Thanks for your reply Aniket. I am just trying to get the worst case scenario… and I find comfort in that valuation as well. Couldn’t agree more with your statement that there is sufficient margin of safety for patient investor. BTW, your industry post is really good!

That is fine Kunal, but the main thing is ‘demand’… Capacity can be utilized only if they manage to get demand, atleast know what management thinks about it. That is where Ayush Mittal can help as he attended SME meeting.

Is there any study that shows the impact of EV on this industry?

Request if some1 can post the impact of BS-VI norms for auto component makers. Kunal - more specifically looking for BS-VI norms in relation to PM makers (does it has any anything to increase market share)…?

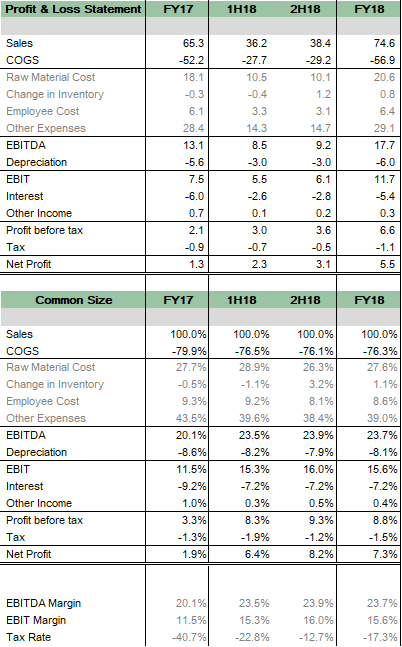

Rs5.4cr profit for the whole year as compared to Rs1.2Cr last year on sale of Rs74Cr as compared to Rs65Cr. PE ratio is around 40. My reason for investment is the moat company has in relation to sintering technology and therefore the high valuation is not a concern.

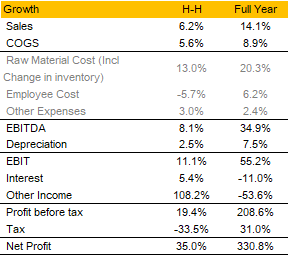

Topline growth has come 14.1% in FY18 because of volume growth.

EBITDA margin has improved to 23.7% vs. 20.7% (2H18 - 23.9%) due to reduction in employee cost and other expenses as a % of sales (See common size P/L).

Bottomline has grown significantly because of an one-off expense (1.84crs) that company had incurred in FY17. Adjusting for that Net profit has grown 75% largely due to EBITDA expansion.

Tax Rate: Tax rate is low currently around 17-18% which might be due to accumulated losses that it might have. This should inch up gradually from here to 22-25%

Balance Sheet:

Working Capital:

Inventory days has declined by 6days to 63 days.

Debtors and Creditor days both have gone up by 20-25 days

Debt:

Total Debt has gone done from 38.5crs to 28.7crs. As a result interest cost has also decline.

Interest cost is expected to decline further to ~3crs from current 5.4crs (assuming 10% interest cost, management has indicated arnd 9.5%) which should further improve the profitability.

I am having a call with the CFO later in the day. Please send in any question that you may have.

Please ask for the breakdown between sintering and old business, margins achieved in each, Any new client or products added during the send half and what is the outlook and target for next year in terms of sales growth and profitability.

I had a call with the company for updates regarding results. These are the Q&A:

Volume sold during the Year?

1550 tons

EBITDA margin:

We ended 2H with margin of 23.9% and this is expected to move up as we increase our volume.

What would be the effective interest cost next year? Rate and absolute amount

Effective interest rate would be 9.75-10% for next year. Our current debt is ~24crs ( would increase by 3-4crs when we import the machinery. Currently this is shown in the balance sheet. Debt as per B/S is 28crs)

What’s included in the other expenses item? It is around 38-39% as a % of sales?

Other expenses includes Power (3-4crs), Outside job work (10crs), freight (2crs) and other smaller expenses

I assume tax rate is low because of accumulated losses of previous years. How much is left for the set off?

Yes it is because of accumulated losses and MAT. It can continue for another 2 years and post that tax rate should inch upto 23-25%

Debt at the end of the year

We would be paying debt of ~5-6crs by end of FY19. We generate OCF of 10-11crs and this would be used to pay off the debt every year till be achieve best possible capital structure

Business Development

How much volume growth do you expect next year

He refrained from giving any forward looking guidance. However, qualitatively he said, should improve margins by 1-1.5% and topline should witness a healthy growth

What about average realisation? Is it expected to move up?

Average realisation for the year came at arnd INR 530-540/kg. As per the talks it has gone up from last year. (Need to check volume sold last year and this year in conjunction to topline growth for the year)

Working Capital Cycle?

it is expected to stay in the range of 80-90days

Company did not specifically gave any guidance and details of new client. It said, client addition is an on-going process and we keep adding clients as and when the testing converts into first stage of production. Current monthly revenue run-rate is 7.5-8crs.

Hi Kunal, nice compilation. Thanks for the update. Have you noticed any increase in receivables. I felt payable also increased. Anyway thanks for the input.

Sorry forgot to update. Yes receivable and payable days are high because some payment was deferred due to long bank holidays in the last week of March.

CFO confirmed they have received dues of 2-3crs in the first week of April.

Working capital days will continue to be around 80-90days for the full year.

