It catched my attention when i saw its trading very cheap compared to peers

PE :

Sintex Plastic = 12.

Nilkamal Ltd = 22.

Astral Poly Technik Ltd = 81.

Supreme Industries Ltd = 42.

Finolex Industries Ltd = 22.

Jain Irrigation Systems Ltd = 30.

I came across this presentation, which looks pretty compelling.

http://www.sintex-plastics.com/wp-content/uploads/2017/08/SPTL_INVESTORS_MEET.pdf

Their product portfolio and Client base looks very impressive.

I would just like to know whats the reason its trading cheap compared to other Platic Companeis ?

Is there some Management History ? or is it the debt ?

If anyone is tracking would really like know your views

Thanks You…

Some of the highlights from Annual Report -

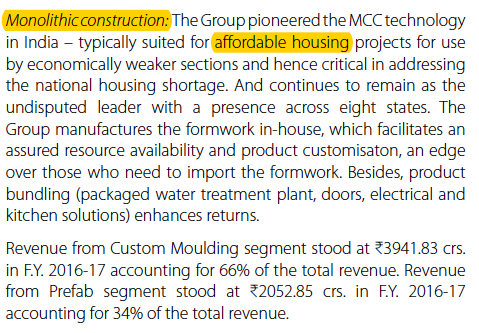

The Company has two business operations – custom moulding (under its subsidiary Sintex-BAPL Ltd.) and EPC contracts for various infrastructure projects (under its subsidiary Sintex Prefab and Infra Ltd.).

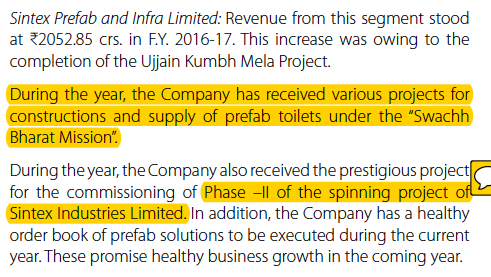

→ Out of Rs 6,000 odd Cr Revenue , Rs 2052.85 Cr was from Prefab and Infra Ltd .

→ The Size of PreFab Toilets order is not known ?

→ Have to see how this Cross selling is done to Sintex Industries Ltd ?

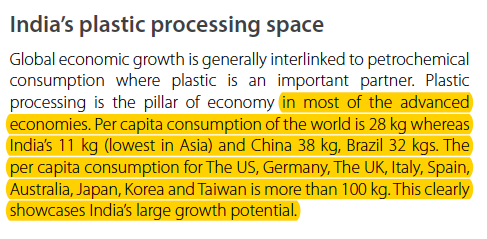

Some General Knowledge Stuff

→ This is really interesting statistic - Much lower for some reason compared to EMs like Brazil and China as well.

→ GST - Case for Unorganized to Organized If plays out there is some easy market share to gain.

Products of the company

Custom moulding – domestic operations → It Includes

Water Tanks , power distribution, automobiles, electrical products, sanitation,

building interiors, warehousing and a host of other verticals.

→ Majority of Orders from Government may be thats why they never made enough money for shareholders considering past corrupt history of Gov of India (My personal View). Things might change or may not lets see.

→ Below seems like a good business, Its growth is important for margins to expand.

→ This seems interesting, Seems like are they are not talking numbers about Septic tank it might be very low and could increase in future or not has to be seen.

Some interesting Innovation :

In addition, the Group has created a retail business plan for small sewage treatment plants catering to individual houses, residential bungalows and propagated awareness of the product and its effectiveness by participating in seminars and by organising contractor work-shops. For retail usage the Group has created customised variants in which the treated water can be used for gardening, toilet flushing, floor washing, cooling tower and in construction activities. The Group has created a dedicated cell comprising consisting of service managers, technicians for aftersales services (including AMCs) to ensure the product performs upto client expectations.

→ Hard to predict how much this will come into revenue but good to see they are trying new things.

→ In Fy 15-16 they got approval for this too -

→ India needs lots many more dustbins than it has ![]()

→ Business from Electricity Boards: This segment is the key revenue generator accounting

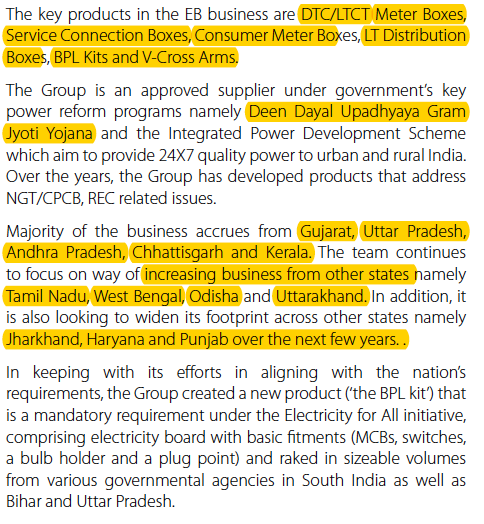

for more than 70% of the revenue for SMC business.

