The company is currently trading at a P/E of 2.06 and an EV/ EBITDA of 2.36. I was interested in the company for some time but had very few data points to understand the business. The shipping industry is a cyclical industry and had a very bad cycle till the covid crisis bought in an unexpected boom to the industry.

Conventionally, in cyclical investing shares are bought when the P/E is very high as earnings get terribly affected during downcycles.

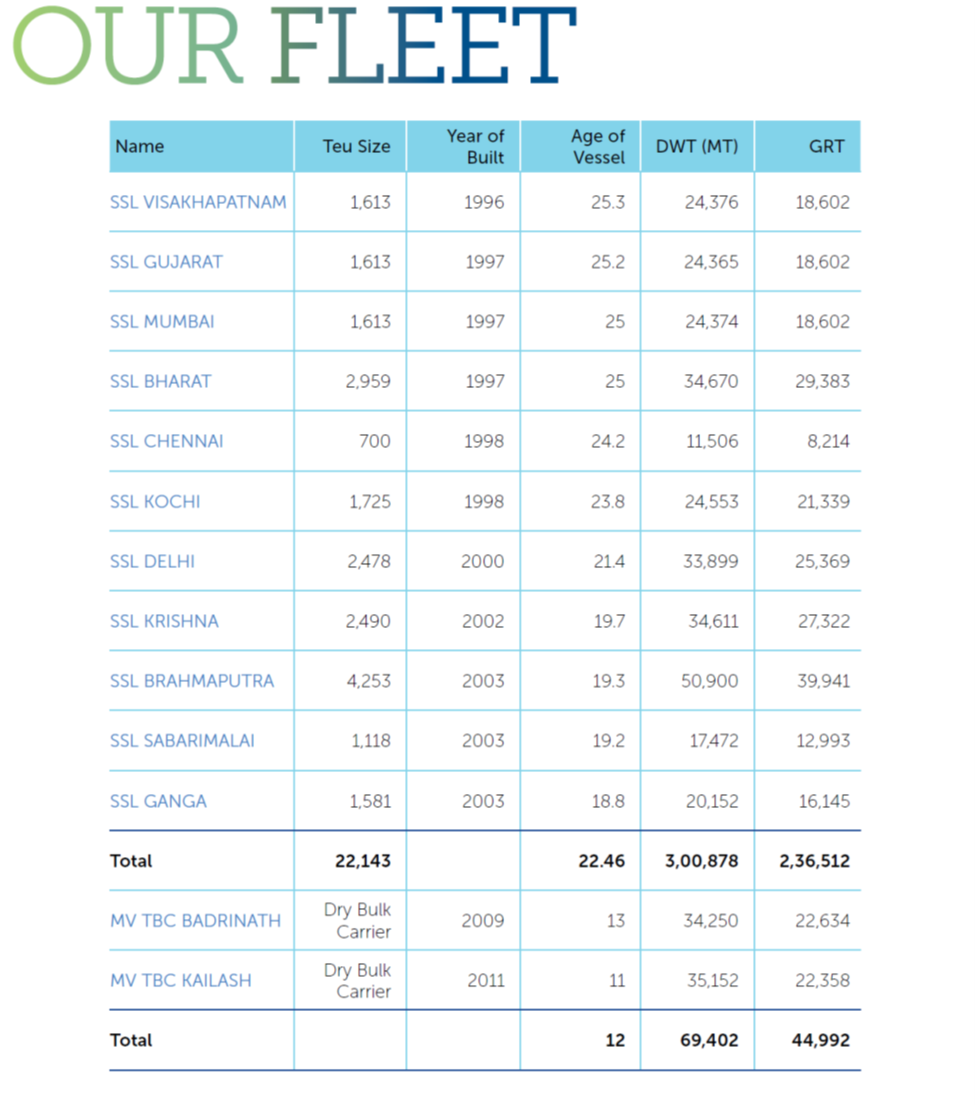

As per AR’22, the company has 11 container carriers and 2 dry bulk carrier vessels.

The company’s OPM jumped significantly after its deal with Unifeeder.

Source: Screener.

As per the earnings release on 14 February 23, all its vessels are on charter. As all its container vessels are on charter, only vessel operating expenses are incurred by the company, and voyage expenses are incurred by the chartered company.

There is very little info or disclosure from the company since 2020 after the arrangement with Unifeeder.

