I made similar calculations for next 2 years. (Y)

Hi, I have invested in sintex plastic and average cost is Rs 90/ share. Is it advisable to add more shares at current level since the management seems to positive about business and showing interest in debt reduction.

1 Like

Think this forum is not for recommendation, but if I were you, I will wait to see Q2 results or maybe even Q3 to see if they can stabilise earnings at Rs. 1.05-1.10 per quarter before averaging more. Plus look out for cash generation updates in Q2.

1 Like

First thing on the investors’ mind imho should be the highly pledged promoter holding (73% pledged)

https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=540653&qtrid=98.00&Flag=New

When are they going to remove it?

Disc: not invested.

Interesting news from Europe. Bain and Apollo to buy-out RPC Plastics, one of Europe largest plastics company. Going by the below article, purchase price will be between GBP12.30 - GBP13.30. The company had an EBITDA of GBP600M which gives a acquisition multiple of 10.5x EV/EBITDA.

With a current EBITDA of about 250Cr for Sintex NP, the foreign sub val. comes to Rs. 2625Cr with current EV of 5500Cr implying a domestic EV/EBITDA of 5.25x (deep discount to peers).

Another way to look it is if they can sell to a PE player for 2600Cr + 710Cr of current cash + 300Cr from warrants + 300Cr from cash this year will reduce gross cash to zero.

With domestic EPS of about Rs.4.05 without any interest cost and PE of 20, price should at Rs. 80

3 Likes

As per the 2018 AR, the Sintex plastics division, which I assume makes the tanks, made a profit of just 3 Cr, while the Sintex NP division (Europe) made close to 100 Cr of profit.

The auto division, BAPL, made only 25 Cr profit though it’s 40% of net assets.

The prefab division, which the co is trying to reduce, made bulk of the India related profit of 45 Cr.

In all, the 3 India based businesses which comprise 86% of net assets, together made a profit of just under 75 Cr. The Europe business with less than 15% of assets made 100 Cr of profit.

Thought it’s interesting that the management is trying to reduce the business which is making the most profit for them, at least in India.

Disc: Invested, planning to average at current prices

1 Like

Prefab division looks the most profitable on paper. If you talk in terms of cash flows, prefab division has issues like not getting paid on-time by the government agencies and need for huge working capital.

Another weak quarter it seems like. I am heavily invested in the stock and am starting to feel that these guys are only about ‘stories’ - every quarter there is some story about why the nos are not good. This time it seems to be around some “reorganizing of product portfolio”.

Anyway, I dont see the EPS hitting 3.6 this year. Half year is around 1.2 and 3.6 is a TALL order.

Hope to be proved wrong on this one

2 Likes

A couple of years back even I was heavily invested after Modi was elected. I got sick of their stories and excuses quarter after quarter.

Finally I gave up and booked heavy losses. I have not regretted my decision till date.

Pl take your own call.

2 Likes

Problem is not the operations, but the interest cost. Interest instead of declining has increased to 89Cr from 74Cr. That itself is approx. 40paisa pre-tax impact when cost should have declined.

Any number of questions on how the interest cost is raising despite lower cost KKR debt has met with opaque answers.

Anyway, I am unable to judge the operations as there are not enough metrics to see / evaluate.

They have a leathal combination of poor transperancy and inability to meet guidance - and I am less hopeful than ever. Maybe time to change ship in this market, when there is atleast the option to recover lost capital is more !

2 Likes

Yes, my average cost is 60 and was a bit worried few months back when it started tanking. But now with every stock down 50%, think will transfer to another stock. Making back the money should not be difficult in this market.

Any thoughts of where way you are going. I am thinking EPC companies or maybe YesBank.

Am hunting for value in Capacite Infra - EV EBITDA of 5 (so yes EPC) and no debt. Ahluwalia contracts is another bet.

Some NBFCs are attractive like hell, but who knows how long the wait there is

Maybe we take this conversation offline, incase you have any other ideas to discuss or have feedback on the above, may not be relevant for others in this forum !

Borrowing more or less around same levels with Cash & Cash Eq. going down by 230 cr. Where has the cash gone?