→ This Should do well considering election in Fy19, Government Expenditure in this area will go up -

→ Also lots of growth prospect by tapping markets into new states with GST in place as well should help in this regard.

→ Growth Plan :

→ If chemical industry will continue to do well then this should do well as well :

→ Ohh Man too many Government Orders

→ Bus yehi government scheme bachi hui thi

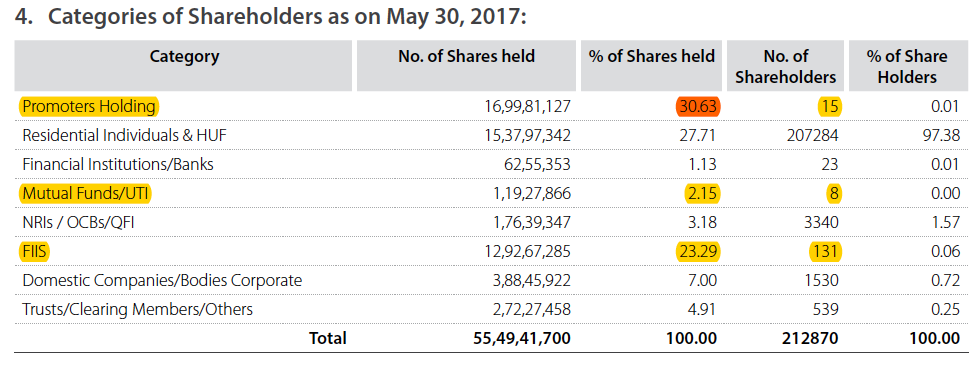

Promoters Holding Is Low - That too held by 15 members

→ This is like another Rs 500 Cr worth of shares

This will take the Debt down but will dilute the Equity Base , Not sure if this has happened already (Need to check latest data)

Financials

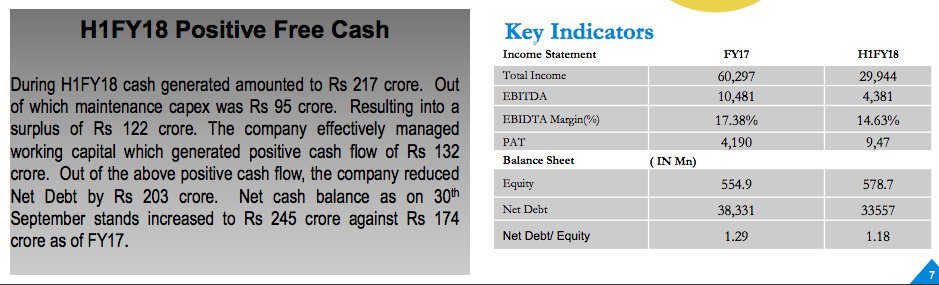

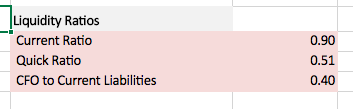

Ideally should be > 1 .

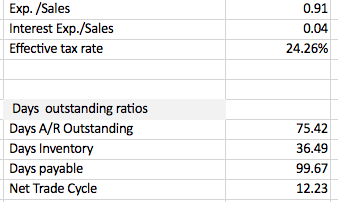

Here you can see the liquidity Problem and High Working capital nature of the business.

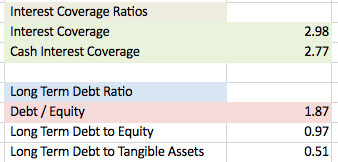

The Interest coverage ratio seems good and long term debt ratios seems okay.

Ideally would like to see Debt/ Equity going down.

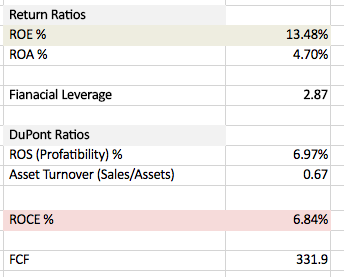

ROE looks optically high because of high financial leverage in the balance sheet, Which (high leverage) is very evident from the pathetic ROCE.

