Hi All,

This is about a micro-cap company operating in the aerospace and defence space.

About the Company

Sika Interplant Systems Limited (Sika) is actively involved in four main areas, namely, engineering (design and development); manufacturing, assembly and testing; projects and systems integration; and maintenance, repair and overhaul (MRO).

The Company is one of the select private enterprises with design approval from the Center for Military Airworthiness and Certification (CEMILAC).Sika has also been granted an Industrial License for Defence production from the Government of India, and also a qualified Indian Offset Partner with a license for Defence production from the Government of India-that provides advanced products and solutions to the Aerospace & Defence sector.

This means that Sika is able to undertake such projects and this also qualifies the Company for offset opportunities. A number of international OEMs have significant offset obligations outstanding, and so it is expected that the opportunity from offsets in the coming years will be considerable, with avenues likely to be available both in manufacturing and services.

The company is now run by the next generation Mr. Kunal Sikka who is the CFO and full- time director of the company. He joined a few years back. This change in mgmt. has brought along with it a forward- thinking approach and more Financial prudence.

Today Sika Interplant Systems Ltd. sits on its largest order book since inception. Mr. Sikka has experience in Investment Banking, Merchant Banking & fixed income currency/commodities. Mr. Sikka has experience with Pricewaterhousecoopers Pvt. Ltd., Deutsche Bank AG & Goldman and Sachs. Since July 2006, Mr. Sikka has worked with Goldman Sachs in New York, Singapore & London in various capacities. Mr. Sikka has a degree in Business within finance & management from the University of Wisconsin School of Business.

The MRO (Maintenance Repair & Overhaul) Opportunity

Indian MRO Market Is Estimated to Grow to A Size of USD5.2 Bn by 2026: KPMG

The fleet size of Indian carriers is expected to grow to 1,700+ aircrafts in the next 20 years. The fleet size of scheduled and non-scheduled Indian operators is likely to double by 2020 along with the aging of the current fleet.

The paper (refer sources) also highlights that airlines have their focus on the next big cost item after oil i.e. aircraft MRO, which accounts for 12-15 per cent of their operating expenses. According to industry sources, merely 10 per cent of the MRO work for domestic scheduled carriers is carried out in India. Approximately 7 per cent of airline revenues is being transacted for maintenance in foreign currency. Indian private carriers are heavily reliant on foreign MRO service providers for engine management contracts, component contracts and heavy base checks.

Amber Dubey, Partner and Head, Aerospace and Defence, KPMG in India said, “The National Civil Aviation Policy (NCAP 2016) and the opening up of the defence MRO opportunities have provided the much-needed policy support for the Indian MRO sector. Under the Regional Connectivity Scheme (RCS), provision of low cost, high quality MRO services to small fleet operators is critical. Structural reforms, growing demand for air travel, expanding aircraft fleet and diffusion of air transport services into the hinterlands of India provide the ideal platform for the Indian MRO industry to transform from being mere line or base maintenance providers to value providers.”

“Indian carriers have been sending their aircraft overseas for MRO when the country possesses reasonably good capabilities. Shortcomings if any can be plugged through a win-win collaboration between airlines and MRO providers. India has the potential of evolving into a major MRO Hub within a short span, fuelled by the growing fleet, availability of engineering talent and the forward looking NCAP 2016. The growth of Indian MRO industry will not only save foreign exchange for the nation, but also create employment and help in skill-building.”

The Ministry of Defence (MoD) too is actively engaging with the MRO industry. Aerospace and defence is a focus industry under the ‘Make in India’ initiative and MRO is a key part of it. In case of defence MRO, the training, certification and handholding is done by the Indian Air Force (IAF), which is an added advantage over civilian aircrafts. This opens a significantly large and sustainable opportunity.

The Indian Maintenance, Repair and Overhaul (MRO) industry was worth USD 800 million in 2016 and is expected to grow to over USD 1.5 billion by 2020. However, currently India constitutes to hardly anything of the global MRO market worth USD 45 billion.

The measured steps that the Indian government has taken in moving towards the open sky policy, increase in military, civil and business aircraft fleet in the country, the growing preference for air travel by India’s largely underserved middle class, and the focus by industry to optimize cost of aircraft operations, provides a strong foundation for the Indian MRO industry to strengthen its capability to meet global standards of excellence.

Setting up an MRO is highly capital intensive with a long break-even time. Operating a credible MRO is highly dependent on investing in the right manpower which is regularly trained and optimally utilized with a strong focus on quality and turnaround time.

