The company disclosure on accident and damages is available in NSE site.Sirca Fire Intimation.pdf (666.5 KB) .

Entire IPO proceeds were invested into this factory and working capital also large part was stored in this factory… management disclosure seems like it is trying to play down size of event (if you see videos above)… And this factory commercial production had just recently started after numerous delays… Hope it is as small as they say since I am currently invested but this looks very concerning

Well, if you don’t trust their disclosures, then you have invested in a wrong company i guess. Take informed decisions or call the company directly to find more details and share to all of us.

1 Like

Yes that is true, I hope I am wrong since I do own shares.

However from the videos itself does not look like minor shed and raw materials damage only; looks like much larger impact. Plus this was their largest actual production plant and they had stressed WC cycles anyway… wonder how long insurance money will take to come back and looks like they will for sure take some time to restart above factory

Copied below from their disclosure if at all you trust?

“It is also informed that the company has on this date enough finished goods to cater the current market demand. Further company is also working to arrange temporary place to restart the production activity immediately.

The company is taking all adequate steps to ensure re functioning of the affected unit at the earliest.”

Thank you, had read that. Also article says "The damage from this incident was restricted to the loss of raw materials and shed structures. The

finished goods and RCC structures remain unaffected from this accident. However the plant and

machinery condition seemed to be okay at first sight but needs to be evaluated. "

which is what leads me to make the above points… I guess truth will show up tomorrow/few days as media reports etc. start coming in and there is more clarity overall

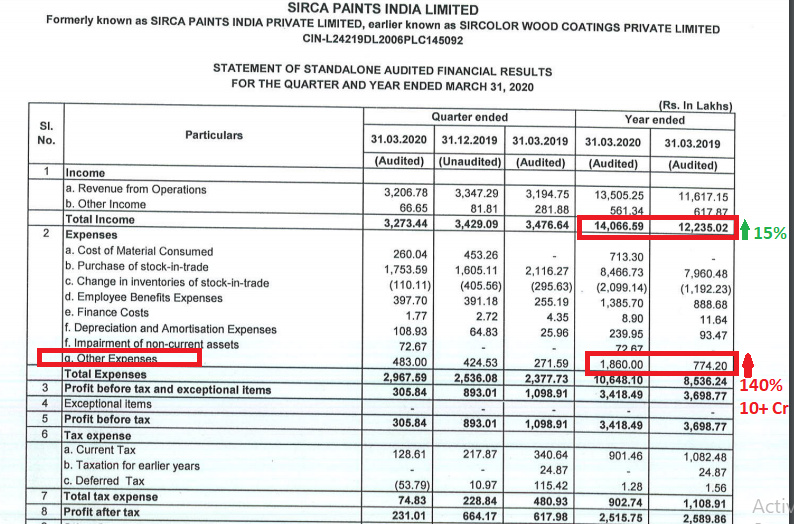

Q4 results have been declared and the same is available in NSE site.

One could see COVID impact on their Q4 performance as is the case with most of the companies.

For full year the revenues jumped 15% and PAT at 25.15 cr, which remained same as last year (25.89 cr).

SIRCA_29062020164856_OUTCOME.pdf (3.6 MB)

Thanks sameernics. Overall considering march was a washout I’m pretty happy with the overall FY result. This is one of my favorite stocks but atm I’m glad I’ve just dipped my toes in with a quantity of 50. It will feel a lot of pressure with what may be perceived as flat results and the fire at the factory plus a washout with Q1. Will pick up a sizeable quantity around Q2 when hopefully all these issues are behind them and everytjing is back on track

Q4 figures are not much out of line. Revenue dip of just 4.19% sequential QoQ and a negligible improvement of 0.37% YoY. Slightly surprising are the full year numbers. FY20, there is a decent revenue increase of appx 15%, yet PAT shows a slight decline of 2.86%.

Appears that Other expenses have dented the PAT, more than doubling to 18.6 Cr (from 7.74 cr), so it would be interesting to dig into whats behind that spike.

