some jottings as below about the impending sale deal

presentation link - https://www.bseindia.com/xml-data/corpfiling/AttachHis/2400602b-f346-4c6a-9bc7-62eacce129c8.pdf

(this is post the q1 concall, whose transcript is also worth reading) - https://www.bseindia.com/xml-data/corpfiling/AttachHis/f736d541-d309-4102-965a-dea5db6a841b.pdf

if i were to cut through the clutter regarding the deal, basically nothing much is changing from company’s Balance Sheet point of view except that they are converting their net working capital to upfront cash - so all adjustments are happening in the current asset / liability side only.

getting cash of 200cr.

settling the working capital debt of 80cr

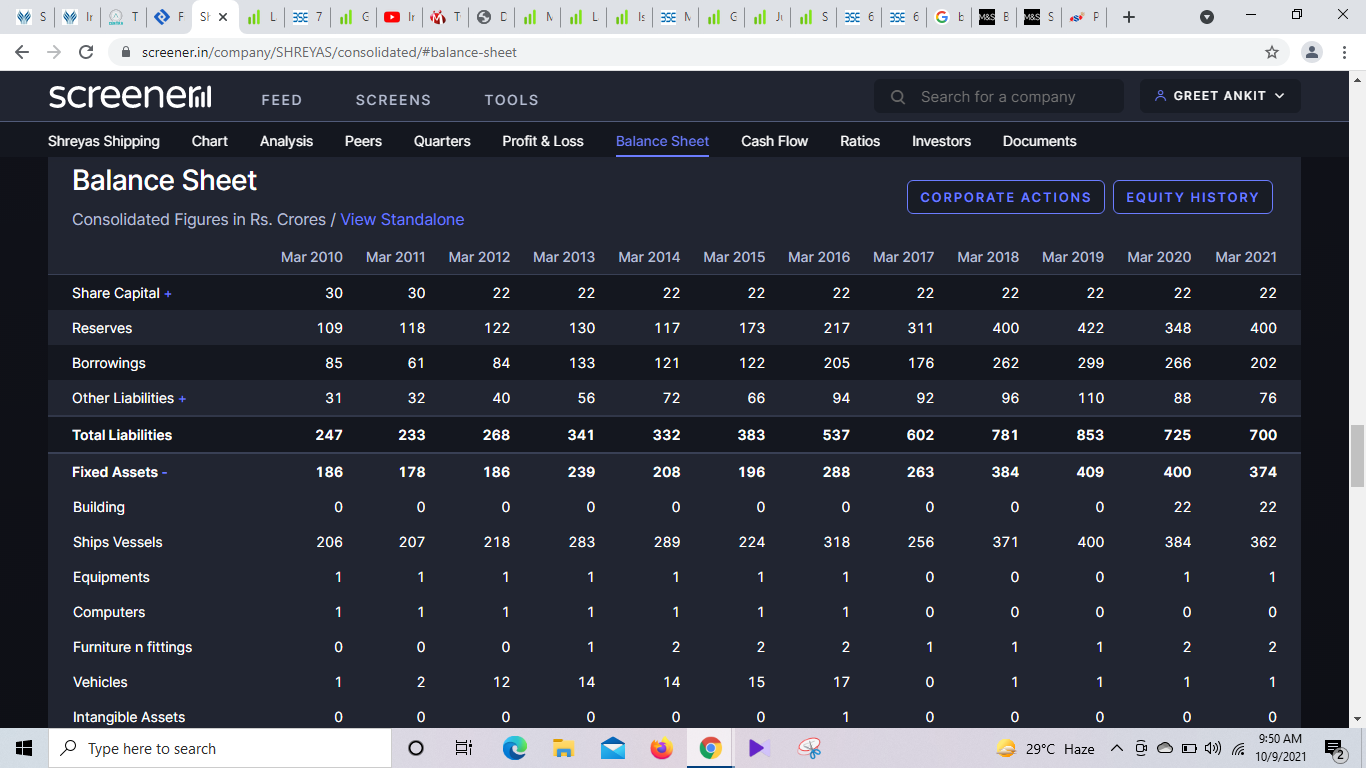

so they have 120cr net cash and 185cr long term loans. and 350cr ships. and no WC - ie no receivables, inventory and payables. BS becomes light to this small extent only. all fixed assets continue to remain on the books.

