Sirca Paints India Limited

Sirca Paints India Limited is a leading manufacturer and supplier of wood coatings, industrial coatings, and decorative paints based in India. The company was established in 2006 and has since then become a household name in the Indian paint industry.

Sirca’s products are known for their high quality, durability, and eco-friendliness. The company has a state-of-the-art manufacturing facility that is equipped with the latest technology and machinery. They have a team of highly skilled professionals who work tirelessly to deliver innovative and sustainable solutions to their customers.

Sirca offers a wide range of products that cater to various segments of the market. Their wood coatings are highly popular among furniture manufacturers, interior designers, and architects. The company’s industrial coatings are used in various industries such as automotive, aerospace, and construction. Sirca’s decorative paints are known for their vibrant colors and smooth finish, making them a popular choice for residential and commercial projects.

Sirca Paints India Limited is committed to sustainability and has implemented various initiatives to reduce their carbon footprint. They have also launched several eco-friendly products that are free from harmful chemicals and VOCs.

In conclusion, Sirca Paints India Limited is a reputable company that has earned the trust of its customers through its commitment to quality, innovation, and sustainability. Their products are widely used and appreciated in the Indian market, and they continue to strive towards excellence in everything they do.

- Sirca Paints India Limited primarily focuses on wood coatings, industrial coatings, and decorative paints. While Asian Paints is a major player in the decorative paints segment, Sirca’s specialization in wood coatings and industrial coatings may differentiate its offerings from Asian Paints’ product portfolio.

- As a general understanding, Sirca Paints India Limited is likely to have a presence in key industrial and commercial centers across different regions of India, including metropolitan areas and industrial clusters. These may include cities such as Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Ahmedabad, Pune, Hyderabad, and other major urban centers where there is a concentration of manufacturing, construction, and industrial activities.

- Sirca Paints derives a significant portion of its revenue from wood coatings. In the financial year 2022-23, wood coatings accounted for 44% of Sirca Paints’ total revenue. This is in contrast to Asian Paints, which derives only 12% of its revenue from wood coatings.

- Another difference between Sirca Paints and Asian Paints is their geographic reach. Sirca Paints is more focused on the eastern and southern parts of India, while Asian Paints has a nationwide presence. This is because Sirca Paints is a relatively newer company, and it is still in the process of expanding its geographic reach.

