Any views on the JV @j2eeprofession_

I think we all share the same view on this JV. It has big potential. Has mgmt. given any insights on this aspect? In the current or any of the past AGMs ?

Any views on the JV @j2eeprofession_

I think we all share the same view on this JV. It has big potential. Has mgmt. given any insights on this aspect? In the current or any of the past AGMs ?

the JV is a seperate entity and it cannot carry over the same certifications as their parent company and therefore, they have to apply afresh. The civil license they should get anytime and the defence licence they have already procured. I remember in the last AGM they said they had got a 1cr test order from defence … the defence business does not work so easily that you get license and they start pouring work on you… but now i feel the ground work is already done and the work should come by their way… i beleive this is also one of the entry barriers for the newer players… they will have to undergo all these things and therefore would have to spend years before they can compete with sika… but most importantly …as i keep on saying is that i like this management… i know i would not get a shocking news atleast on this front which in small caps is a rarity and hence i am not overtly bothered by day to day stock price…

Defence psu order books. To be noted that HAL has the maximum with 60kcr followed by Bharat Electronics at close to 55kcr.

It is to be noted that one of Sika’s largest customers is HAL (Bharat electronics is also one of their clients)

As Sika keeps getting credibility in the space (it is my understanding that Sika’s order book has a couple of big orders) they could end up cornering alot of business from these larger defence companies. It is to be noted that L&T tata etc: are on their client list.

Apart from PSUs, as these big private players like Adani, Tata, Reliance, ashok leyland grow their defence JV’s business, would it be safe to assume that Sika might end up becoming a highly preferred outsourcing partner for select works from these companies?

I do not know of any private listed defence company of this size with the licensing and credibility of Sika.

I cannot get enough info on where these orders come from? are they an outsourcing partner for these larger players?

I’m just trying to understand if Sika can grow this order book rapidly, a few big orders from these guys could change the company’s fortunes almost overnight.

Disc. I still hold my small tracking position, views are biased. No intentions to scale it up as of now, mainly because I lack the ability today to study such scuttlebut kind of micro cap ideas.

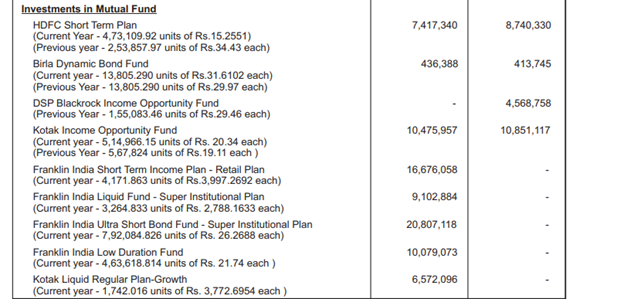

Easily liquifiable Non- Current investments of some ~8cr on Sika’s balance sheet, in addition to ~4cr in cash and equivalents (AR 18-19). This would mean more than 10% of the market cap of the company is in cash.

I think the two big triggers to send the company to the next level are:

It is a three decade old company with major growth in revenue coming only the last few years. I believe the new management is pivotal to growth in revenues as seen in recent years. Also, government has given priority to this sector and is pivotal to their ‘Make in India’ plans which has acted as a tailwind.

Investing in microcaps is risky but I believe that risk reward ratio favours the investor if one invests in potentially good companies. The most important thing according to me while investing in microcaps is the management. Many times the earnings of the company is manipulated or stock is a scam to trap retail investors. One has to be very careful of the management. Also, businesses are subject to disruption and can die out pretty quick. On the contrary, they can have explosive growth and be great multi-baggers. So, it is a double edged sword.

I am trying to study the company, so pardon my ignorance. And please correct me if I am wrong.

Coming to the management, I think the management in this company is not the one for mischievous misadventures. They have been somewhat long enough in the business and working with credible organizations. Having a joint venture with an overseas company would require some good reputation ,in my opinion. They also have sufficient skin in the game with 71% holding. Also, they are almost debt free with only negative on BS being huge upward in receivables. Also, profit/loss numbers seem to be erratic each year which shows lack of manipulation in numbers to fool retail investors. If they haven’t fooled investors for past three decades, they will most likely not do it in future. Succession planning is also there. Management remuneration was less than 1 crore last year. The board of directors has Dr CG Krishnadas Nair as an independent director with 1.8% holding in the company. He was former in command of HAL and has won many prestigious awards. Having such people on board reduces fears of corporate governance and can also provide them good counsel with lifetime of experience in a similar field. One equity fund is invested in it which is headquartered in Bangalore. Other than that, no institutional holding is there, which I believe is great.