Good news is atleast company generating some “Free Cash” which can be used to re pay debt in future. I think most of the CAPEX is done So , far no mention of CAPEX in Annual Report.

Also, Would like to see Margin (ROS) improvement in future earnings.

Source to my Sheet -

They have invested 50 Cr in Zillion Infraprojects

Not much info as its private company, CEO of the company doesn’t look Shady atleast Ex L&T guy

https://www.linkedin.com/in/c-s-saxena-61695526/

‘Zillion Infraprojects Pvt. Ltd.’ is an Industrial Construction company and was earlier known as ‘Durha Constructions Pvt. Ltd.’. I started this company more than 35 years back as a subcontractor to L&T. Now from a mere staff strength of 4 people, we have grown to a company with 1,200 permanent employees and more than 8,000 workers with projects spread across India.

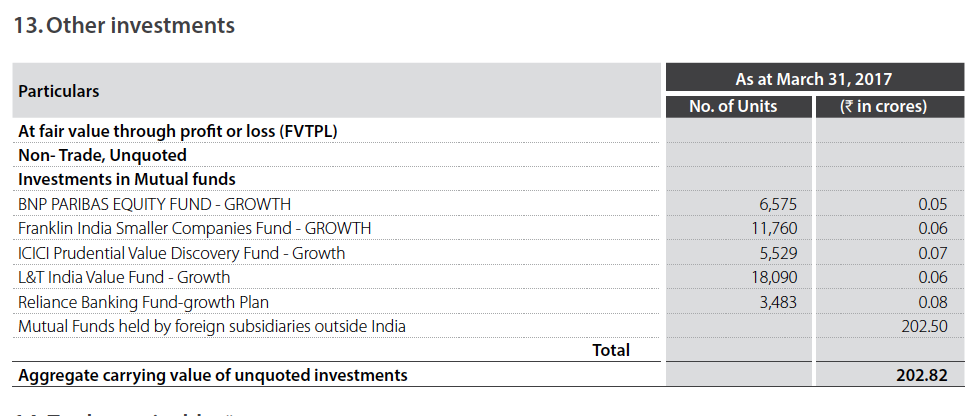

Other 202 Cr generated by Foreign subsidies invested in Foreign MFs .

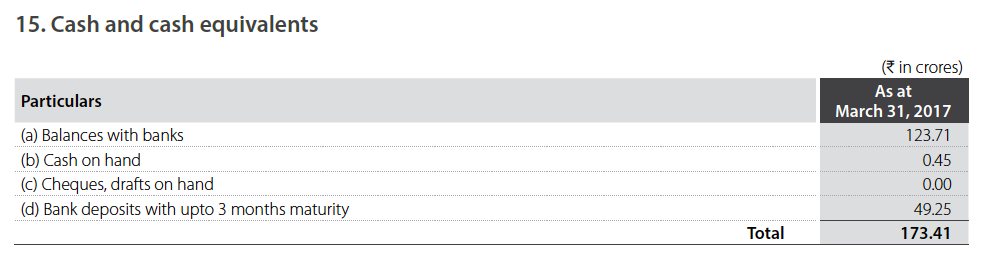

Cash in Hand

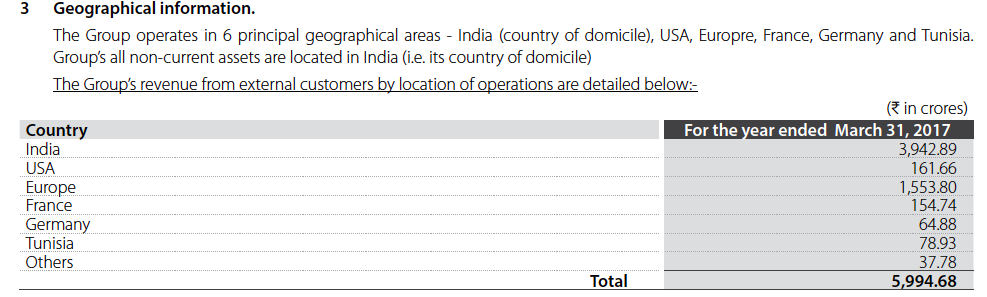

Geographical Revenue Split -

The Risk / Things to watch out -

Debt overhang - No new CAPEX, So going forward Debt should go down.

Management Focus - Should increase as its now separate entity compared to past.

Demand - As they do lots of Government projects , it’s a good proxy play to Government spending, Hope is Government would be going to spending more considering elections are on FY19.

Disc: Invested.