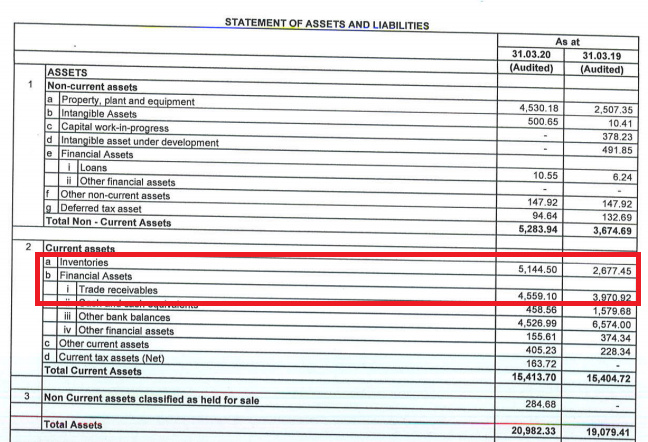

On balance sheet, the inventories have risen sharply too, almost doubling (92%) from last year, a spike of 24+ Cr, probably in an effort to stock up beyond normal limits due to Covid situation. Sirca receivables have always been high (probably providing credit to dealers during the critical expansion thrust pan-india), and have grown further to about 45 Cr now, that’s 33% of the annual sales figure… So that’s a metric to be watched very closely, especially in the current financially distressed situation due to the pandemic.

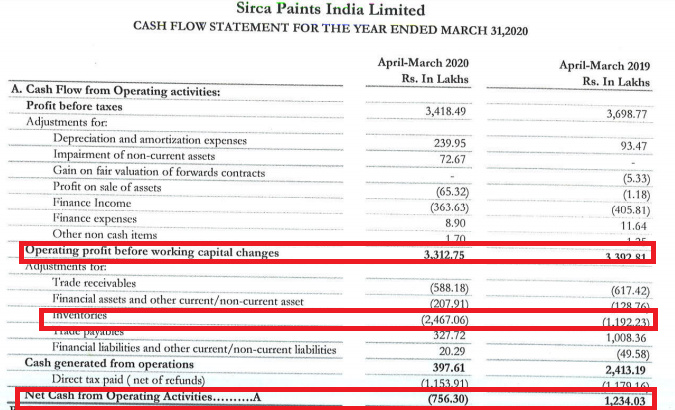

CFO has turned negative for the year…again primarily due to working capital changes arising from 12+ cr addition to inventory, doubling from previous year.

I think, fundamentally the company is doing well, though the Covid situation will definitely stress test the company, and if they emerge stronger from this, it would be one to watch out for. We’ll also have to wait and see the extent of damage & disruption caused by the if the fire incident … hopefully its nothing much.

Discl: Have a very small tracking position. Looking to add on dips.

5 Likes

The management has invited an analyst / investor conference call for Q4 results tomorrow at 4pm. It is good for all serious investors to attend and ask all your questions.

SIRCA_30062020163013_INTIMATION.pdf (720.3 KB)

2 Likes

Sirca Q4 Investor Presentation is available now at the link below

https://archives.nseindia.com/corporate/SIRCA_01072020174108_Intimation.pdf

Also, here are some quick notes from today’s Con call. Apologies upfront for any mistakes that may have crept in the notes, though I have tried to be as accurate as possible.

-

About 2 weeks worth of year-end sales impacted due to Covid lock down. Usually, this is the time when dealers pick up volume to meet yearly targets.

-

Management estimate is about 10 to 15 cr of sales impact

-

Huge inventory rise is due to

a. Increase in raw material inventory for local manufacturing

b. Higher procurement of finished product inventory from Italy, due to uncertain situation. Management says they now have inventory of 8-10 months with them. About 16 containers were shipped from Italy during lockdown

c. Shipments to dealers were held-up / delayed due to lock down situation -

Sales / Infra expansion continued this year, and is now complete to the planned level pan-india

a. Dealer network expansion has continued this year too, and is now up to 1600

b. Sales team expanded to 146

c. Branch / Depot count expanded to 15

With this, base is ready for sales / revenue expansion. No more infra expansion planned for next 1-2 years -

Receivables

a. Company trying to reduce the receivables now

b. Have implemented a new 7-day payment policy for dealers and 15-day payment policy for OEM partners

c. All new sales post-lock down are being done under this new policy

d. response from dealers and partners has been encouraging so far

e. Company giving an additional discount of 2.5% under this arrangement

f. Sales impact unlikely, as the dealers themselves are NOT extending credit to their own customers

g. Company is hoping that this will be the new default policy in the industry going forward

h. Other top competitors are also following similar reduced credit policy

i. Company has given an additional 30 day period for making old pending payments (pre-march 2020).

j. Company has run a campaign with dealers to provide additional discounts on clearing old payments and they have seen encouraging response on this too, and many dealers have taken advantage of this. -

