Siddhika Coating Limited Listed on NSE Emerge, lot size 2000

Siddhika Coating Limited is India’s largest texture paint contract company in single brand segment. Siddhika is marketing & application partner for SK Kaken Ltd. Japan, having its headquarter based in New Delhi and more than 10 branches all over India including Mumbai, Bengaluru, Hyderabad & Kolkata. Its association with SKK is for more than 18 years. SKK is reputed name worldwide in the business of Architectural Coatings, Supplies & Applications.

The company is managing more than 5 million sq. ft. of contract work annually with SKK Products. Their clientele includes most of the prominent architects & developers along with many major institutions, IT Companies, Business Park Developers, and Hospitality Leaders. They provide their services to almost all segments- commercial, residential, institution, factory and even individual houses. They claim that almost 70% of our business comes only from repeat clients year on year. They target to double the quantum of work in the next 3 years with expansions on territorial grounds and product portfolio.

Product portfolio is available in this brochure:- Siddhika Brochure.pdf (2.9 MB) Financials:

The company has been profitable throughout, in good and bad times.

The company touches a topline of almost 30 crores and profit of 3.8 crores in 2020, before covid.

The operations were disturbed in covid times, leading to drop in topline; nevertheless the company remained profitable.

In normal times, the company is showing a profit before tax margin, upward of 10%.

The company has been paying dividends. In 2021, it paid Rs. 2 per share, and in 2022 it paid Rs. 2.4 per share dividend.

In H1, 2023 the company has declared a topline of 14 crores and net profit of 1.35 crores and eps of Rs. 4.37. Thus, with slightly better H2, we can expect an annualised eps of Rs. 10 in FY 2023. Valuation:

The company has an equity base of 3.1 crores. Thus, at Rs. 135 current market price, the market cap is around 40 crores. Taking current year sales at 30 crores, and eps of Rs. 10; the valuation looks very attractive- merely 1.3 times sales and at a p/e of 13.5. Based on past dividend payouts, we can expect Rs. 4 dividend, leading to a more than 3% yield.

Combined with the management goal of doubling sales in 3 years, we have a very attractive growth share at a very reasonable price.

Basis of Investment:

There is only one basis of investment in the company- it is fast growing small company, which is growing without much debt infusion and with decent profitability. If such growth continues for a few more years, it can prove to be a decent investment. Risk:

-Investment in nano caps can lead to 100% capital loss.

-We dont know the SKK plans for India going into future.

It is basically dealership of SKK. The product offering is modest at best. PEG ratio is (-)3.58 and a volume under 10000. Under these conditions, I wonder if its good for us.

Very True. They import their product and sell them, and in that sense, they are basically a dealership. However, they add value by application. The other aspect is the process- most of the MNC paint companies enter India through dealerships only. Sirca Paints was also a dealer till a couple of years ago. However, we don’t know SKK’s plans and strategy in India.

PEG ratio is appearing negative because of covid disruptions. Management believes that volume can grow double in 3 years, and based on that I believe that they can grow at the rate of 24%.

Yes, the volume is less as it is normal in SME listed stocks.