unifeeder / dp world will become their significant major customer due to the FCA. income stream becomes less fluctuating due to charter income. they said charter yields are same or slightly lower than yields they earn when the themselves operate the ships, but the yield is more uniform over time because they are not exposed to fuel costs. and unifeeder/dp world being much much larger entities, shreyas will get assured business.

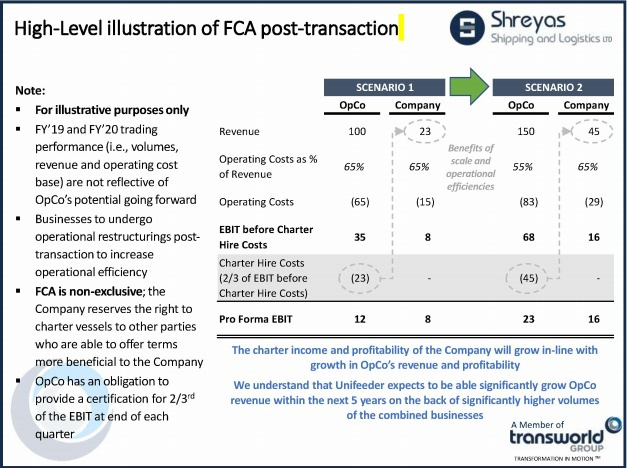

to get some idea of how their PnL would look like after the deal, this slide from the presentation is interesting:

if what i have understood from the above is correct, unifeeder will pay them 2/3d of their ebit (certified) as charter hire, which becomes income for shreyas. though absolute scale of operations might decrease, profit margins will be much much higher. due to their size, dp world/unifeeder would be in a better position to manage the fluctuations in fuel costs, atleast in comparison to how shreyas would have been managing it.

regarding capital employed - if shreyas takes on WC debt to fund receivables from unifeeder, then its back to square one. if they dont, then roce will improve. so the better unifeeder does financially, the better shreyas will do. ofcourse, we need to believe that unifeeder will not do hanky panky in their accounts. its a dp world company, so thats a comfort.

they are likely not to fully settle the long term loans because they need to replace part of their fleet which is coming close to 22-25 years. so they will need debt for that. but they now have decent cash for that.

so in essence, nothing much changes because of the deal from company’s perspective. and hence the related party angle of the transaction becomes important. which is…

in addition to cash, the promoters are getting a minority 17% stake in the acquiring company because they (the promoters) are selling their similar businesses in qatar, saudi, europe etc to unifeeder. and dp world would be comfortable if they continue to manage this business. probably they have therefore given them a stake. most likely the promoters would be involved in running of that business, maybe partially, because they have been saying dp world wants to “drive more synergies”. which means dp would want the top team to be involved. strategy etc could be dp world’s, operations could be managed by shreyas’ promoters. just a guess. it is possible they may not be involved at all, but unlikely.

and unifeeder / dp world becomes the main client of shreyas. thus, the promoters become involved on both sides. in effect, they would be giving business to their own company ie shreyas.

ofcourse unifeeder / dp world are much larger entities. still, there is an element of risk that all transactions may not really be at arms length.

also, one last point, the company (shreyas) wrote down the value of their investment in Avana logistek substantially before selling it to unifeeder. so this raises doubts about their past capital allocation. also, why do this deal at what is probably a near-bottom of the shipping cycle can be questioned. ofcourse the pricing also - why sell this for an amount that equals just the net working capital. surely the knowledge gained over the years of operating this business, the systems/processes/clients/employees would have some value? and lastly, they have not provided for one doubtful debt in last 2 quarter results. if that has to be written off, the q2 profits will turn into loss.

however, like i said above, deal or no deal, nothing much really changes for the company. without dp world also, they can still go ahead and change their business model and become a pure chartering company. with dp world, they are assured of business.

