@james_kerala Yes, I am very much invested & have been in buying mode for the last few months. The results have been gratifying. Q2 was very good, but Q3 was even better! I don’t want to extrapolate numbers but if the current run rate is sustainable, then the stock could double & still be a buy!!

Clearly, getting DP World on board has been a game changer, in that Shreyas does not have to go looking for business, which is perhaps where it was struggling somewhat. DP World is mainly in the business of managing Ports & has the wherewithal to manage Port traffic, & thereby get business for Shreyas. It’s a win-win for both, as Shreyas has the right to first refusal if the proposition is not attractive. Perhaps the street has not fully appreciated the new business model. Its not that Shreyas has sold the business to DP World & is merely leasing its ships. It continues to run the business with a 2/3rd share of profits from the operating Co. It is just that after this new arrangement with DP World, only the 2/3rd share the operating profits due to Shreyas is reflected as revenues. So the total revenues have understandably reduced substantially, but so have the expenses as all revenue expenses including bunker (fuel) charges are now debited to the operating Co.

Another point to note is that the operating Co. itself is very much managed by Shreyas in that the crucial man power like the earlier CEO etc. have now been shifted to manage the operating Co.

Part of the business, the break bulk side continues to be directly managed by Shreyas as before & Shreyas feels there are enough opportunities there as Shreyas continues to add to its fleet for this business. The arrangement with DP World as of now is for the container business only.

If the Fuel Cost (bunker Cost) has increased higher as compared to increase in Freight rates for the quarter, then in that scenario Shreyas will get lower Lower charter income (2/3rd of EBIT) as Operating company will have lower profits. In that scenario Charter Hire Income will not be fixed income and will continue to have impact of Bunker Cost and Freight Revenue (Linked to Time charter equivalent).

Shreyas has get the Synergy benefit to get better Freight rates and operational efficiency of Voyage Exp (i.e. Fual/Bunker Cost).

Global Player - Maersk

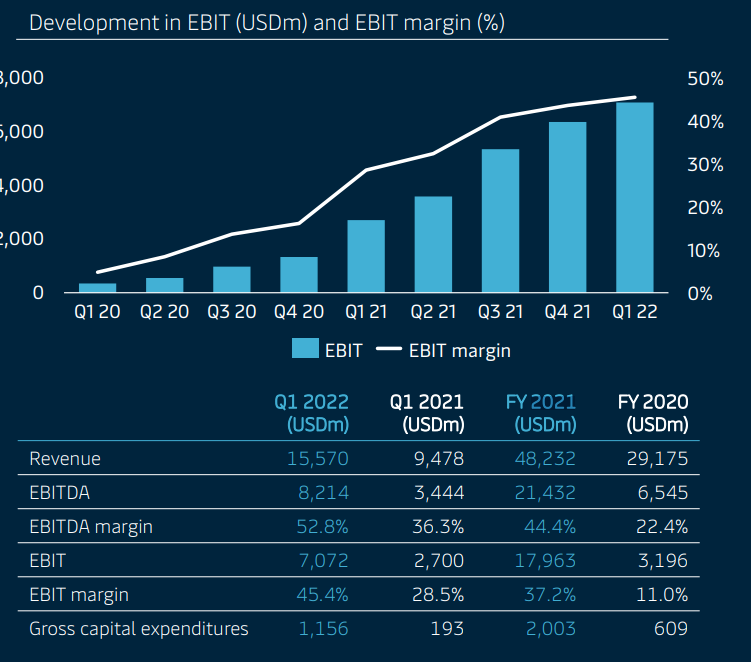

Maersk Q1 2022 Result indicate increase in EBIT Margin by2.5% (52.8 %-50.3%) as compared to previous quarter

But it seems the company is evolving from a regional coastal container trade to dry bulk also, which changes its profile. The company’s website shows some of its vessels outside India’s coastal waters.

DISC: Just invested in the company and plan to increase holding.

Shreyas Q4 numbers clearly indicate that the uptick in the shipping business has only just begun, & the current run rate is clearly sustainable & could perhaps get better as increasing the supply of vessels is something that takes time. The profit for the year gone by 2021-22 is Rs. 211 crs with the profit for the second half itself coming to Rs. 134 crs. The market cap is only 765 crs. As the mood of the market improves, the stock potentially can go a long way from here.

About the Co. paying low Income Tax, I understand that shipping Co.'s have the option to pay what is known as tonnage tax which is a scheme of presumptive taxation wherein notional income arising from operation of ships is determined on basis of tonnage of ships. This is probably much lower & is available to all shipping Co.'s. The Co.'s availing of this have to create a reserve that can be used to augment their fleet.

All in all, the tide seems to have turned for the shipping industry!

While the numbers are impressive. How can one confirm that the uptick has just begun and this is not an aberration for a year before things normalize at a lower level (albeit much better than earlier - due to integration with international market)

Average core EBIT margins for the big global container liner companies reached another record high of 57.4% in the first quarter of this year according to Alphaliner. This should bode well for Shreyas though it is primarily in Indian coastal trade. Maersk though thinks 2023-2024 may be loss-making for the container sector.