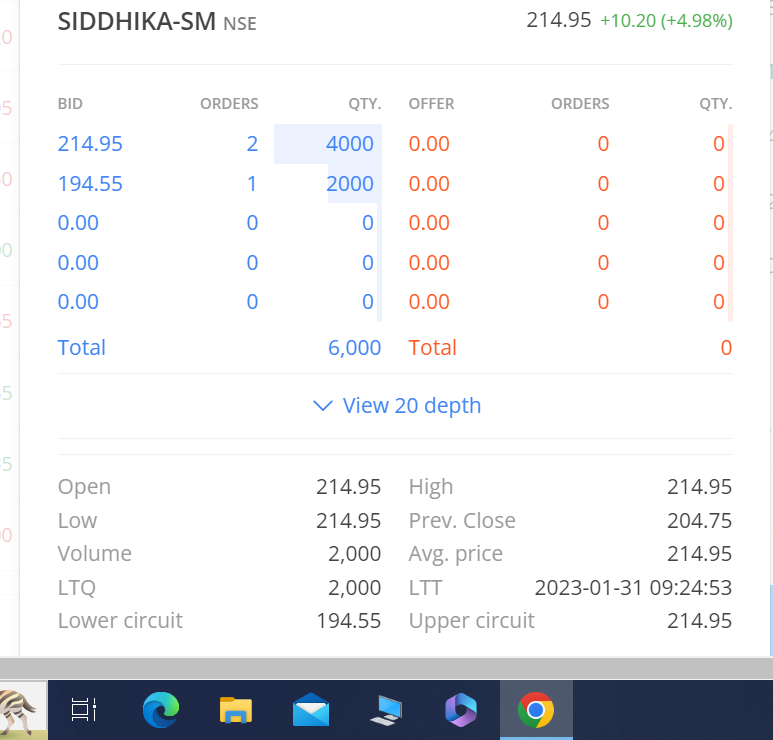

Looks like some accumulation is going on in the counter. The counter is in the upper circuit for the last many days, whatever sell quantity comes is being absorbed.

@rk1771, yes no volumes and highly illiquid stock. Hence prone to operator manipulation. Predominantely its a trading company (95% revenues), but commanding expensive valuations (PE 40).

I don’t think it is a trading company- it is a paint application company. Thus, they don’t import and sell paints, they import and apply. As they apply the products their margin is good. They did have fall in topline during covid, but now they have recovered their topline too, this year I estimate that it may touch 30 crores. Their profitability has always been good, and it may touch 12% this year. They have done well in H1-2023, and declared Eps of Rs. 4.37 in H1. Going by the past trends of better results in H2, we can expect an annualized eps of Rs. 10 in the current year.

These figures command trust as in the last 2 years, dividend payout has been in the 40-50% range. Even on a 30-35% dividend payout this year, we may expect a dividend payout of more than Rs. 3 this year. Thus on a current year earning, its p/e is around 20, and the dividend yield of 1.5%; not bad.

The real issue which needs to be examined is scalability- can it scale? We have no history of any paint application company in India. On a global scale there are a few reputed paint application companies- Sherwin Williams which command lofty valuation and market cap. Can we have such companies in India. It may be noted that even established paint companies like Asian Paints have started taking application work.

Today the company has a topline of 30 crores. Certainly, it can touch a topline of 100 crores or 200 crores going forward, that scalability is always there. Can it go further? If it can go further, in my view it is a gem.

Yah, hardly 1-2 lot is being traded. But I have felt that the moment a sell lot is offered, it is grabbed on whatever prices it is offered. However, whoever is accumulating wishes to keep the prices lower and buy orders are placed closer to LC.

Today appears different. For the first time I am seeing open buy orders on UC. Le us see if some sellers emerge.

It has come out with annual results. Topline has gone up to 33 crores, with PAT of 3.5 crores. EPS is Rs. 11.41, and the company has declared a dividend of Rs. 3 per share. Net cash from operating activity is around 5 crores. On consolidated basis the topline of around 35 crores and PAT of 3.7 vrores. OUTCOME_24052023135436_compressed.pdf (2.9 MB)

On 12 Rupess eps, the stock is trading around 206; looks reasonably priced.

Disclosure: Invested

Annual report of the company is out. Keep takeaways-

The company is expecting that going forward the clients will start looking for more organized service providers, i.e. paint applicators.

Debtor days have improved from 64 to 36 days.

Company’s working capital requirements have reduced from 117 days to 63 days.

Inventory turnover ratio has been improved from 3.35 from 2.1.

Company margin has improved, net profit margin is higher than 10%.

Quoting management-

“Demand for SKK paints & our services are still good. We look forward to business moving back to normal in construction industry. Recent optimism in real estate sector adds to our confidence on growth. We also expect demand to pick up in our segments of façade renovation once 100% work from office is back on track.”

The AR is available on NSE site.

[Disclosure- Invested and biased]

Yesterday bulk deal happened in Siddhika. The person who sold shares is not shown in existing shareholders list. It may be possible that he bought slowly after March 23 and yesterday sold. All shares were quickly absorbed. @rk1771 if you have any information about yesterday’s bulk deal please let us know.

Have you got any chance to interact with management, can you share your view for OPM, how you think it will have in future, will it remain in two digis? I have been tracking this but not able to have confidence yet due to bad topline.

Once I requested and they were very willing to meet. I could not meet at that time. I am also connected to the CEO and some other employees on LinkedIn, and they keep on sharing company’s update there.

On OPM, my view is that they will maintain that margin in 2 digits. Paint application industry is moving from unorganised to organized, and this is a great wealth generation trigger.

On topline, I have found from their LinkedIn post that recently they completed painting of a reputed hospital in Delhi (A Tata Project) and they were rewarded a certificate for good service. I can see they are doing work in various schools and colleges, commercial buildings in different parts of India. My view is that though the topline will not jump, it will keep on growing at a decent pace of 20-25% in foreseeable future.