Fire Incident

a. Management assessment is in line with what they have already declared in their disclosure

b. As per current assessment, the fire started from RM (for local manufacturing) store area and spread to store / shed nearby

c. No damage seen to the finished goods imported from Italy

d. No damage seen to the machinery

e. Premises was covered at 100% under insurance

f. They have identified a temporary location nearby from where they plan to restart production in about 7 days

g. They have finished goods inventory of about 10 days, and they plan to restart production in 1 week, so they do not envisage any opportunity loss due to lack of finished goods

h. Full assessment of the value of raw materials lost in fire will only be possible once they start clearing the debris from site… they will get permission to do it in next 2-3 days

i. Current location plan will restart only 3-4 months later

j. Overall, no impact seen on sales / revenue due to the incident -

Post-lock down trend

a. Sales has picked up, particularly from Tier 2 and Tier 3 cities

b. Gradually, sales has shown strength, specially in North India region. Sales pick-up is slower in Southern region and Maharashtra, given the lock down restrictions still in place

c. They expect the sales to be back at pre-covid levels by July 2020, provided if there are no shocks such as another round of lock downs etc -

Outlook for current year

a. Situation is still uncertain, so no specific sales target shared for current year

b. Despite loss of sales for 2 months, they are optimistic about making up for lost time in the remainder of the year, thus achieving similar sales levels as last year, with some upside, if all goes well -

Outlook for next 2 years

a. They expect to grow well in FY22 & FY23

b. Can see growth of about 20% + in Italian PU segment

c. Grow the volume in wall paint segment by about 4 to 5 times

d. Grow the local PU segment 25% to 30% (not sure if this is per year figure or cumulative)

e. Gross margins to remain more or less same as current i.e. 42% to 45% and EBIDTA margins of 25% to 27%

f. Imported as well as local products have similar gross and EBIDTA margins

g. Expecting strong EBIDTA in these years

h. Enough infra / head count in place to support strong growth in next 2 years -

Market Share

a. About 22% - 23% market share in Italian premium PU coatings

b. Pidilite-ICA has around similar market share

c. Asian paints market share is about 40% to 50% higher than Sirca (so about 33% appx)

d. Sirca and Asian paints are the price setters in the premium segment

e. Company’s central focus will continue to remain on Premium PU product segment -

RM Prices and RM sourcing from China

a. Most RM are easily available in India, so no specific dependence on China

b. RM prices are of course dependent on Oil prices, but in short / medium term this is not a concern -

Local manufacturing

a. Local manufacturing is focused on economical PU & Melamine products, as well as Wall paint

b. No plan to locally manufacture products which are currently being imported from Italy

c. Last year 32 cr of CAPEX, no CAPEX outlay for current year -

Sirca Parent

a. No disruption seen in plant / production in Italy, even during the lock down

b. No royalty paid for sale of Imported PU products

c. Royalties are however, paid for products manufactured locally in India. Local products sold under brand Sirca Unico brand

d. Parent planned to increase shareholding to 10% level, and just prior to Covid crisis blowing up, discussions on this were complete already. However, due to crisit, Sirca Italy is caught up in some challenges so this will be delayed. -

Sanitiser Product Line

a. Received license around mid-June, began production a week later and within next 1 week the fire incident disrupted the production.

b. Plan to manufacture about 6000 to 7000 litres of sanitiser per month

c. will be distributed through existing channel / dealers, so no added cost on distribution

d. Priced at about Rs 150 / litre -

Product Mix

a. In FY20, 95% of revenue comes from imported products

b. About 5% of revenue came from wall paint (local mfg)

c. Going forward, the revenue from imported products is planned to be about 70%

d. Remaining 30% revenue to come from locally manufactured products, with 20% from economical PU / Melamine and 10% from wall paint -

International Expansion

a. Agreement signed for Nepal, plan to open a studio there very soon, and first dispatch of product within next 1-2 months

b. For Sri-lanka and Bangladesh, discussions are underway, and something could firm up in Q2 this year

c. In Dubai, commercial discussions are underway

Overall, I think they seem to be in control of the situation, and have taken some good measures to counter the current set of challenges.

16 Likes

Thanks @bhambani. for being first to post.

I also did capture few notes, hope more or less same with yours.

Highlights of Todays Management Concall.

I am not going into details of Q4 business performance update as it is already mentioned with reasons in the investor presentation and is available in NSE site. What I am summarizing here is the key highlights of today’s call with analysts and investors.

