Sintercom India Ltd

Market Cap @ 65/- ~156crs

Revenue 1H18: 36.3crs / FY17 – 66crs

Margins: ~24%

Why to read more about Sintercom

- One of the three company in India making Sintered products (Auto component) alongside GKN (a MNC), Sundram Fastener.

- An associate of global market leader ‘Miba’ in Sintered products

- Strong board/management composition

- Strong margin profile for a 66crs revenue company.

- Growing and untapped market

Company Background:

Sintercom India Ltd. is one of the leading automotive sintered components manufacturer located in Pune, India. It specialises in manufacturing medium to high density sintered components for automotive engine, powertrain and exhaust systems as well as sensor components for global customers. Company was started by Mr. Jignesh Raval in 2007 as Maxtech India Pvt. Ltd. Mr. Raval is a technocrat with over 20years of experience in Automotive industry. Prior to starting Sintercom, he was working with Tenneco Inc as ED, Global Supply Chain Management division.

Timeline:

2007 – Started as Maxtech India Pvt. Ltd

2010 – Started manufacturing Stainless Steel Hego Boss (converted forged parts to Sintered products)

2011 – Entered into a JV with MIBA Sinter Austria (converted Forged Gears to Sintered Gears)

2012 – Changed company name to Sintercom India Pvt. Ltd (kept introducing new products)

2013 – Started supplying to Maruti Suzuki

2015 – Developed 6-speed transmissions Syncro Hubs

2016 – Developed a product for Bajaj Auto (Forged shift tower component to sintered)

Board of Directors

Mr. Hari Nair – Chairman, ex-COO, Tenneco, 20yrs experience

Mr. Jignesh Raval – MD, CEO

Mr. Markus Hofer – CFO, Miba AG

Mr. Harald Nuubert – CEO, Miba Sinter Group

Management Team

Mr. Jignesh Raval – MD, CEO

Mr. Pankaj Bhatawadekar – CFO

Mr. Nikhil Chavan – Head, Engineering and Marketing

Mr. Sachin Gunjal – Head, Manufacturing

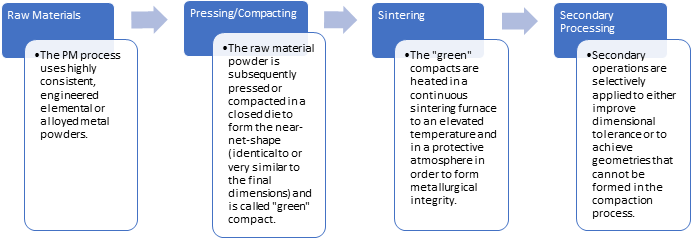

What is Sintering Technology

Sintering is a process that uses metal powder to make components. Sintered products are highly tensile and density higher than normal casting and foundary products. Please go through the video here to understand more about the process. (Sintering process)

Sintering is a green technology as it uses metals scrap and uses less water and energy compared to Casting and foundaries.

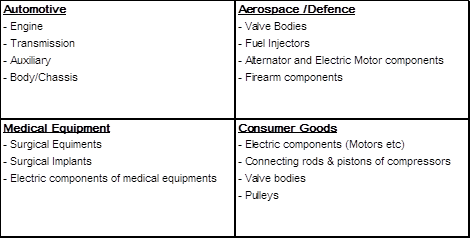

Usage

Market Sizing

Currently market size of Sintered products in automotive segment is pegged at ~950crs. Share of sintered products in PV is ~4kg/Passenger vehicle, however in the US this comes to 17kgs and in EU and Japan, this is around 12kgs. If management is to be believed, this could go up to 7kgs over next 5 years.

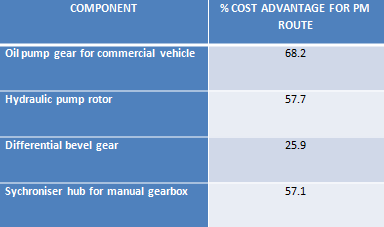

Since sintered products are lighter than casting/forging products, hence they are more and more preferred by the OEMs to reduce the weight of the vehicle which helps in increasing efficiency of the vehicle.

If Auto analysts are to be believed then 2W market is expected to increase by 12% per annum to reach 23-24m while PV is expected to go up to 5m over next 2-3 years. Also as BS VI will roll out in 2020-21, usage of sintered products is expected to go up by another 1-1.5kg/PV.

