Shree Renuka Sugars (CMP 16 Rs.) is one of the largest sugar producers in the world, the leading manufacturer of sugar in India, and one of the largest sugar refiners in the world

Sugar:

The Company operates eleven mills globally with a total crushing capacity of 20.7 million tonnes per annum (MTPA) or 94,520 tonnes crushed per day (TCD). The Company operates seven sugar mills in India with a total crushing capacity of 7.1 MTPA or 35,000 TCD and two port based sugar refineries with capacity of 1.7 MTPA. The Company also has significant presence in South Brazil, through acquisitions of Renuka Vale do Ivai and Renuka do Brasil. Renuka Vale do Ivai was acquired on 19th March 2010 and is 100% owned by the Company. The Company currently holds 59.4% equity stake in Renuka do Brasil which was acquired on 7th July 2010. The combined crushing capacity of the Brazilian subsidiary companies is 13.6 MTPA. The Company is the only sugar producer globally with year round crushing due to complementary seasons in India and Brazil.

Ethanol:

The Company manufactures fuel grade ethanol that can be blended with petrol. Global distillery capacity is 6,240 KL per day (KLPD) with Indian distillery capacity at 930 KLPD (630 KLPD from molasses to ethanol and 300 KLPD from rectified spirit to ethanol) and Brazil distillery capacity at 5,310 KLPD.

KBK Chem-Engineering (100% subsidiary) facilitates turnkey distillery, ethanol and bio-fuel plant solutions.

Power:

The Company produces power from bagasse (a sugar cane by product) for captive consumption and sale to the state grid in India and Brazil. Total Cogeneration capacity increased to 555MW with exportable surplus of 356 MW. Indian operations produce 242 MW with exportable surplus of 135 MW and Brazilian operations produce 313 MW with exportable surplus of 221 MW.

The Company’s presence in the largest sugar producing country, Brazil and the largest sugar consuming country, India provides access to information on movements in market price and the know-how of the global supply-demand situation. The Company’s operations in Brazil are favoured by low operating cost, high scalability and highly conducive climatic conditions. The Company’s Indian operations are present in sugar rich belt of South and West India, ensuring high sugarcane yields and sugar recovery from cane. The strategically located port-based refineries in Gujarat and West Bengal states of India cover India, South Asia and Middle-East markets competitively.

Promoter:

Narendra Murukumbi’s rags to riches story is inspiring. He is only 46 years old and an IIM graduate. Approx. 10,000 famers became shareholder in company’s IPO which changed the relationship between the farmers and the sugar mill from supplier to that of a shareholder.

Annual results in brief

(Rs crore)

Mar ’ 15 Mar ’ 14 Mar ’ 13 Mar ’ 12 Dec ’ 11

Sales 5,744.20 6,522.40 6,395.40 6,362.10 5,381.80

Operating profit 176.30 140.00 594.80 738.80 542.40

Interest 336.20 318.20 367.10 369.90 272.70

Gross profit -156.00 -123.50 242.70 370.00 270.70

EPS (Rs) -3.18 -6.95 0.77 1.25 1.17

Shree Renuka is an innovative company and there are many things I like about the company:

- Leader in India’s fuel ethanol business with nearly 21% market share. New ethanol tenders are expected to price at Rs. 26

- Largest raw sugar refining capacity in India. Sugar refining capacity helps enhance the company’s asset utilization by processing raw sugar during off-season.

- The company is the second largest exporter of sugar from india with a presence in the Middle East, South East Asia and East Africa. It exports almost 20% of India’s international sugar trade

- The company directly markets sugar to institutional buyers instead of selling to wholesale agents and dealers. The company is a sugar ‘supplier of choice’ amongst companies that produce carbonated soft drinks, fruit juices, choclates, baby foods and dairy products. Its clients include Coca Cola, Pepsi, ITC, Britannia, Nestle and Cadbury, among others. The company sells premium refined sugar.

- Company enjoys certain advantages on account of its West and South Indian location. It has plants in Maharashtra and Karnataka. It enjoys a longer crushing season (over 200 days, starting from October to May), higher recovery (10-20% higher than other regions), proximity to port and lower sugarcane prices due to much lesser state interference in setting sugarcane prices.

- In order to diversify it’s revenue base, the company has acuired a 80% stake in KBK Chem-Engineering Pvt. Ltd. engaged in providing turnkey solutions (EPC contracts) in the field of distilleries, ethanol plants and biofuels.

Conclusion:

With the collapse of global sugar prices, financial performance started deteriorating and put the company to near bankrupt position.