The company has small feeder container ships which can be used in coastal shipping. The one thing to note is that the average age of ships as per AR’22 is 22.46. The government of India recently proposed a plan to ban all 25-year-old oil tankers, bulk carriers, and other ships.

Source: Government set to ban 25-year-old oil tankers, bulk carriers and other ships calling Indian ports, ET Infra

If this is implemented, the company will have to replace most of its ships immediately. Shreyas has already pointed to the need for the replacement of ships. As per care ratings, SSLL has a capex of 300 crores planned for the next 3 years for dry docking and replacement of vessels. Most of the cash flow over the next few years will be tied up in capex and debt will also increase. SSLL has recently purchased 3 ships.

- Kaveri - 2007 – 2553 TEU

- Godavari – 2010 – 2872 TEU

- Thamirabharani – 2005- 962 TEU

The company doesn’t disclose the cost of these acquisitions which makes it difficult to understand the capex required.

However, as per a news report from Hellenic Shipping news

Feedermax Sky Pride (962 TEU, Jul 2005, Dae Sun) sold to undisclosed buyers for USD 8.50 mil, VV Value USD 6.45 mil – DD Due. (69 crores)

Source: https://www.hellenicshippingnews.com/weekly-vessel-valuations-report-february-21-2023/

This can give us an idea of the capex required for modernizing the fleet.