Concall Highlights

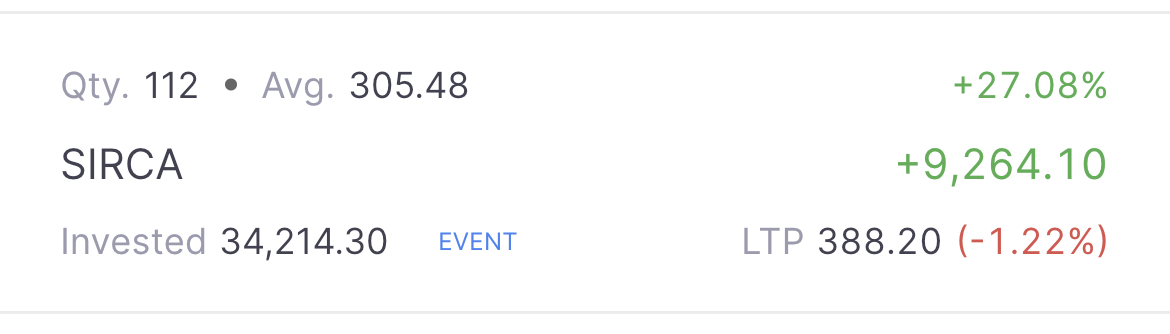

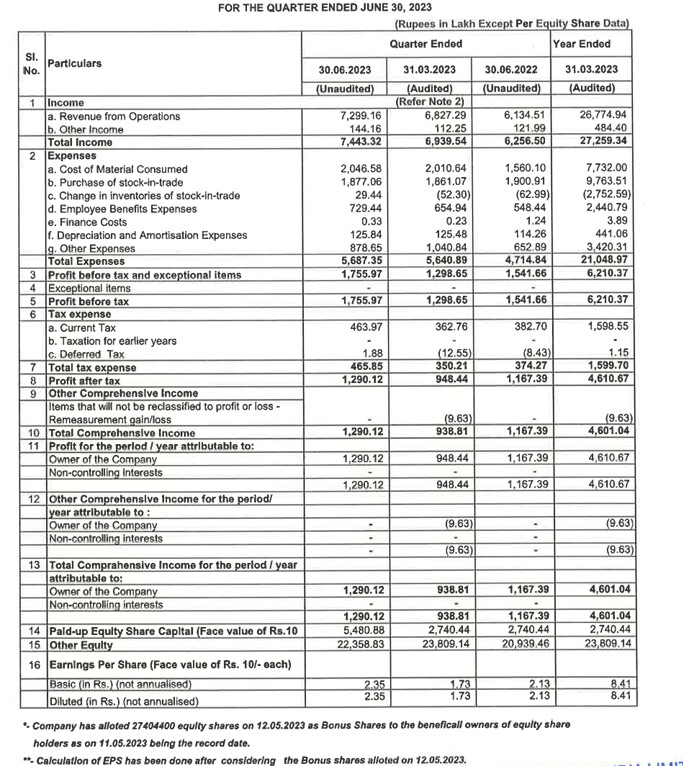

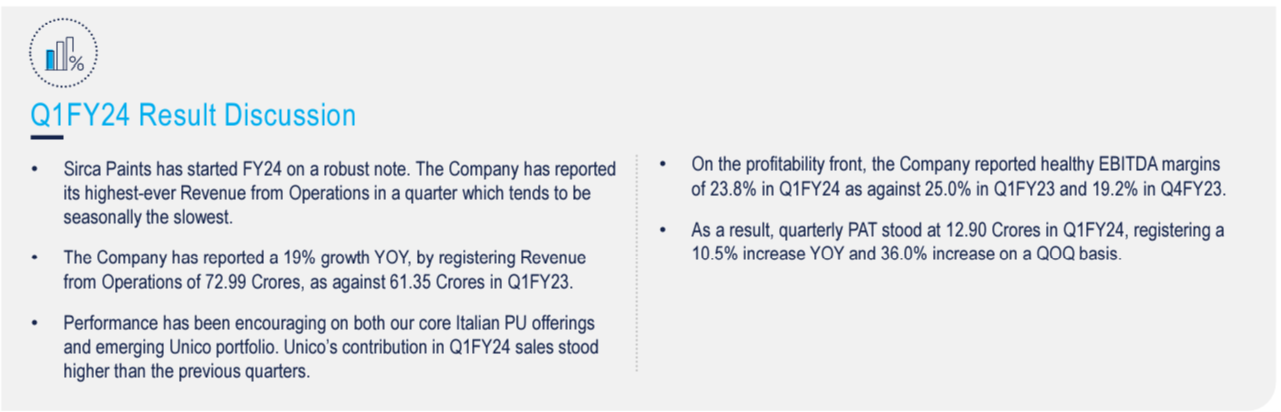

- Sirca Paints India reported a top line of INR268 crores in FY '23, a growth of 34% over the previous year.

- Revenue from operations were INR68.27 crores in Q4 FY '23, registering a 26% growth YoY and 5% QoQ.

- EBITDA margins for Q4 FY '23 stood at 19.2%, compared to 21.6% in Q3 and 17.4% in Q4 FY '20.

- PAT for the quarter stood at INR9.49 crores, an increase of 53% year-over-year and 10% quarter-over-quarter.

- For the full financial year, the company reported a higher ever top line of INR267.75 crores, a significant increase of 34% year-over-year.

- While EBITDA margins for the year stood at 23.05%, higher than previous year’s 18.9%.

- Net profit for the year stood at INR46.11 crores, a substantial increase of 66% over the previous year.

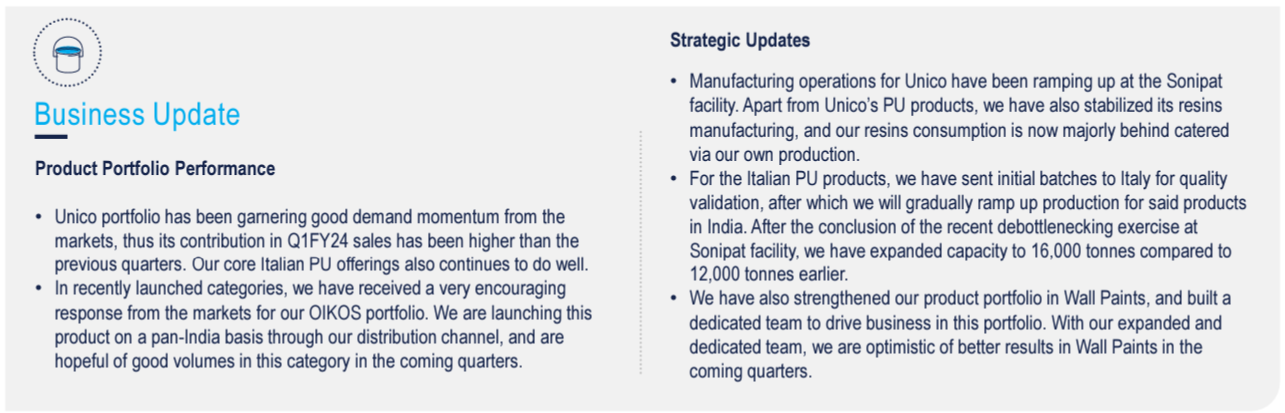

- The company has launched OIKOS, a luxury category product in the decorative paints segment.