Fire Accident update:

The raw material section and the shed is affected. However their finished goods and the machinery at the first sight are unaffected. A detailed survey is underway to assess the overall damage. The good news is the management has identified a new place to manufacture those moving Indian products which were currently being manufactured. This manufacturing will start in 7-10 days time. Whilst the current facility expect to resume in 3-4 months time. Currently there are enough finished products for 10-12 days period. So the management expect no loss of sales or market opportunity due to fire incident. Entire factory is covered by insurance.

New Business initiatives:

- Reducing trade receivables

The company has implemented a new policy post COVID, a 7 day payment policy in retail. As a result a significant improvement in trade receivables is expected in from the new order onwards. Which means for all retailers it will come down to 7 days as compared to current 40-45 days and for OEMs it will come down to 15-20 days as compared to current 60-90 days. Also they have given a 45-60 days timeline to clear any old outstanding. So the company is seeing a very good positive shift and this will be the business and industry practice going forward. There are negligible bad debts. The management believes this shift is achievable as the dealers and contractors also do not offer any credit to their customers. The management is also constantly focusing on reducing working capital cycle and will see a good improvement going forward.

- New product launches

The company had already launched Indian made PU products and are getting very good response in the existing market and expect it to grow 20% of revenues in this year. They are working with Alder, a company which has 60-70 stores and the results of Indian product has been excellent and price is acceptable. Also working on couple of more and the product results has been excellent. Company also launched Hygiene plus and Hand sanitizers considering the need of the hour. The license for Hand sanitizers was very recent one and they already produced about 800 litres. They expect the monthly production to touch about 6000-7000 litres. They are mainly targeting to sell them through current dealer network plus OEMs. Average price is around Rs.150/Litre.

Business outlook for rest of FY 21:

Due to lock down, management has recognized that April month is a wash out. The factory got approval to restart with a reduced capacity in the early May month. With lockdown opened up, their main North India market is seeing a good pick up. Sales are bit slow in west and south. However from July onwards the sales would reach normal pre-covid levels without any impact on gross margins and ebitda margins or any increase in the expenses. If there is no second wave of lockdown, then the management expects a good growth in the second half and make up some of the sales loss of Q1.

Business outlook for next 2 years:

Revenues from imported Italian PU, which would reach about 70% contribution of turnover (currently 95% contribution) will grow 20% plus on Y-O-Y basis. Revenues wall paints will grow 5 times as compared to last FY revenues (5 crores which started in Sep 2019) within 3 years. Revenues from their Indian economical range of PU and Melamine would be of about 25-30% capacity turnover within 2 years. Overall, the management expect to double the turnover or a bit more in next 2 years.

Margins:

Gross margins shall be at 40-45% and EBITDA margins shall be around 25-27%. These margins would remain more or less same for Imported Italian as well as Indian manufactured products.

Revenue break-up:

Currently imported Italian constitutes 95% of the revenues and about 5% Indian manufactured products as it was just started and then the lockdowns came in. The management gradually expects this will shift to 70% imported, wall paints about 10% and around 20% Indian products.

Current Market share and Competition:

Current market share in imported Italian products is around 23%. Both Asian paints and ICA Pedilite continues to be leaders in Italian PU. However, the market is growing enormously and there is enough in the market for everybody that it is not a risk to Sirca. In order to increase the market share, company is adopting different strategies such as building strong network and dealer relationship. Company will focus more on the dealer and contract margins so that they have interest in promoting Sirca in the first place. To build the network and relationship they are offering free hand sanitizers along with main products on every billing.

Export Business update:

Post COVID, recently they have signed an agreement with Reliance Paints in Nepal and a Sirca studio being setup. So within a month the operation will start and 1st full consignment will be sent from the new temporary facility. As regards to Sri Lanka and Bangladesh, still the talks are going on and will pick up some movement in Q2. As regards to Dubai, commercial negotiations are going on and just waiting for the project to restart in the middle east. Just waiting for the financial approval and there might be some positive news coming in on that front. Currently middle east is also impacted by COVID.

Italian COVID impact and the Stocks availability:

Fortunately operations of Sirca Italy has not been impacted that much and they were running the plant as usual even during lockdown. There are enough stocks in hand equivalent to 8-10 months of requirement. Due to COVID, they had ensured at least 16-17 containers arrive in May month.