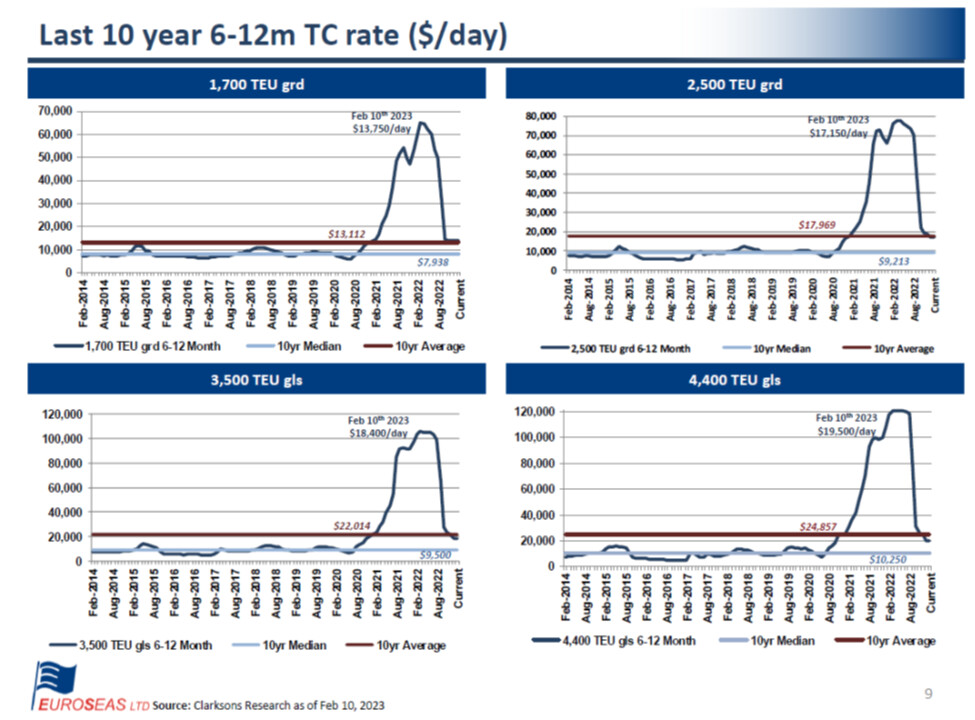

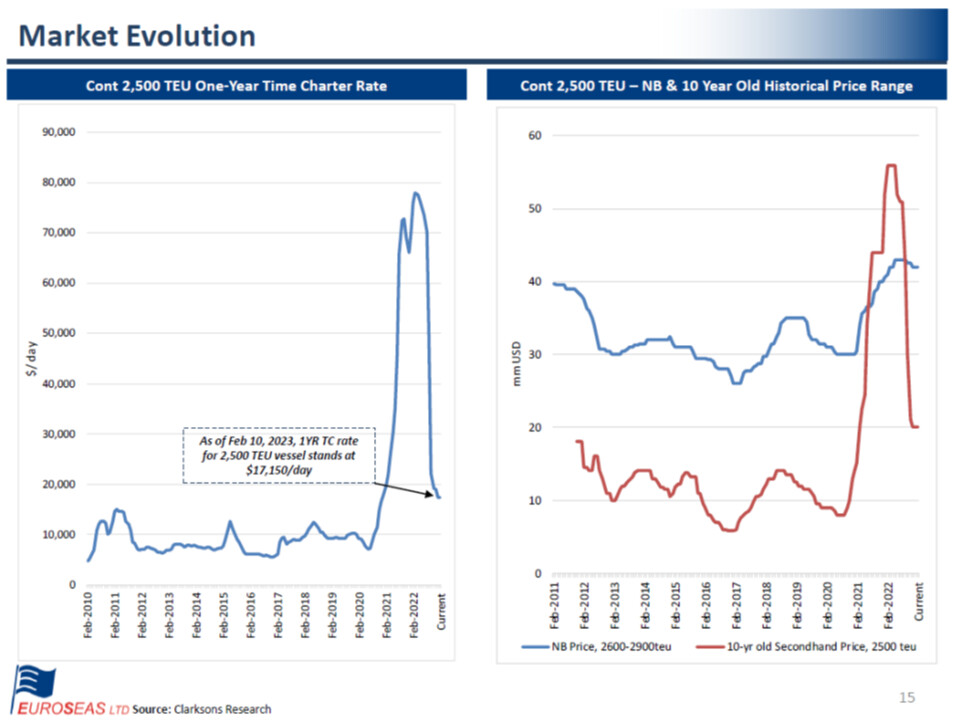

At this point, I am totally discounting any CG issues in the deal with Unifeeder and considering this as a cyclical play. As a cyclical player, I must be considering time charter rates, the order book for small feeder ships, the age profile of existing ships, the cost of second-hand ships, and scrapping activity. Well, all the data SSLL could give was about the Baltic dry index and Robinson howe index in its earning releases. So had to find out a peer and I think Euroseas fits the description. Interestingly, Euroseas investor presentation provides a lot of insights.

