Hi there ! Can anyone

comment on the Interest cost ? I couldn’t find details about total debt outstanding and rate of interest on it.

Also, I see that no single client is contributing more than 5% of sales in CM business which is good. For the Q1 numbers the share price seems to be justified. Any positive surprise in coming quarters will help re-rating of the stock and to me it looks like it will take atleast a year to reach previous valuations (5K crore M.Cap). Please comment if there is any flaw in my understanding.

I had taken a small trading position getting attracted by the Demerger story and reading various articles by research houses. Also, not to mention the great old Sintex tanki brand. Somehow got so ttracted to demerger value generation story and the leading brand that forgot the basics of Management quality. Although, did not go into much depth but the moment came to know about numerous equity dilution and management not walking the talks, I exited with 40% loss. Happy with my loss now as getting huge relief after the not so timely exit but getting rid of not so good Management stock name from my portfolio

The only positive I can make from the result is the fact that it promoters appear to be taking steps to create value. From my view, the fact that they have converted their warrants into shares shows that they have confidence in the business going forward. We may see increase in profits to the extent loan is repaid. Secondly, by employing Big 4 as auditors, the company is indicating that there is nothing wrong in the books of the company.

While obviously the results seem below par, but given the above, at lease you get a sense that may be it can turn around. What actually happens is something that only time can tell.

Sharing some notes I took from the earnings concall today. Please verify with the transcripts once they are available as interpretation errors are possible.

Guidance:

EPS guidance for FY19 & FY20 is 3.5 & 6.5 per share respectively (before dilution). Q1 EPS is 0.6 & FY18 EPS was 2.37/2.33 before & after dilution

FY19 EBITDA margin guidance is 16.5% for the full year (Q1 13%), estimated EBITDA of around 762 crs

Top-line growth forecast is around 20% for the next 2 years. Q1 YoY top-line growth for Custom Moulding business excluding excise is around 20%

Net debt as on date is around 3164crs, this expected to come down by 300/400 crs to around 2800 crs by end of the year

Free Cash Flow estimates are around 550 crs & 700 crs for FY19 & FY20 respectively

FY19 depreciation is around 210/220 crs estimated

FY19 finance cost estimate is around 275/280 crs

Net Debt / EBITDA target is 2.3 by 2020

Contribution of prefab business is expected to be around 800/900 Rs for the full year. May come down by another 100 crs in FY20 – but no significant decline expected. EBITDA contribution will be 90/110 crs

Additional commentary

Despite the negativity surrounding the stock and continuous decline in share price, management is of the view that street is failing to recognize the significant improvement in the earnings quality. Expenses which technically qualify as capex are being recognized as opex in PNL. Consequently, while the growth in profits are muted, the capex figures have significantly gone down, to around 21 crs only for Q1Fy19

Distribution & organization structure revamped, with separate CEOs for Retail & Institutional business. New distribution model introduced in 2 regions (North & East?) for 2 products – tanks & doors, & the initial results appear to be promising. Deployment across all regions expected to be complete by this year

Q4 should see a significant jump in earnings (historically this has been the best quarter for the business)

New product in auto space – Urea Tank for BS-VI diesel vehicles. 3-4 players in India, one being manufacturer & rest importing from China & S. Korea. STPL expects additional revenue opportunity of 350/400 crs from this segment, with peak demand coming from September, 2019

Utilization is around 65-70% - no immediate capex requirement

Guidance is very good. 3.5 Rs EPS for FY19 and Rs 7 for FY20 and FCF of 500 and 700 for FY19 and FY20.

Also company is reducing debt at a good pace. Last year closing net debt was 3628cr. Currently it stands at 3144cr. Target for FY19 is to reduce it to 2800cr.

Management is very bullish on custom moulding segment and expecting minimum 20% growth. They are slowly trying to get the capital out of prefab.

If management walks the talk and reduces debt as planned, stock will gradually get re-rated.

Generating huge free cash. With FCF 500, and 20% growth as management guided, company can reach a market cap of 15,000cr. But even with conservative growth, it can reach at least 10,000cr.

All depends on how well they reduce debt, release pledged shares, show growth as projected.

Also a company that expends its expenditure rather than capitalizing them will look less profitable initially, but will show more profit in the later years since the balance sheet will be light and less depreciation in the subsequent years. It would’ve been nice if the management said how much they expended instead of capitalizing.

Check the below link , the highlighted section from their conf call. I feel this management does not follow their words . For instance they said retail will grow 40 % in last conf call now they says more than 20% .

Dis: invested and now think i made a mistake , was blinded by the future prospect of the company . Should have checked more about management credibility .

Did you prepare this MoM yourself? Very detailed…thanks for sharing.