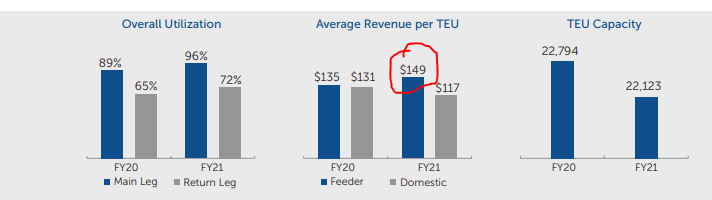

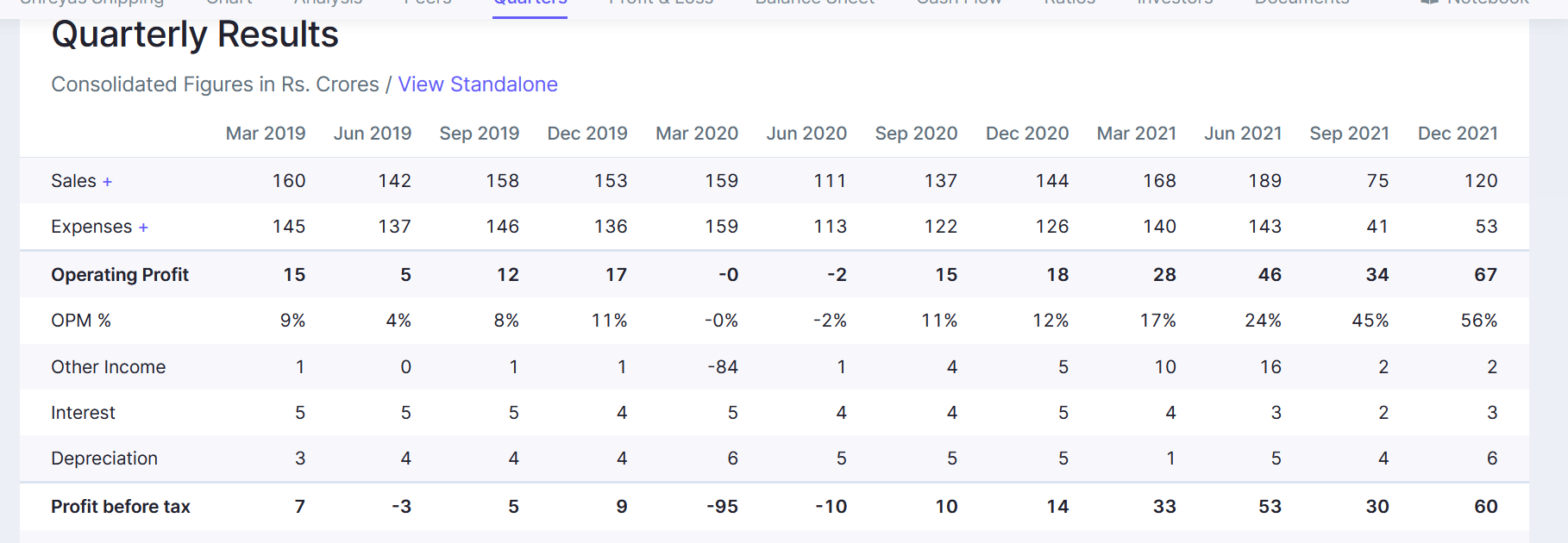

freight rates and container lease rates are consistently increasing as unlocking has been progressing. which is getting reflected in the quarterly results of shreyas and other shipping cos also. my guess is that this is likely to sustain for some time.

i am also attaching the latest credit rating report which lists down some negatives in the business. some of those are becoming positive factors in current times…

discl - have taken an initial position here and will evaluate as and when more details are available about the transaction.