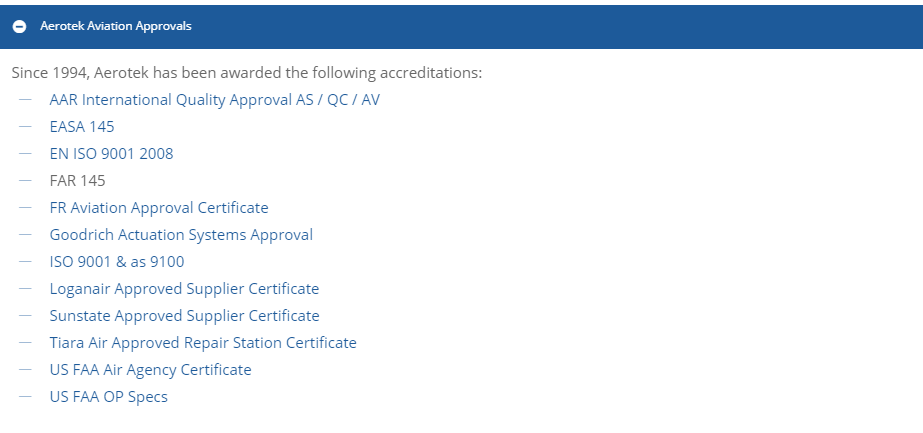

It also requires continuous investment in tooling, certification from safety regulators such as the Federal Aviation Administration (FAA), the European Aviation Safety Agency (EASA) and global OEMs such as Airbus, Bell Helicopter, Boeing, Bombardier Aerospace, Dassault Aviation, Gulfstream Aerospace, Honeywell and others, in addition to certification from the local regulator in order to stay relevant in today’s competitive global environment.

The MRO business is a great opportunity of course but there is a significant barrier to entry in this space and that is getting the required licenses, approvals etc: as stated earlier.

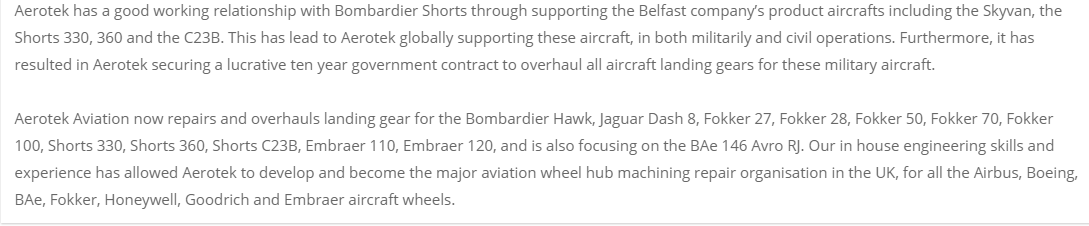

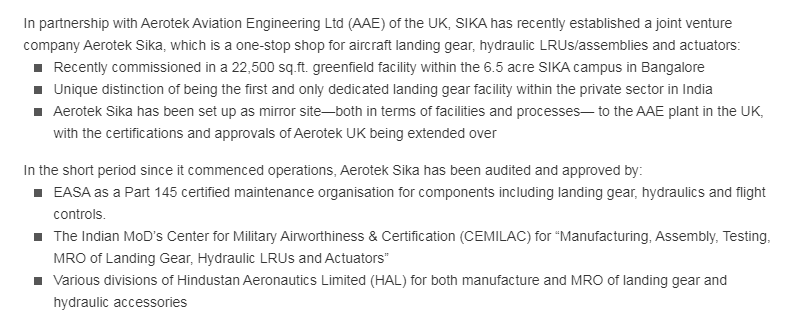

To tap this space and other synergies with its existing business Sika Interplant Systems got into a JV with Aerotek UK.

This JV is quite a big deal as Sika can now enter this space. And the revenues are more annuity based (one would assume) as opposed to order based per se like its defence business.

Aerotek Sika (JV) deals in maintenance, repair and overhaul of landing gear and related assemblies, aviation hydraulics, engineering repair of wheels, cadmium plating and spares supply.

MRO is now an opportunity that Sika can benefit from greatly going forward.

The Defence & Offset Opportunity

It is estimated that during the next decade India will buy close to USD 100 billion worth of fighter aircraft, radars, missiles and warships. Though it is difficult to reach a clear estimate on the value of offsets which will be involved with this huge Defence Import, nevertheless the offsets figures could well be above USD 30 billion.

One of Sika’s largest customers HAL had an IPO recently and it should do a number of good things for Sika as things are now open to scrutiny by the public, investors, vendors etc:

This should further ensure timely payments to Sika as well as timely completion of projects becomes more important to HAL.

Sika should also be a beneficiary of the big offset defence opportunity as stated earlier, many OEMs have significant outstanding offset obligations.

Sika’s Order book

It should be noted that Sika had an order book backlog of around 100cr as of July 2018.