Just want to share my phone discussion with Mr Pankaj CFO of Sintercom while it is still fresh in my head. I just got off the phone. Thank you Peter Lynch! Just read in one up on wall st yesterday to contact management and had an excellent success today.

First, I really appreciate their effort to talk to a Retail shareholder with minimal shareholding and that too within a day of emailing my queries. Very impressed with their CG standards. Some of these may have already been discussed above.

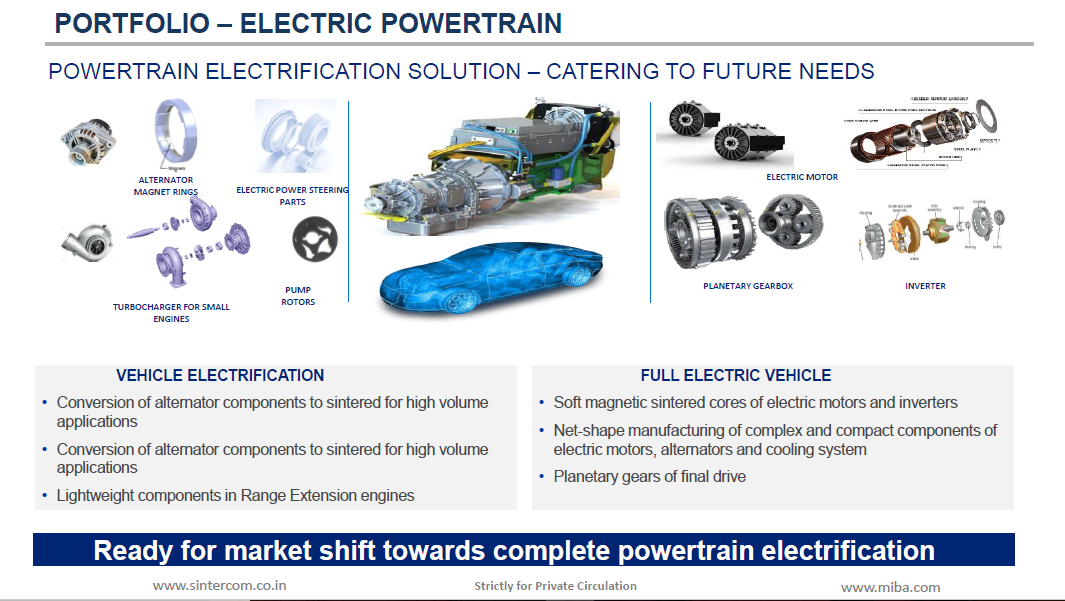

Current market size of sintered components is about Rs1,300cr of which Sintercom has 6% market share. GNL? and Sundaram fasteners have much bigger market share because they are providing all OEM products some of these have low margins. Sintercom provides only high margin products. Hitachi (I think) has also entered India but they are mainly supplying to Hyundai.

USA has about 17kg sintered products per vehicle, EU, Japan have 12KGs. It is currently 4.5KGs in India. So there is capacity for improvement in market share.

Sintercom has both its own products and products developed with tech from MIBA (35% of products). For MIBA’s technology, Sintercom pays an upfront fees and 3% revenue as royalty for 5 years. After 5 years they are free to use the product without royalty.

MIBA has a non-compete arrangement with Sintercom in India for Sintercom’s customers and Sintercom cannot compete with MIBA customers outside India.

MIBA has no plan to increase or decrease its shareholding and is looking to operate in India with the current arrangement.

MIBA has other product lines other than Sintered components like bearings which Sintercom is not interested in as there are no markets in India.

No immediate plans but Chairman wants to diversify to commercial vehicles and medical components.

Current capex of Rs 17crs is almost ready. Capacity is 3600 tons. No further plans of capex until 2021. Plans to increase capacity to 4900 tonnes after 2021.

Did not give a direct revenue guidance. But realisation per kg is Rs500 and the capacity utilization is gradually expected to increase from 66% in Mar18 to 90+%.

Company fully exited other businesses and is only into sintering. So NPM of Mar 2018 is maintainable and we can expect marginal improvements from here.

Top 4 clients make up 90% of the revenue with Maruti making up 48% and Mahindra making up 28%.

It takes at least 1.5 years for the customer to accept a new product from Sintercom doing R&D to client testing and accepting the product.

New emission control norms to be implemented by 2020 could provide additional opportunity as it will require both improvement in fuel efficiency and noise control. Sintered components are 10% lighter and also less noisy providing an advantage here.

Working capital days is high at 180 days as the company is the exclusive component provider for certain model without which the whole production will stop. Therefore always carry stock of raw materials and finished products. Can improve to 165 days but not much is improvement is expected here.

Fixed asset turnover is less than 1 because the FA includes 5 acre land and buildings only half of which is being utilized now. Adjusting for this it improves to 1.3 which still looks low to me.

I think the turnover can go up to Rs150 cr by 2021 and they will need new capex to increase turnover further. With current margins. Net profit can double to 12crs in 3 years which gives a 3 years forward PE of 15. Low FA turnover, high working capital days, probably ROCE would suffer here. On top, the company is in cyclical auto industry with high client concentration and servicing B2B. Not much going for this company other than exclusive technology partnership. Management capability of the company remains to be seen. Probably a high risk bet which is definitely overpriced at the current level.