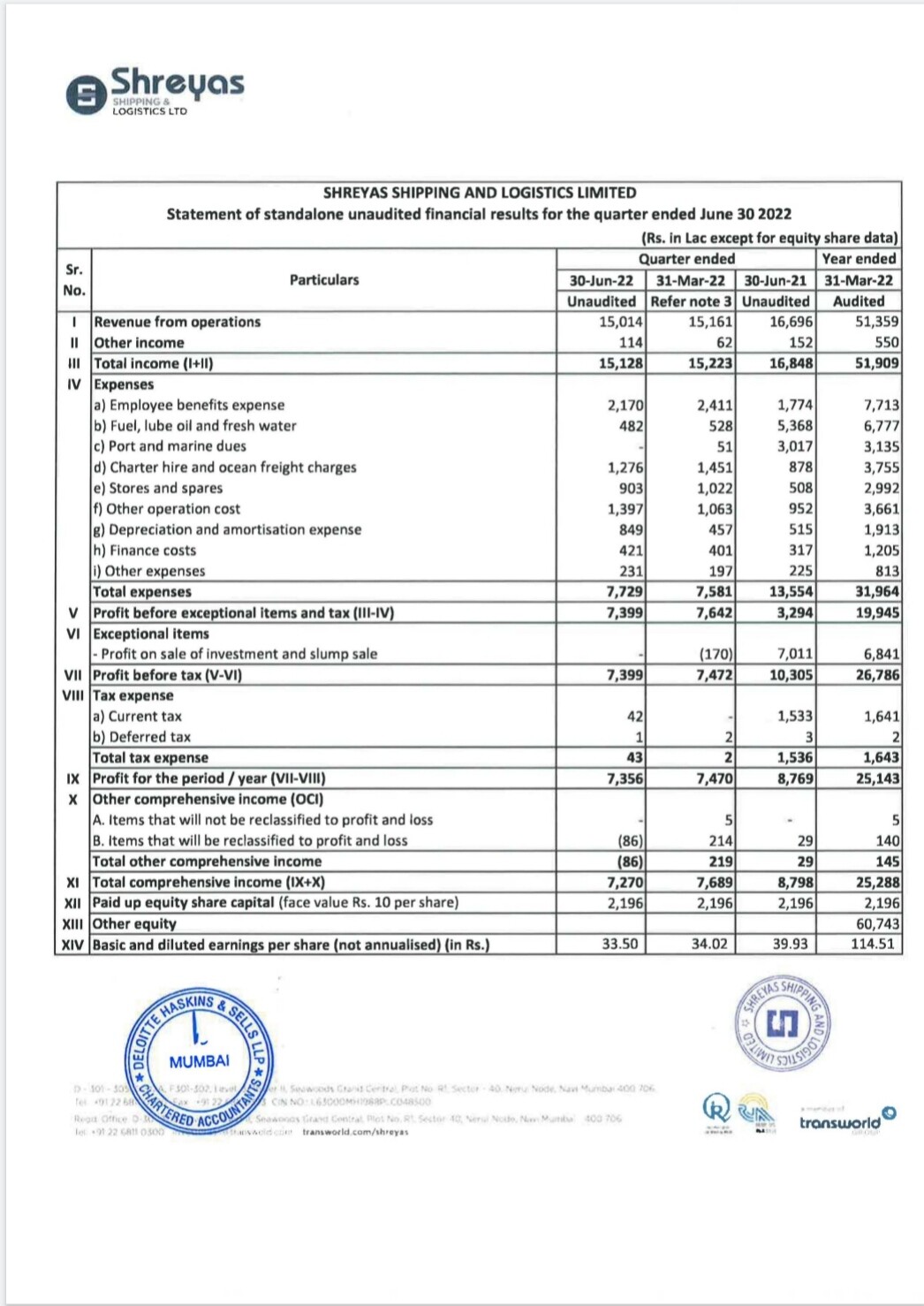

Exceptional results. They should host a con-call to give more clarity on whether the performance is sustainable. The growth in profits is phenomenal - Looks lower optically compared to Q1 2022 as there was an exceptional item of sale of business in last year same quarter. Looks like they will clock an EPS of Rs.100+ even though container freight rates have come down (compensated by increase in 2 dry bulk vessels procured recently which are doing very well ) .

Hi. Where can I read more about this co? I don’t find any concall or management interview? Also with declining freight rate, do you think the margins are sustainable?