The company is available at a Market Cap of 60Cr. Valuations are crazy cheap if you count in the possibility for a steady growth. It has a great potential in many verticals. It will have two strong verticals as per management in future. It is dependent on order book for engineering services as of now. Opportunity is huge and price is miniscule today. I couldn’t find any competitors in India as most MRO is done outside India for civil planes. Cost reduction potential is huge and it would be recurring business not dependent on order book. So, there is 150 Cr order book and an MRO JV in works. These both verticals will bring almost all of the revenue five years down the line. One is dependent on market conditions while other is recurring in nature.

I don’t know the competition of this firm but one thing seems clear. A great management can do wonders with this opportunity. So, taking a bet on this stock is more of taking a bet on management as they will be helped by macroeconomic defence/civil aviation expenditure tailwinds.

As Charlie Munger says’ Invert, always invert’. Some people on this thread have shared really invaluable information. There are a few questions still lingering in my mind when I think of this stock. Many things need clarity and can’t find answers to them. It would be great if someone can clear these doubts to me

It has a great potential and seems like a story worth spending time on. But I believe some more information is needed to make a rational decision.

Disclosure: Not invested. Looking to add tracking position

I do not see any signs of positivity in the above article.could you therefore elaborate or provide data based on which you see the future potential

The industry growth can be huge in india in future. I don’t know whether the company can capitalize on it or not.

For MRO industry

https://www.mro-network.com/maintenance-repair-overhaul/indian-mro-industry-verge-expanding

The net is full of similar articles

For defence manufacturing and offset contracts

Also many articles on the web on defence offset contracts and manufacturing industry.

The industry if given push by the government can grow. Many things must come in order for the company to provide value. Still studying and need more clarity.

Mgmt. Discussion

Now in many cases smaller companies just cannot be bothered because pretty much no brokerage house/big investment house covers them. They will mostly do the bare minimum that is needed for reporting. Don’t expect a godrej like annual report. In most cases it will be same year after year unless there is some major development. I do not know if sika outsources their IR to a capable company or not. Usually if the IR company is good, the reporting of the company will also be great as the IR company will bring out the right info from the management since they know what public investors want/expect.

Aerotek

Aviation is not a space you can easily be a part of. Aerotek has offices across the world. I won’t get into this as there is enough info on their website and you cannot just get FAA, EASA etc: licenses overnight. Moreover they are an official test center for A320 landing gears as well.

Promoter news

For this only those who have met mgmt. at the AGM can provide you with insights. I think @j2eeprofession_ must have in the past and the views are shared on this thread.

It is a sub 100cr company, the promoters aren’t going be part of many public interviews. You can’t expect them to either. I have a link I’ll share it at the end of this.

Competitors of SIKA

In India there are larger MRO companies. You can go through this thread I’ve shared a few links that cover some of them.

The regulatory part is a fairly tough barrier to cross. In fact if I’m not wrong Air India is awaiting its EASA clearance for its hyderabad facility. And GMR’s MRO in hyderabad had its EASA licence suspended last month I think. So it is something to consider. Regulatory barriers in Aviation seem to be quite a significant moat and newcomers will take years to get in and compete let alone meaningfully compete.

Order book is probably made off of many things! I don’t know as details aren’t available. And I doubt they will openly give out details due to them being in defence. Their services etc: are available on their website and Aertoteksika’s website.

I have no scuttleutt, just whatever is available online. Again @j2eeprofession_ might have insights on this.

you can find Mr.Sikka’s write-up in the 21st page I think.

They were supposed to get their civil license by end of this year right ? Any update on that

Nope. I have no idea on the statuses of their licenses.

All info that I know/read is shared on this thread!