Sika then reached an order backlog of over 150cr as of October 2018 (a 50% jump). What this order book is made up of is not known as data is not available in their announcements. Further there has been no announcement/update on the order book since October 2018.

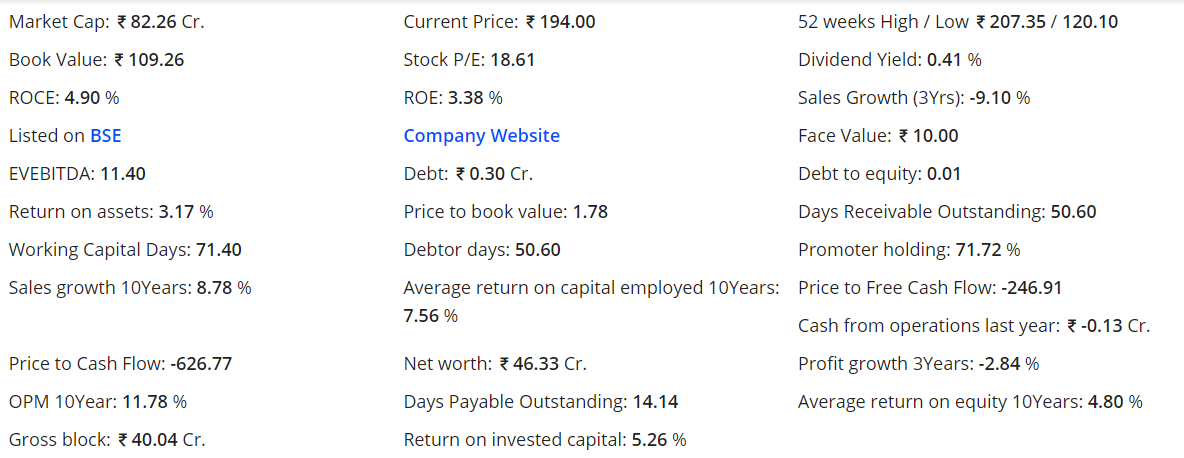

Valuations

The company trades at around an 80cr market cap. And around 18x earnings (Trailing 4 quarters).

It should be noted that the company has land alone that is worth around 30cr. This land is in Bommasandra (Worth 25,43,81,946 as per 2018 AR) and Thimmanahalli (Worth 7,58,344 as per 2018 AR).

The company is virtually debt free which is not the norm and certainly an achievement in the sector that it operates in.

The promoters have substantial skin in the game with a holding of 71%

Looking at the opportunity ahead in terms of earnings, a sun-rise sector so to say, near debt free status, good mgmt., and the various tailwinds in the sector coupled with the high barriers to entry, the valuations look quite attractive.

Risks

Delays from the govt. in terms of orders/tendering etc: The typical risks expected from a business that deals with the govt. or companies dealing directly with the govt. (HAL etc:)

Most of the threats to the domestic A&D industry are rooted on the policy front. These include slippages on the fiscal front, lengthy procurement and evaluation processes, controversies

related to corruption and disputes over short listing in competitive bids. These will serve to delay acquisition plans of the armed forces and impact timing of execution of already longdated projects. Further, given the nature of the A&D business, the products and

systems involved are typically of complex advanced technologies, often resulting in the approval and certification cycle extending for materially longer than originally planned. This can result in delays in production orders and consequent deliveries, affecting the timing of revenues.

The business faces the typical risks associated with a business that deals indirectly/directly and depends heavily on govt. policy etc:.

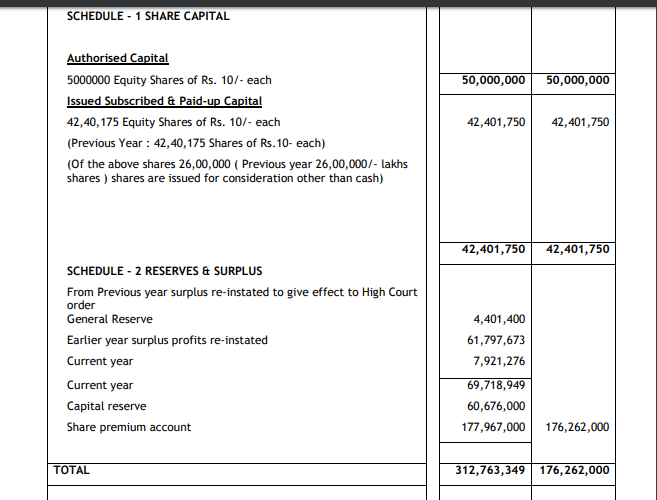

Financial data metrics

Sources

Company AR

http://www.indiamro.in/pdf/KPMG-Report-2016.pdf

Disclosure: A 2% tracking position. Interested in the story.

Year 2019 2018 2017

Year 2019 2018 2017