invited. There seems like a big jump in stock in trade inventories

Revenue down by approx 50% yoy

Net loss of 60 Lacs

1 Like

Dear Akshay,

As I gone through the information available, Sirca paints looks like a avoidable company. Management seems to paint a Rosy picture with the IPO money.

- There are just doing a trading business.

- They manufactured a plant with IPO money but technical feasibility not explained. In my opinion there are lots of doubts about this plant and it’s parent firm also (i.e., Sirca paints Italy).

- The new plant got major a fire accident but management statements are very surprising as they tries to show it as a very small event and from an alternative place they are able to function normally. How this is possible, If it is not a trading company?

- They are showing very good numbers with the IPO money? things seems like that… As on one hand their inventories are piling up but they are giving dividend…

Requesting you all to please enlighten me if Imy views are wrong…

Disc: Not invested.

2 Likes

Q1 results were expected to hit a low, and so in that sense it does not carry any surprises. Post the massive rise in inventory seen in previous quarter (due to supply concerns from Italy due to Covid), there’s a net addition of another 6 crores of stock in trade inventory in this quarter, so that’s clearly pulled down the bottom line really, else that number could have been in positive territory.

More than 1 month was lost in lockdown and that of course translates straight into lost sales. Topline is roughly 1/3 on both YoY and QoQ basis. Now this indicates that even in the approximate 2 months of operations (assuming May and June), they clocked roughly about 50%-60% of pre-covid average sales. Clearly the sale is slow, and far below the pre-covid levels.

In their con call, the management had said they were hopeful that they expect the sale levels to return to normal by month of July 2020. Though most parts of the country are now gradually open for business, economic activity and intensity still is by and large subdued and dampened, so there is a very real possibility that the slow pace of sales may continue to spill over into Q2. In that sense, it may be prudent to brace yourselves for another subdued quarter, though not to the extent of Q1. It would be a very pleasant surprise (and a welcome one too!) if Q2 topline is close to 30-32 cr mark.

There another interesting observation from the decisions of the latest board meeting

- They have approved a decision to manufacture white cement wall putty at their unit in Rai, Haryana. Not sure if I had missed this completely in past years management commentary, but this comes as a surprise for couple of reasons. First, they had not yet fully stabilised their production from units local units, nor have they scaled it up yet (wall paints, primer, economic melamine etc). Second, the fire incident has obviously caused another business disruption (though temporary), and they have had to relocate their plant, so is it prudent to plan / launch another totally new product at such a time, instead of tackling and fixing current challenges.

The AGM is scheduled on Friday, 18th September 2020, so it will be interesting to hear the management, specially on the post-covid recovery curve, and overall outlook for the rest of the fiscal year.

5 Likes

I am sure, wall putty product will very well complement their wall paint as both go hand in hand in the market.

1 Like

I am sure, if a company do A, then do B, they will grow at C%

But without the cogs of production & efficiency, without the company, delivering an ounce of what they promised for their production.

Is it really so easy that a company that is posting loss this quarter, will excel at something completely new, how optimistic could one be?

3 Likes

I agree. In Wall putty and wall paints business, theirs would be like any other commodity product (though there will be some rub off from the brand given the wood coating business). The wall business is just a distribution play to try and get a decent share of the distributor basket.

What is imp. is to watch out whether they are extending themselves too thin by focussing on too many products (wood coating… disinfectants… wall paint … wall putty).

Disc - invested.

Just copied Q1 management commentary. I am very optimistic of the future of Sirca as long as they are doing all the right things. There are few new product launches during the quarter and the reasons also mentioned why they have launched. It sounds now their wall paints is picking up faster than they originally estimated.

Full presentation in NSE.

2 Likes

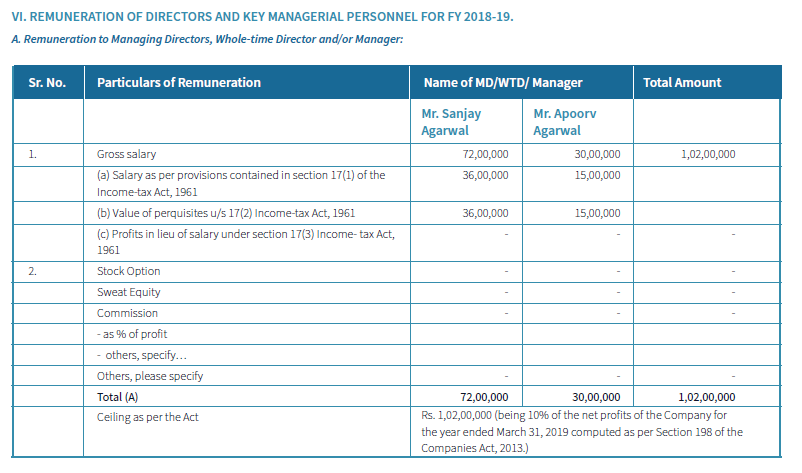

For the last two years, the total remuneration of KMP’s is exactly equal to the ceiling. I find this little odd since the exact profits for the year wont be known in advance and there seems to be no variable component as well. Am i missing something?