With rough calculation, we can arrive at the market size of ~1500-2000crs over next few years. That roughly doubles the market in next few years.

Sintercom currently has market share of ~6.5% which it expects to increase it to ~10% by 2020-21

Key Customers

Sintercom has long standing relationship with major players in India like Mahindra’s, Bajaj, Maruti, Honda and others. It is also exporting a small portion to Suzuki for products in Japan. Pic below shows how many models of which OEM uses Sintercom products.

Financials & Other operating metrics

4-yr Revenue CAGR – 10.7%

4-yr Sintered Products revenue CAGR – 18.5%

4-yr EBITDA CAGR – 15.2%

4-yr PAT CAGR – 104% (On a low base)

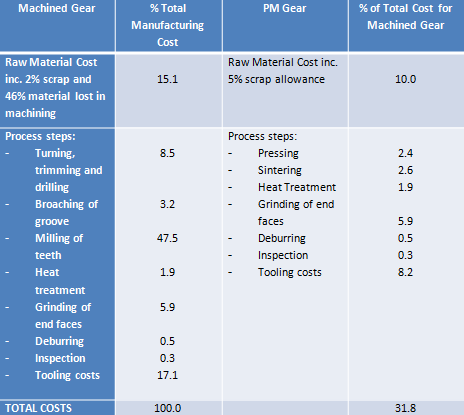

EBITDA margin has improved from 17-18% to 24% in 1H18. This is largely because of discontinuation of sale of Hego Boss (non-sintered product) which was a low margin business. Management had consciously taken this decision to reduce sale of hego boss and as of 1H18 it has been discontinued. Sintered products have higher margins and every new product introduced will improve the margins further.

RoCE has increased from 11% in 2013 to 14% in 2017 & 18% in 1H18.

Cash Flows: Company is generating ~10-11crs of operating cash flow and uses it to reduce debt.

Asset turnover is ~ 1.5x and operates at 70-75% capacity. They use rest of the capacity for R&D purposes to bring new prototypes.

Object of the IPO:

Company would be raising ~INR 56.5crs (incl anchor/Preferential allotment).

Total amount Raised – 56.5

Exiting Shareholder – (23.0)

Capex - (16.56)

Debt Repayment - (11.5)

W/C requirement - (3.0)

Remaining for general corporate purposes

Sintercom would be spending ~16.5crs on capacity expansion which would increase its capacity from 1800 tons to ~3800tons (need to confirm this number). Also at the present facility they can increase the capacity to 8000tons by just installing machineries.

Current debt is 35crs out of which they would retire 5crs from operating cash flow and reduce it further by 11.5crs from IPO proceeds. Portion of debt that they are retiring is a high interest debt from Mahindra financials that charges ~14% interest. After the IPO, effective interest rate is expected to be ~11-12% which is likely to reduce further to 9-10%. Interaction with the management indicates they already have an offer from HDFC with effective interest rate of ~9.5%

Valuation

At IPO price, company will have a market cap of ~156crs. In 1H18, company has generated PAT of ~3crs and is likely to cross ~6crs for FY18. It would command a multiple of ~26x at IPO price which is not expensive but not cheap either. Other auto ancilliary companies with similar margin profile trades at higher multiples.

Other Details:

MIBA AG would hold ~20% after the IPO. Company pays 3% royalty to MIBA for the technology/Know-how that they use from MIBA.

Company has an order book of 50crs for New products that it has developed.

To sum up

Sintercom is an interesting company to study. Sintered products demand is increasing globally. It has a strong technology partner in MIBA which is a leading player in the industry. Company is run by a passionate CEO and has strong BoD in place. Further company is only focussing on Auto industry while sintered products finds place in other industries as well. However, management feels they have long road ahead in this industry and hence any diversification will come only when they penetrate this market well.

Key Risks

- Slowdown in Auto markets

- Change in technology

- Increase in royalty to MIBA

- Increase in raw material prices could affect margins

Investment in SME stocks has its own risk. It is always about growth while investing in SME/micro cap stocks. Please do your due diligence before investing.

Discl: Applied in IPO. This should not be construed as an invest advice. Please take your own decision before investing.

Source: Company presentation, Youtube and RHP