Though management has never stated this, once their paint application business gets a decent size, SKK may be keen to enter into India in paint manufacturing and it may become a vehicle for paint manufacturing (purely my speculation). Similar thing has happened in Sirca, who became paint manufacturer after doing import and distribution work for some time. India is too big a market for SKK not entering into India.

As a prudent public investor, I don’t wish to ask futuristic questions like future plans, future sales and margin from management. I am happy with whatever they announce publicly.

On a present analysis, a paint company is available at 16 p/e, with 20-25% expected growth, 1.6% dividend yield, debt free… enough for me.

(Disclosure: Invested)

@rk1771 Happy new year !! Recently the stock started to show some positive movement. While I believe the stock is a niche play in the paint segment and has good prospects going forward, was there any positive development that prompted this move? Thanks

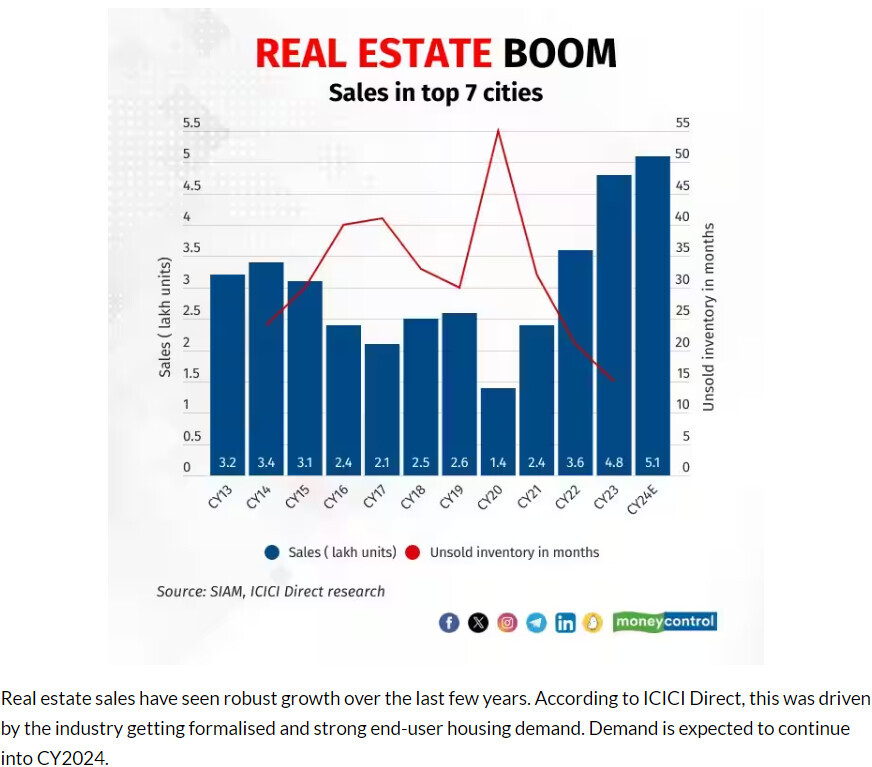

Real estate boom can help the company.

The company is in a great business niche, and I think it should be a bit more aggressive in pursuing growth. They have started new branches- now more than 10, which should help them in growth.

The company is earning decent profit, distributing good amount of dividend; in the H1- 2024 results, they have invested more than 5 crores of rupess in mutual funds!! Siddhika.pdf (7.5 MB)

Extrapolating the figures, the company is likely to earn INR 15 eps in the current financial year. What will they do with this money? If they keep on investing in mutual funds, RoE will fall.

Management must look for more business opportunities to employ the profit they are generating.

Most of the corporates which were working remotely are now going back to working from offices. So repainting contracts from these clients, apart from the real estate boom will drive the growth for this company IMO. Also it is to be seen, if the management has any plans to manufacture SKK brand products in India instead of importing them.

I will really love to hear from Management further growth plans.

They have started offices in more than 10 cities. Thus, some growth will come from new businesses.

With the new business in the same vertical, i.e. paint application; they can grow at 20-25 percent per annum.

Paint application can itself becomes a great business as “organised sector replacing unorganised sector” theme can play.

The real issue here is “capital allocation”; how will management deploy the cash generated from the business.

If they prove to be great capital allocators, it can be a good long term investment.