Dr. C.G. Krishnadas Nair holds a B.Tech from the Indian Institute Technology, Chennai and holds a M.Sc in Metallurgical Engineering and PhD in Engineering from the University of Sask, Canada. Dr. Nair is a former Chairman of India’s largest defence public sector undertaking Hindustan Aeronautics Limited. He is widely recognized in the field of aeronautics both in India and abroad and was elected President of Aeronautical Society of India (1995-97). He is the Chancellor of International Institute for Aerospace Engineering Management, serves as a Director of the Aerospace and Aviation Sector Skill Council (AASSC), and founded the Society of Indian Aerospace Technologies & Industries (SIATI). He has authored several books in Engineering Technology and Management and has published over 200 Research & Technology and Management papers in National and International journals. A fellow of the Indian National Academy of Engineering, Dr Nair was conferred with the Padmashri Award for outstanding contributions in Engineering Science and Technology. He is also Director of Brahmos Aerospace Thiruvananthapuram Ltd and Global Vectra Helicorp Ltd.

A point to note is that Mr.Nair serves as director and is a major shareholder in the company as well. Holding around 1.9% or 80k shares.

Another set of very strong results from Sika Interplant.

Revenues almost up 100% compared to last quarter while PAT is up close to 30% from last quarter.

Compared to Q3 of last FY revenues are up 60% and PAT is up some 150%

9m ended Revenues up 100+% and PAT up 200+%

I would also just like to throw some caution:

There is a structural flaw in India and that is the incompetence coupled with the poor processes of the Government and similar authorities.

I would like to just reinforce the fact that Sika’s business is open to this structural flaw on both the defence and MRO side.

The MRO industry has been broken for a long time and action is not being taken very actively to help the industry in India.

Defence of course, Govt. is the main factor in this industry.

Please do consider the assumption that both the defence story and the MRO industry could remain in the same status quo for many years to come without any structural reform taking place.

Hi guys anyone knows what is their current order book? And any update regarding their civil license?

This is very good news for Sika Interplant. Finally the govt. has slashed the GST from 18% to 5% on MRO, something the industry has been calling for for a long time.

Anyone knows if their plant is closed during this lock down ? If I’m right businesses related to defence are allowed to function

Recent announcement clearly a huge positive for sika …I think only thing holding them back is the civil licence which they were supposed to get …does anyone have any update on that ?

Hi @sowrabh1818 Which recent announcement are you talking about

This one …but off late this govt has been all talk and no show so need to take this with a grain of salt …however unlike the other govt projects there is a pressing need for this to happen

Hi guys,

This is going to be a long series of posts , which may seem drab at times, but i will cover the complete sector

PART 1: Defence Equipments / Maintenance

PART 2 : Maintenance Repair Organisations (MRO) / Aircraft Maintenance Organisations (AMO) facts, operational and financial aspects.

PART 3 : Feasibility of AMO in India

DISCLOSURES:

I am associated in aviation for almost 25 years in various roles from hands on to Managerial, having worked in Private Aviation, Airline, MRO and with Leasing Companies and as a Consultant.

I DO NOT hold the stock , I DO NOT intend to also. Please read my full post for my reasons.

This is purely an educational post and I am not expressing any Buy / Sell recommendation neither am I authorised to do so. Please do your due diligence.

Airline Stock are considered as “ wealth destroyers “ but i would say Aircraft Maintenance stocks are “wealth devestators”. This is purely my personal view, hence as you guessed it my opinions may be biased . But I will try to be Neutral in my writing.

PART 1 : Defence Equipments and Maintenance.

There are various Govt Bodies who are purely into defence production viz. HAL, BEL, Bharat Dynamics, etc. who come under the umbrella of DRDO and produce mission critical components.The PSU’s are always laggard when it comes to innovation and keeping pace with the current technology; a classic example is our LCA project which is still in development since 1980’s. Its just started to roll out that too with Imported engines.

my conclusion being - Do not expect this company to get contracts for any mission critical components due to confidentiality issues. They will be stuck manufacturing smaller non critical and small margin parts.

There are other private companies involved in Defence production like Tata Advanced Systems, Mahindra Defence Land Systems , L&T Defence, Adani Defence & Aerospace etc. These are mainly JV with foreign competitors. These have got a fillip after the latest FDI norms in defence, but again they will mostly be Assembly companies. No foreign country will want to do a Technology Transfer of their latest Weapon systems. Remember as in the Auto industry, the money comes from spares not sales of weapons / delivery systems.

my conclusion being - If a foreign partner does come in, why will he look at this company when there are already bigger & better Indian companies available? Whats so special about Sika?

Disc- As per initial post.