1 Like

Hi Any recent update on the company?

Also any update joint venture with Aerotek for MRO services? The FY22 annual report doesn’t mention anything about the JV. Only talks of company named Aerotek Sika

Aviosystems Private Ltd which has zero revenues.

Aerotek SIKA is already a joint venture

I meant in terms of operations? Are they getting decent orders? And how does the financial performance looks like…

I am yet not clear on their capabilities and focus in the MRO business which seems like a small proportion of their business. More info in this regard would be appreciated.

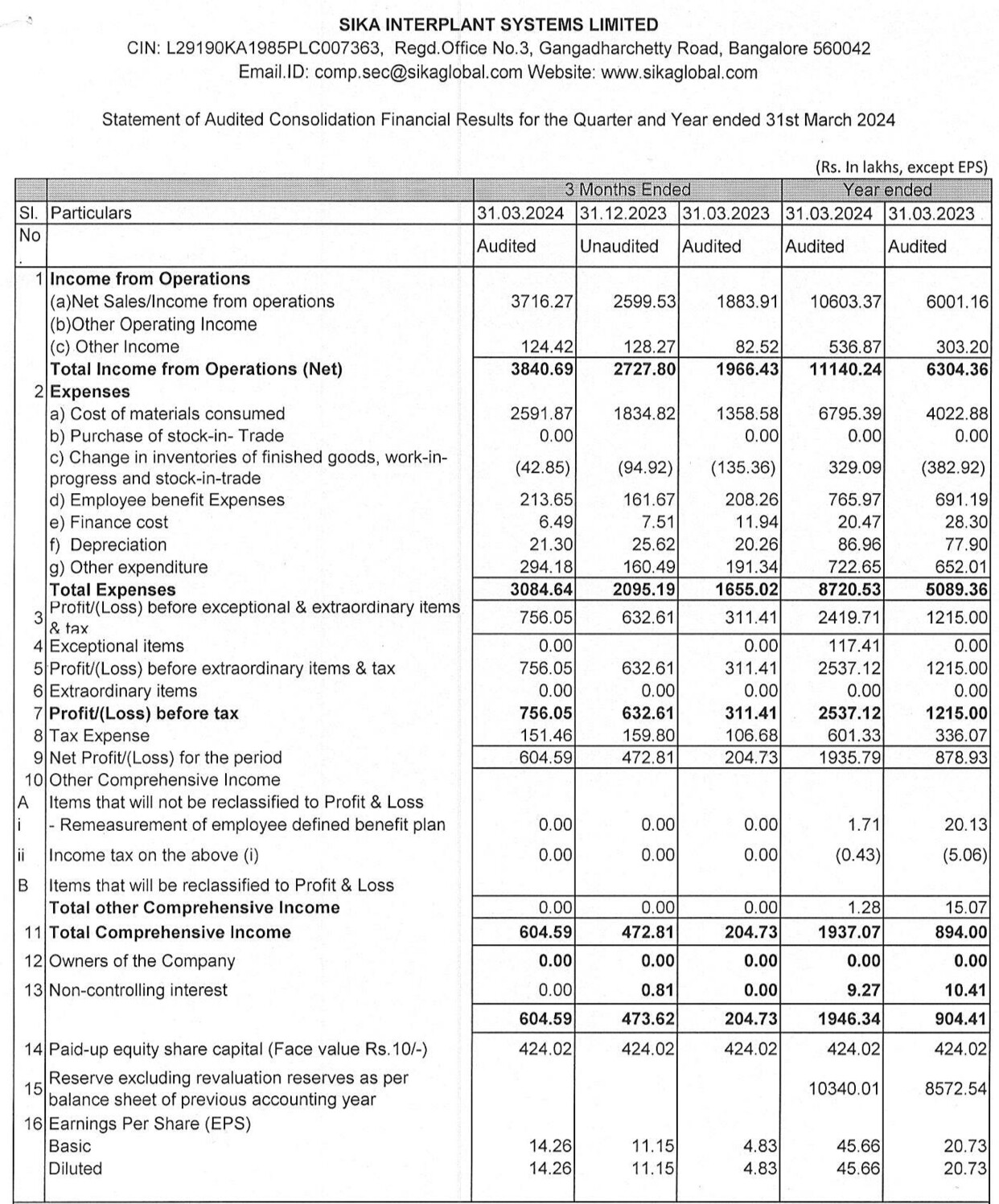

Sika Interplant Systems Ltd. - A valuation exercise

There are several posts previously commenting about the fundamentals of the company. This post is purely about the valuation of the company at the current levels of Rs 1300.

Why the insane run up in price?

- New orders: Back in August’23, Sika announced cumulative new orders worth Rs 117 Cr since the start of the year. Considering the revenue for FY’23 stood at Rs 60Cr, their order book size bagged was nearly 2X their revenue at the time. Hence, the stock soared to new all time highs and the PE doubled. Is the current valuation sensible to enter? The next section will try and clarify the same

- War currents: Two massive wars happening during this time period. The Russia-Ukraine war and the Israel-Palestine war have caused defense sector stocks to sky rocket. Even though Sika as a company does not supply many products and equipment that can be directly exported, they benefit from the increase in order volumes placed by other defense giants. Not to mention, the psychological impact of a war environment on the valuation of the entire defense sector is significant. We all know this euphoria is not going to last forever, and ultimately all that matters is whether the company’s fundamentals is keeping up with its valuation.

Valuation

Sika traded at a PE of 22 in April’23 and today it has doubled to 45. Being a micro-cap company with a Rs 550 Cr market cap, coupled with the points stated above, the stock commands valuations that an explosive growth story would expect. Is it justified today? Let’s run some rough numbers

- Revenue per share (estimate): FY’23 revenue stands at Rs 63Cr. Assuming 50% of the revenue continues into the rest of FY’24, and that the new orders will be executed all in the same year (which is highly highly unlikely, but be it the best case scenario). That should give us an estimated revenue of Rs 148 Cr for FY’24. Number of shares = 0.424 Cr. Revenue per share estimate: 148/0.424 = Rs 350 per share.

- Earnings per share (estimate): Average OPM is around 17%. Another 25% for tax deductions. Rs 350 X 0.17 X 0.75 = Rs 45 EPS (Estimate)

- Fair price (estimate): Current PE of the defense and aerospace sector is 30 (10-year peak is 32, so its trading at the highest possible valuation). So using this PE as fair reference, 30(PE) X 45 (EPS) = Rs 1350

Conclusion

Considering everything as the best case scenario, we reach a fair price of Rs 1350. That is without even leaving any room for margin of error. And today its trading at Rs 1300? Imagine the effects on this fair price when we account for all of the below factors:

- Order book will mot definitely not be executed in a year, even if you were to consider the revenue to be received across 2 years, your SPS and EPS estimates will drop by almost half. And if some are long term contracts then your estimates need to be lowered further!

- Industry PE is trading at a near 10-year high. The 10Y average sector PE is 20. If we were to use this for our estimation instead of the current PE (peak), the fair estimates would be nowhere close. What do you think will happen to these valuations when the wars sizzle down?

In my opinion, the current valuations are ridiculous. I have ridden the defense wave and made my share of profits over the past year. But I simply can’t justify these valuations that small-cap and micro-cap companies command especially when the management doesn’t provide any upfront guidance on con-calls or PPTs. I was unable to attend the recent AGM, but I would like it if someone can share some notes. Let me know if you disagree, and please do share your opinions.

7 Likes