I haven’t followed the past concalls very closely - 40% growth for next 10 years is anyway laughable. My personal view is that some of the statements in the call were less explicit than I would have personally liked - for e.g. they indicated that the prefab business will shrink further by close to 50% from FY18 levels by Fy20, bulk of it being this year.

That said, if CM grows by 20% and margins expand by 16.5% as guided, stated EPS figures are likely to be achieved. But - what are the chances?

In Q1, CM grew by 21%, with the new distribution model deployed in 2 regions. With rest of the regions adopting the new model, lets hope at least they are able to sustain the current growth rates.

Margins though fell to around 13% in Q1, due to I think high employee cost (not likely to change) and possibly also due to certain additional expenses (technical capex type items) getting recognized in operations. Not very clear how such significant margin expansion will happen (perhaps some of these expenses will go away in coming quarters?). This can be a potential risk, unless CM growth exceeds guidance.

Company is going through a major transformation, and sometimes, changes take bit more time to take effect. Perhaps, that is why clear communication is so desired.

In any case, given where the share price is today, I anyway have no choice but to wait.

If I look at it another way - assuming their guidance is met, which management was extremely confident of achieving, stock is trading at around 5x FY20E earnings. And there is no denying they have a strong brand.

Last point to note: Promoters converting warrants at near 3x market price

76cr finance costs in Q1. 67cr last year. Despite debt restructuring and reduction in debt.

Management gave explanation for that in the concall, but that was not satisfactory, and the person who asked the question didn’t continue on that topic.

Explanation by management:

76cr is not interest outflow. It’s accrual. Outflow is lesser by 15cr.

Avg interest cost for the money lent by KKR is 8.75%. Avg outflow QoQ is 3% less than that, which will be paid at the end of 3 yrs.

My comment:

Interest outflow may be 61cr (76cr - 15cr), but the 15 cr which was not paid is still credited to the interest payable account and is lying in the liabilities section of Balance Sheet, which they will HAVE TO PAY one day (here they said in 3 yrs).

So, the company’s cash position is good, but the Balance sheet is bit heavier.

So, the finance costs of 67cr last year and 76cr in Q1FY19 are comparable (despite how much cash goes out)

But the management tried to project in the concall that the interest expense is lesser by 15cr (which actually is not). So, this is definitely an increase in finance costs.

Guidance for reduction in interest costs in Q4 con call: “Reduction of 75cr annually”. This equates to 18.75cr per quarter. Logically, finance costs should be in the range of 55 to 60cr per quarter, which is apparently not the case.

Guidance for finance costs in Q1 concall was 280cr per year. That is 70cr per quarter, which contradicts what they said in Q4 concall (55 to 60cr).

Finance cost of SPTL has always been a mystery. Next few quarters should show the trend.

This has been the trend so far. It’s been in the range of 70 to 75cr per quarter (exception was Mar '18 quarter where it spiked to 85).

My kitchen sink EPS of Rs. 4 looks good. Company has guided 3.6 EPS this year which would mean 3 Rupees for next three quarters. My guess this quarter had one-time items which sank the CM EBITDA margins to 12%.

This year I expected higher EPS at 4.35. Where did I go wrong? Interest cost. Though the company touts net debt, the gross debt number has not gone down from 3800cr odd. The company cited maturity cycles for the gross debt o/s.

So how do we see going forward. I assume that by next year 1400cr gross debt will be repaid. (700cr - from current cash, 250cr - 2018 cash generation and 450cr - promoter warrants). This will bring down gross debt to 2400cr so save about 126cr of interest (assume 9% costs) or Re. 1.43 in EPS (25% tax)

Allowing for a 10% rise in EPS from the kitchen sink of Rs. 4 EPS, I get about Rs. 5.5 EPS for 2019-2020 making the stock currently valued at 7.25x.

When does the stock react? Everything in the markets is narrative. They have to show one quarter at Rs. 1 EPS and normalized EBITDA margins. That would do the trick. I still feel Europe business should be sold off.

Took that into account. Felt lazy to show entire waterfall to Rs. 5.5.

So this year, guidance is Rs. 3.6 - EPS with about 62.4 diluted shares which they should manage. I think they are not assuming any tax going by last two quarter.

But I have taken the normalised “kitchen sink EPS” of Rs. 4, so that makes normalised PAT = 250cr. Add interest of 280cr to get EBIT of 530cr. Grow that by 10%, you get 583cr. Deduct 150cr of interest. I tax at 15% next year as effective tax from zero this year. Fully diluted shares I take as 66cr shares. Gives you 5.5 give or take.

Two things, one I am assuming debt starts getting paid early next year as warrants expire by March I think. If they delay repayment then interest cost will be higher.

Second, taxes are higher than 15%.