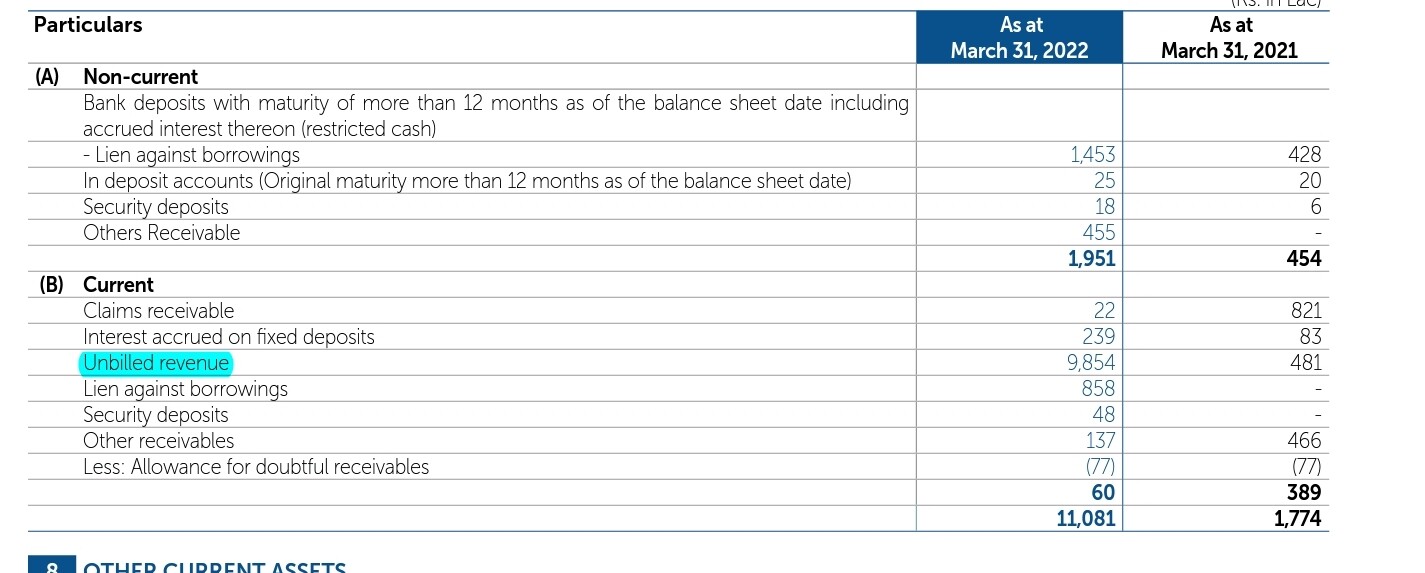

Could anyone explain why there is such a huge % of revenue is sitting as unbilled revenue and i guess same thing is impacting the cash flow from operations ( which is not inline with profit). Is this a red flag. Because 100 cr is huge number

Unbilled AR is an Asset account on the balance sheet that represents amounts recognized as revenue for which invoices have not yet been sent. This can occur when you invoice in arrears or have any delay in billing relative to the revenue recognition trigger date.

As the charter is to a good group I do not see much risk here

Posting in the forum after a gap. How are you all?

I was wrapping my head around this since yesterday after seeing Shreyas shipping at PE 2.5.

A business (post DP deal) with OPM=40+%, ROE=30% and ROCE=40% and DE=0.33, with no WC requirement at PE 2.5? Markets can be inefficient but can it be so crazy? Why not go in for an opportunistic investment until it catches up and valued correctly by the market? But can the market ignore such a no-brainer opportunity for so long? I was confused.

However, after reading through Aug 2020 conf call transcript, I see a Seemant from Unifi Capital questioins the cheap valuations at which the businesses are sold and that the deal is not in favour of minority shareholders, the same point already mentioned in this thread.

I also can see the same news in ET:

The promoters had also sold a pvt entity as part of the deal and got a 17% stake in DP world. Could there be some foul play by the promoters to hide the actual money involved in the deal from the minority shareholders? Could this be the reason why the stock is not catching up? Recall LEEL? I do not know, it may be or may not be true, however if there is any chance of this to be the truth, which one can never know for sure, I wouldn’t dare to touch this stock. From a risk management angle, finally I decided to drop this one.

Unifi had exited the stock as well, back in Dec 2020.

Shareyas (SSL) was struggling to grow the business on its own for several quarters prior to selling the business to a JV in which it holds 67%. DP World, which holds the balance 1/3 share of the operating Co. and is in the business of managing multiple ports is in a far better position to arrange for greater traffic/ growth in the shipping business. This is evident from the numbers that have come in post the transfer of the business to the operating Co. The Sales figures in SSL’s P&L represent largely its 2/3rd share of profits after deducting the operating expenses like fuel / man power etc.

That said, as the noted economist Keynes has stated, “valuations can remain irrational/ compelling far longer than investors can remain solvent”!! There is no knowing when the market in its wisdom will give the company proper valuations, if at all. I feel something has got to give sooner than later……either the numbers will not sustain or valuations will improve meaningfully.

Current book value is 345 and the last few quarters results also good, but still stock is trading way below the historical PE. any specific reason, may be the management should do buyback to improve the sentiment.

ShreyasShipping & Logistics Limited has signed a Memorandum of Agreement (MOA) on 14th February 2023 for acquisition of one container vessel of 2872 TEU (35538 DWT)