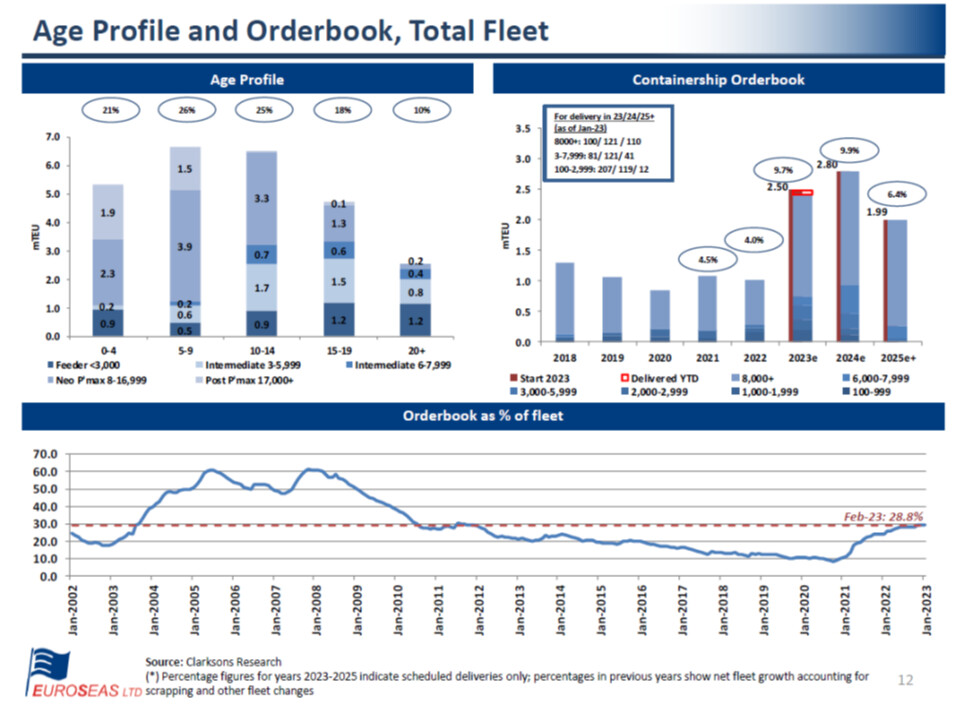

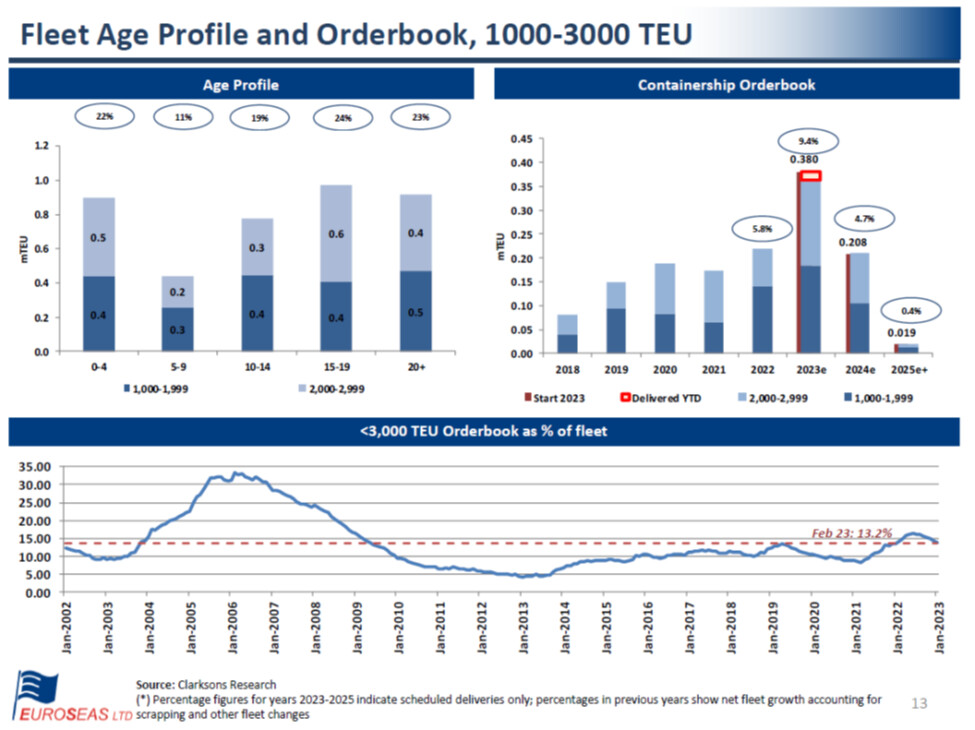

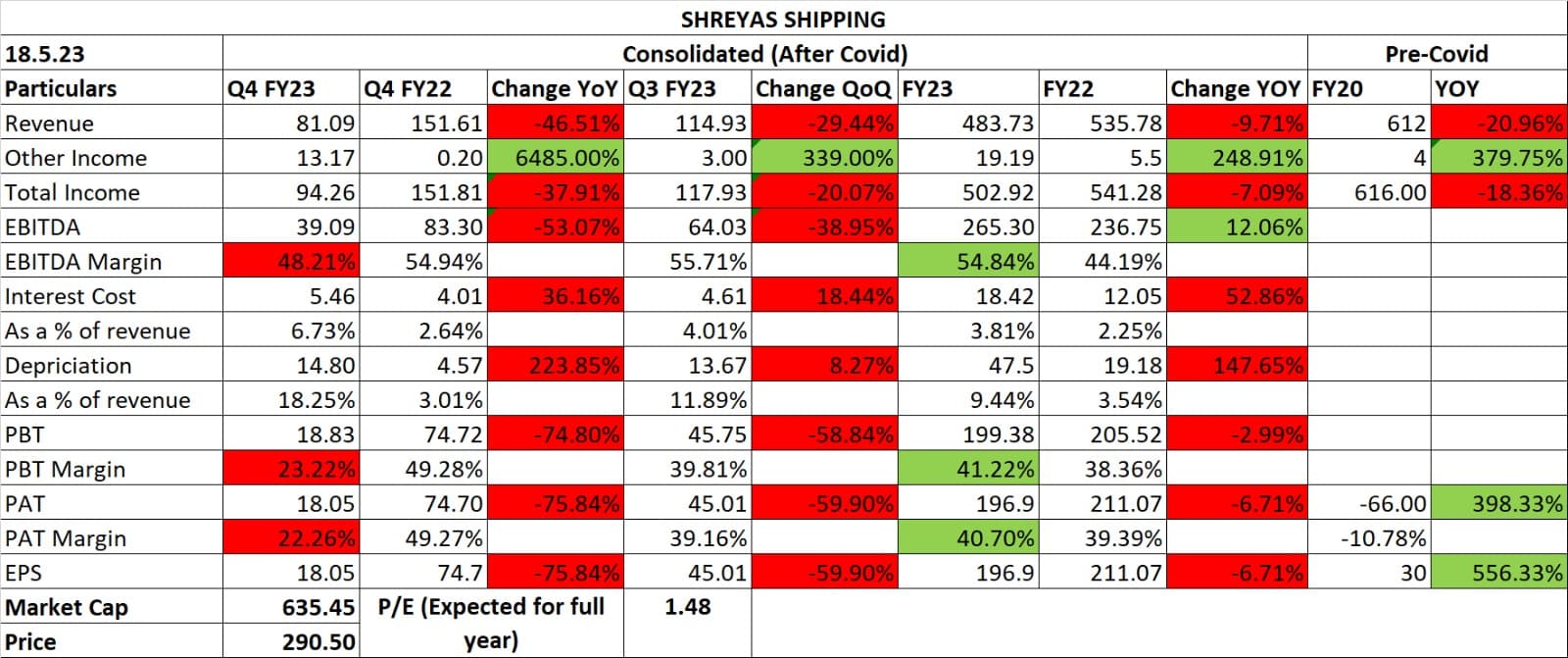

It is good to see that SSLL managed to generate an EPS of 20.50 per share even after time charter rates falling so much. But it should be noted that it is considerably above 10-year average. We may never see the highs of time charter rates or container indexes during covid in our lifetime. So trailing PE analysis is almost meaningless. One may also notice that the order book made a sharp jump in 2022 and a good number of ships are up for delivery in 2023 which may put more downside pressure on Time charter rates. Euroseas alone has 9 feeders up for delivery in 2023 and 2024.

To conclude things, I believe the turnaround in time charter rates is still a few years away with the new orders getting delivered. SSLL will need all its cash flow along with debt to modernize its fleet in the next few years. The