Interestingly, the management guidance is at 6.5 which if you use my numbers and apply no tax you will get. Once the AR is out I can go through and figure out the DT treatment.

Promoters infuse about 110 Crores in the company by converting their warrants into Equity Shares (@ 90/share). Very positive development, which reinforces some belief in promoters walking their talk. Hopefully this is accompanied by improvement in operational performance going ahead.

Promoter converting their warrants at premium still dilutes the earnings of the company. Isnt it not bad for the shareholders especially the minority holders?

We could presume that the promoter is showing FAITH in the future performance of the company though.

Dilutes the earnings yes, but given the price and number of shares, the same will be marginal. The benefit, however, of 110 Crores would be immense operationally and would help in building investor confidence.

Cash flow from operations after WC adj. was at 781Cr. Assuming similar amount this year and CAPEX of 160Cr + Interest of 250Cr, company should be have about 350Cr for debt repayment.

With 710Cr of cash and another 300Cr from warrants over this year, company can bring down gross debt from 3800Cr to 2500Cr by March 2019

They have security deposits of another 301Cr in the Prefab business. If they can get some back + some assets sales, further reduction is debt is possible

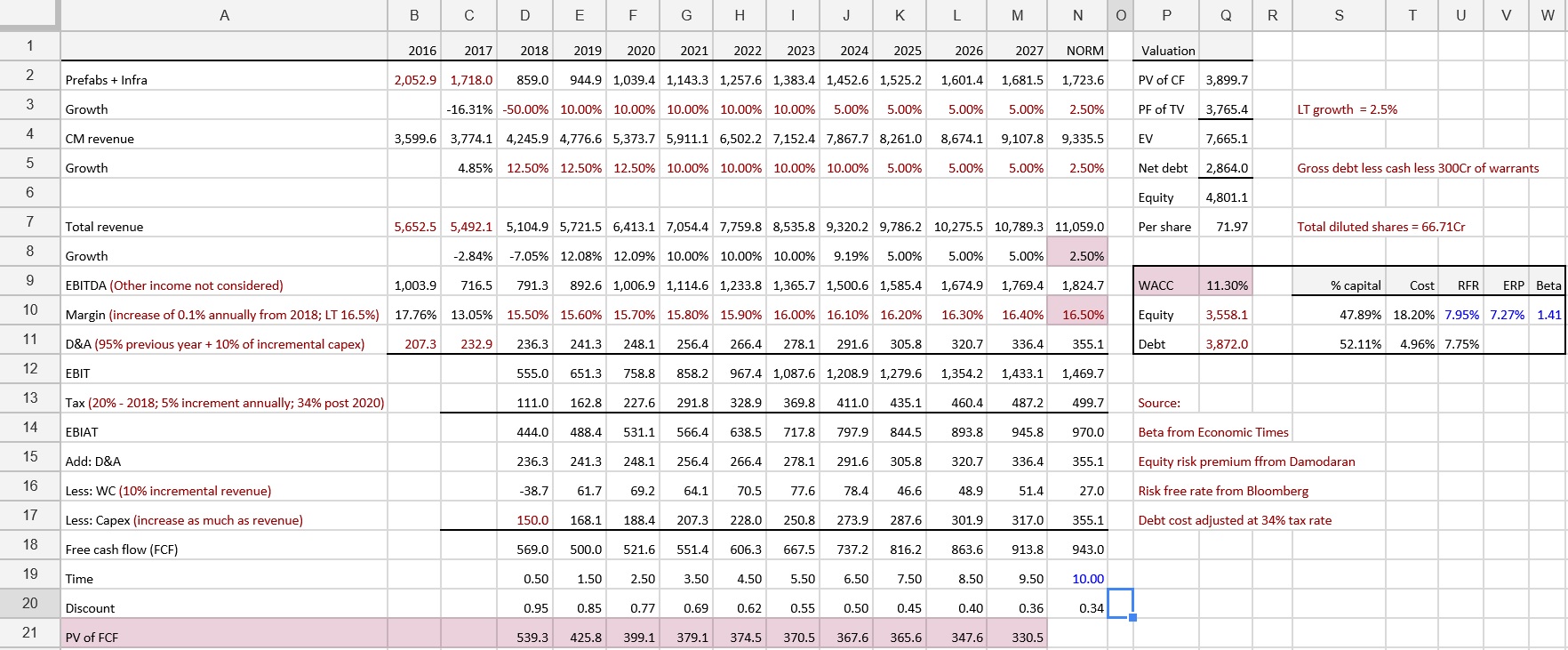

Will add a model later possible next two years. At 10x PE, stock looks appealing.

Built a simple DCF for Sintex. Very conservative assumptions. Model self explanatory. If they can just about manage the ship (not even heady growth rates, this should double).