Also the management compensation has increased by 30% while the average employee salaries have reduced by 20%

Disc: Invested

2 Likes

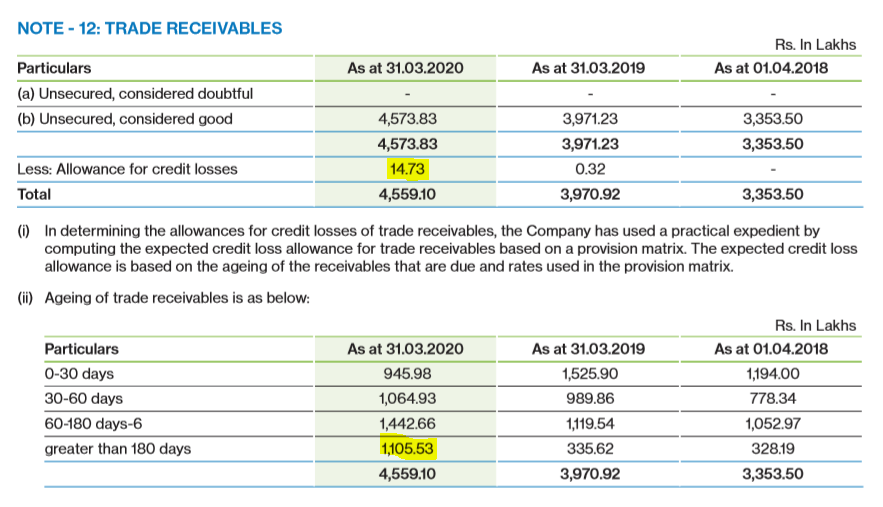

Hello,

I saw another issue in the recently published Annual report. Under Trade receivables, they have 11.05 crores pending since more than 6 months but have still accounted almost nothing (14 lakhs only) under allowances for credit losses.

It looks to me that the company is hiding the true picture on receivables and the impact would be severe in months to come. Anybody who has any udpate on this?

Disc: Invested

10 Likes

Hi,

I dont have any exact info on the credit losses part but I would like to address the overall scenario on the receivables front which is a major part of Working capital

So mgmnt have said in the con call about the new 7-day payment policy which is surprisingly very aggressive as compared to their existing 60 days

This one move will substantially reduce the working capital overhang and we will be able to see better operating cash flows.

My personal take was why will any dealer take that offer and will retaliate and will not do business in the future but I did some channel checks and confirmed from him the new payment policy. He was first stumped that how I know this  then he confirmed that this is true and the majority of dealers are accepting this as they have shifted towards cash business with their customers as well which earlier was credit business.

then he confirmed that this is true and the majority of dealers are accepting this as they have shifted towards cash business with their customers as well which earlier was credit business.

The 2.5% discount is being taken by the dealers with open arms

Now bringing attention to the wall paint segment :

The wall paint segment is doing surprisingly well as compared to the mgmnt expectation, I personally used Sircas emulsion plastic paint for my home and the quality is comparable with Asian paint royale category. The dealers are pushing this product as they get way better margins from Sirca

Overall i think the company is well poised for the future, I mean you are getting a dominant player in one consumer-facing category at such a low market cap which is expanding - it sounds good

Furthermore the mgmnt follows what it says - in the previous concall they suggested to improve the debtor days condition and they are doing a good job handling it

The new Indian PU UNICO series will also garner a better market share as it will be their entry in local PU with a good known brand name being pushed by the dealer initially and the consumer actually likes Sirca products (I have personally done channel checks with some carpenters, painters) so ultimately they have a good brand recall which is invaluable.

Disclosure: Invested

9 Likes

Great to see one of the PMSs seems recently entered Sirca Paints.

Source of info: Today’s money control article. Beating lockdown blues: 20 stocks from top 5 PMS schemes gave 60-90% return in 6 months

1 Like

Negen founder holding sirca since listing

He follows Joel Greenblatt style

3 Likes

Neil bahal was the one who identified sirca

He gave a presentation and since then i have been following the company

1 Like