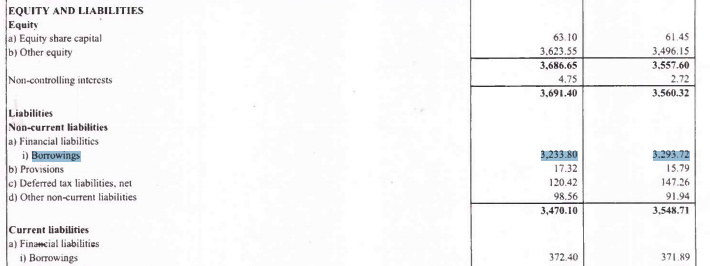

Quarter after quarter some stories but NO PROGRESS ON DELEVERAGING!!!

Oil prices, $ value, delayed payments from govt orders all not in their control BUT what explains not deleveraging (which is 100% in their control)?

Anybody going on the call today might want to raise it - unfortunately I wont be able to ![]()

2 Likes

Company in the conference call told that they have paid 200 cr debt. However due to rupee depreciation the debt looks elevated. Given the way the company and mgmt has guided earlier I am not sure if we can trust the current explanation.

Coming back to my running commentary on Sintex. Still hold at 60Rs.

-

Why has the company not hit Re.1 EPS which should be normal earnings. ONE REASON. Interest cost. Interest cost went up by 13Cr which is Re.0.2 impact to earnings (0% tax assumed)

-

By my calculation interest actually should have been at 70Cr or in earnings terms Rs.0.3 impact to earnings which would have given you Re.1 earnings.

-

Reason for interest cost at this level.

- Company said 9Cr impact was from forex translation which makes sense.

- Due to working capital they could not reduce debt much (Rs200 cr stuck overdue)

-

Company reduced debt by 288Cr but gross debt looks same as 1400Cr is dollar denominated, which again makes sense. Whether you believe the management or not is another question.

-

Growth is slack but I was not baking in any growth this year. With all the changes, difficult for any company to turn around in 2-3 quarters.

Disc - Was thinking of selling it but after call think will hold on for another quarter. Guess Monday will be in red.

3 Likes

Adding more from the Q2-FY19 conf call:

-

Less margins due to:

i) High crude oil prices impacted - raw material and transportation costs

ii) Weak Rupee against Dollar increased the interest cost -

Pledged shares details:

- Debt taken from the NBFCs and the shares are pledged to them.

- The Warrants will continue to be converted at Rs. 90 per share.

-

Future Guidance: Hope to increase the revenue by 3X in next 6 years, reasons given:

i) A large range of water tanks will contribute lots of revenue

ii) The urea tanks for diesel vehicles, reservoir tanks will start contributing in revenue from Sep 2019.

iii) Mass transit (Metro train) products will start contributing in revenue from 2022. -

The prodcution/revenue of some of the products kept down (in control) to avoid the high cost and less margins due to high crude oil prices, it was a concious decision henec less revenues in Q2. Also pre-fab revenue declined which is as per plan.

-

Total capex of H1 was 117 Cr only (India capex = 24 Cr, Foreign capex = 93 Cr), which seems very much under control.

Disclaimer: Invested, hence views may be biased. Its not a buy/sell recommendation.

4 Likes

the management has been saying for the past 1 year tht thy r bringing down the gov aka prefab revenue wch has infact transpired but though the sales in prefab r down by 600/700crs thr hasnt been a reduction in working capital loans nor has thr been a reudction in long term loans evn though promoters gv infused 350cr worth of capital via warrant conversion

IIFL has given a positive view on SPTL…

Sintex Plastics, a leading player in composite plastics space, is a re-rating candidate owing to better cash flows from shift in business focus and promoter infusion leading to deleveraging; valuing at 8x FY21E EPS.

2 Likes

Today management has issued a notice that they are doing everything possible to deleverage the company in the interest of shareholders, this is probably being done to address the recent stock crash from 25 to 18…But can someone tell me why the leverage doesnt appear on the balance sheet . Is it due to “fccb” as already discussed above on the thread? I am referring moneycontrol march 2018 data…