- OIKOS is positioned as a niche product, but it is expected to help create the brand Sirca a popular brand for wall coating.

- The company has also acquired the rights to manufacture 10 different polyurethane wood coating products in India.

- This will allow the company to cut down its import bill, optimize its inventory days of finished goods, increase its manufacturing in India and strengthen its operations on pan-India basis.

- The company has also launched a new water based days coating range, D’Aqua PU.

- D’Aqua PU is a safer to use in children furnitures since it contains almost no volatile object content and emits no odor because of its water-based properties.

- The company is confident of continuing its growth momentum in the coming quarters.

Here are some of the key questions and answers from the concall:

- Q: How do you plan to differentiate yourself from the rest in the decorative paints space?

- A: The company is planning to launch a number of innovative products, including texture paints and solid paints with 200% more coverage.

- Q: What is the current capacity utilization and how much sales can be generated with full capacity utilization?

- A: The current capacity utilization is around 75%. With full capacity utilization, the company can generate sales of around INR350 crores.

Overall, the concall was positive and the company is confident of continuing its growth momentum in the coming quarters.

Downside

Sirca Paints is a well-established company with a strong track record of growth. However, there are some potential downsides to investing in the company, including:

- The company’s high valuation: Sirca Paints’ P/E ratio is currently around 41, which is considered to be high. This means that investors are paying a premium for the company’s stock, and the stock price could be volatile if the company’s earnings do not meet expectations.

- The cyclical nature of the paint industry: The paint industry is cyclical, meaning that demand for paint tends to fluctuate with the economy. This could impact Sirca Paints’ revenue and earnings if the economy enters a recession.

- Competition: The Indian paint market is a competitive market, and Sirca Paints faces competition from a number of other well-established companies. This could make it difficult for the company to maintain its market share.

Overall, Sirca Paints is a good company with a strong track record of growth. However, there are some potential downsides to investing in the company, and investors should carefully consider these factors before making a decision.

Here are some additional risks to consider before investing in Sirca Paints:

-

Regulatory changes: The paint industry is subject to a number of regulations, and changes in these regulations could impact Sirca Paints’ business.

-

New product development: The paint industry is constantly evolving, and Sirca Paints needs to continue to develop new products in order to stay ahead of the competition.

-

Foreign exchange risk: Sirca Paints imports some of its raw materials, and changes in the foreign exchange rate could impact the company’s costs.

-

Expansion of the company’s manufacturing capacity: Sirca Paints is planning to expand its manufacturing capacity by 20% in the next two years. This will be done by adding new production lines at the company’s existing manufacturing facilities.

-

Investment in new product development: Sirca Paints is also planning to invest in new product development. This includes developing new products for the company’s existing segments, as well as entering new segments.

-

Expansion into new markets: Sirca Paints is also planning to expand into new markets, both domestically and internationally. This includes entering new countries and increasing the company’s presence in existing markets.

The total capex for these projects is estimated to be around INR 100 crores. The company plans to finance these projects through a combination of debt and equity.

Why the OPM of Asian Paints is higher than Sirca Paints?

There are a few reasons why the operating margin of Asian Paints is higher than Sirca Paints.

- Scale: Asian Paints is a much larger company than Sirca Paints. This means that Asian Paints has a larger economy of scale, which allows it to purchase raw materials at a lower cost. Asian Paints also has a larger distribution network, which allows it to reach more customers.

- Brand equity: Asian Paints is a more well-known brand than Sirca Paints. This means that Asian Paints can charge a premium for its products. Asian Paints also has a strong reputation for quality, which allows it to command a higher price.

- Product mix: Asian Paints has a wider product mix than Sirca Paints. This means that Asian Paints is able to generate more revenue from each customer. Asian Paints also has a stronger presence in the premium segment of the market, which allows it to generate higher margins.

In addition to these factors, it is also important to consider the cyclical nature of the paint industry. As mentioned earlier, demand for paint tends to fluctuate with the economy. This means that operating margins for paint companies can be volatile. However, Asian Paints has a track record of maintaining high operating margins, even during periods of economic downturn.

Region

Sirca Paints mainly operates in India, but it also exports its products to neighboring countries such as Nepal, Bangladesh, and Sri Lanka. The company has a strong presence in the Indian market, and it is one of the leading brands in the wood coatings and paints industry.

Sirca Paints is planning to expand its international operations in the coming years. The company is targeting countries in Southeast Asia, the Middle East, and Africa. The company believes that there is a growing demand for its products in these regions, and it is well-positioned to capitalize on this growth.

Here are some of the countries where Sirca Paints operates:

- India

- Nepal

- Bangladesh

- Sri Lanka

- Southeast Asia

- Middle East

- Africa

The company is also planning to enter new markets in the future. These markets include China, the United States, and Europe.