Wall paint strategy:

Their foray into wall paint is based on a successful case study, which will help penetrate the south Indian market. The PU products along with wall paints will be really drive the penetration.

CAPEX plans:

The current infrastructure in terms of Depots, offices, studios and team is more than enough to achieve sizeable turnover in the coming years without any additional expenses.

Sirca SPA Italy shareholding:

Currently they hold about 2.9% equity holding and there is a good possibility that it will go up to 10% in the future.

Key takeaways from the investor presentation:

The latest Q4 investor presentation shows the dealer network increased to 1629 from 1477 in Q3 and team has increased to 327 from 310. OEM Vs Retail revenues 30% : 70%.

Disclosures: I tried to capture as much as possible from the call. There might be few miss outs due to poor audio / network issues. As already disclosed I am invested in the stock.

13 Likes

Just in case if i missed out to capture something in my post, we have full transcript of the call disclosed by the company to NSE.

SIRCA_03072020201735_INTIMATION.pdf (955.0 KB)

1 Like

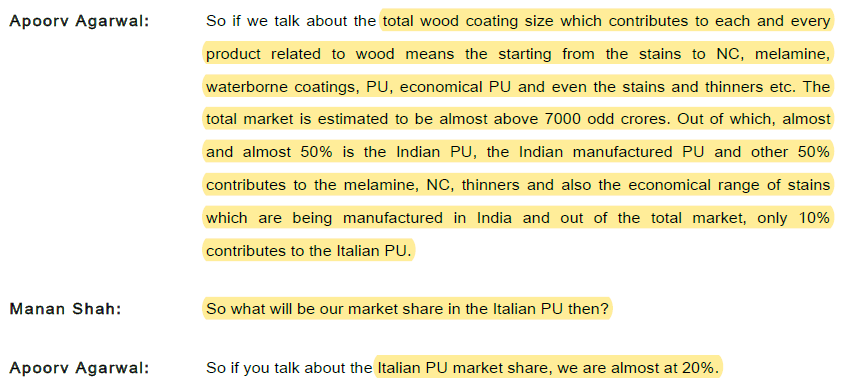

There is some ambiguity from Sirca’s management.

They claim that wood coating market size is ~₹700cr and they have 20%+ market share. However their turnover in FY20 is ₹135cr, and 95% of this revenue is from imported wood coating segment.

Disclosure : Invested

Not sure what is the source of your information for 700 cr.

Refer to Sirca’s management con call dated Nov 27, 2019, wherein it is mentioned, the wood coating market size is over 7000 cr.

So if the market size is over 7000 cr. what is your doubt? Why do you mention 700 cr then in your post?

Read - Italian PU market out of 7000cr, they have said it is 10% of this market

1 Like

Sirca Italy is going to pump in money post lockdown so that advances can be given to contractors so that they can return back. Also advances to distribution/Retailers so that they push the new economic range of products and also main aim is to remain debt free. They don’t like debt.

Also Have an roce of 40%.

Post covid they are going to concentrate on economical products so that people who will think about price post lockdown then they can compete there. So they will keep the luxury items on backseat for a while. Margins I think will take a hit here. But momentum will be maintained. Management seems like it knows what it is doing and sirca Italy is guiding them all the way through. Good thing is sirca Italy plant was not shut even one day even though you know how bad Italy was impacted due to covid. Management seems like they know what they’re doing & great thing is that Sirca Italy is guiding them through the entire process.

4 Likes

Sirca was started by two friends Mr Agarwal and Mr Bhais 20 years ago

Sirca was the first one to start PU coating in India. But first 2-3 years were tough.

First break threw came when Asian paints too start PU and then People started giving them more attention. Hence sirca was giving technical support for superior finish which other companies were not concentrating on.

They are mostly concentrating on OEMs like Godrej, Greenlam laminates & century ply. So where ever Greenlam and century go sirca has to go too. Wood sector is growing well.

They are mostly present in North & East. Now getting into retail after the IPO before they were concentrating on OEMs.

They are exporting to middle East & Dubai. They have some tie ups in places like Pune & Ahmedabad.

Last 20 years company has been debt free.

They’re expecting 35% increase in retail.

Signed a MOU with Godrej and exclusive right to give materials.

Signed contract in April 18’ to sell in Srilanka, Bangladesh & Nepal.

They’re the only company in Europe to make their own resins.

They’re looking to expand Vertically and Horizontally. Looking to expand Dealerships.

Made some notes from an interview video in 2018 with Apoorv Agarwal

3 Likes