company should do well in the next upcycle. But I believe that the downcycle is still not over. On the plus side, 10-year second-hand price of feeder ships has come down sharply to 20 mn USD which will benefit Shreyas while looking for replacements. SSLL is looking for older ships so their price will be lower. As steel prices look good and with TC coming down there will be incentives to scrapping of ships which may balance supply to a certain level.

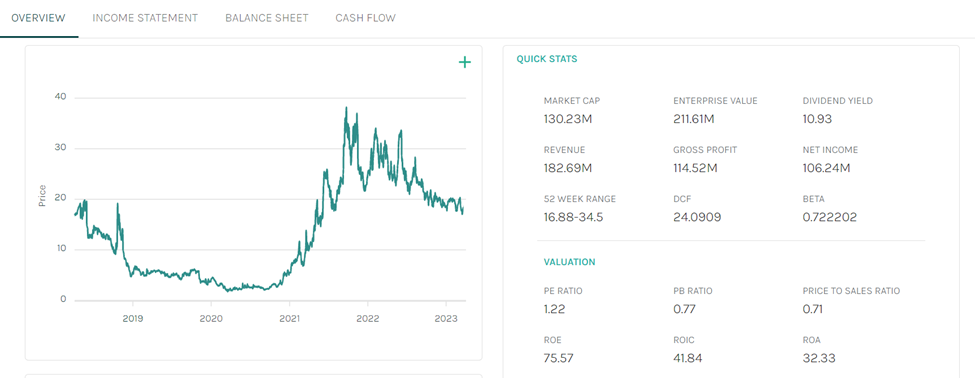

Euroseas is currently trading at a PE ratio of 1.27 and a dividend yield of 10.93 % on a trailing basis.

Discl: No investments. I am not a SEBI registered advisor. I could be wrong about the cycle. I have used the Euroseas earnings presentation for drawing most of the conclusions. Euroseas quick stats snipped from potley portal. Notes may not be in any proper order.

earnings release q323.pdf (317.2 KB)

Euroseas-Q4-2022.pdf (1.8 MB)