But now it has started turning the corner in line with global prices and many Sops in the offing by Present government including Ethanol blending, export incentives and others.

The Company has witnessed a strong Revenue CAGR of 55% and EBITDA CAGR of 58% from FY2006 to FY2012. The strong financial performance has ensured consistent returns for shareholders with an average Return on Equity of approx. 20% from FY 2006 to FY 2012. The Company’s strong Management team has delivered consistently to ensure growth through successful completion of strategic acquisitions.

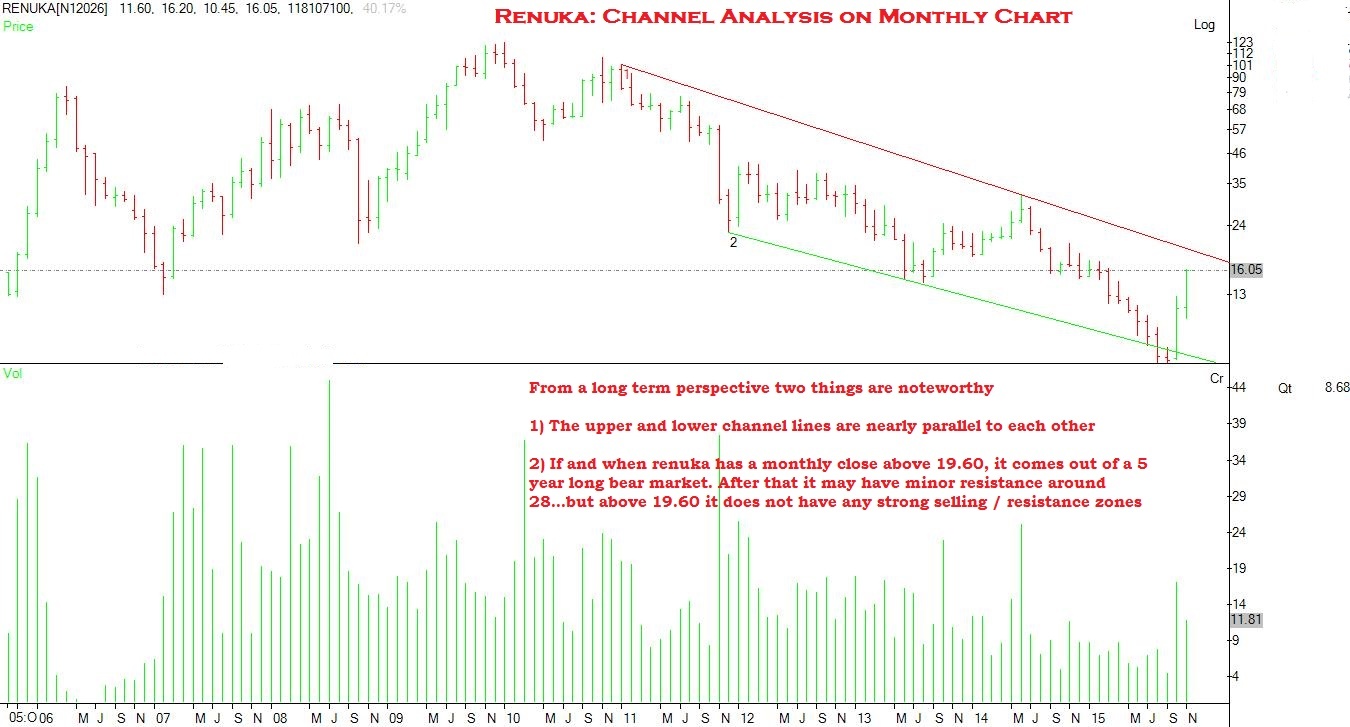

In addition to compnay’s efficient management, underlying reason for such a strong performce is sugar prices at global level almost tripled during this period from 11 c/lb to 35 c/lb. Considering cycle of 3-5 years in sugar sector prices have now bottomed out at 11 c/lb and again started rising above 15 c/lb. Up surge in sugar prices after consecutive surplus year after year has forced in efficient players out of market. And those who have survived will derive benefit in coming time with prices likely to touch upper end of cycle and may surpass 35c/lb in two to three years.

Shree renuka with improved efficiency and synergy is likely to repeat strong CAGR of 55% again for coming 3-to 5 years. Stock prices are likely to increase 8 to 10 times from present level of 16 Rs.

Supporting Hypothesis to conclusion:

Warren Buffet is against cyclical stock for simple reason that average cash flow over a period of time is not so fantastic because of negative return during down turn of cycle. At the same time many renowned players have advocated for cyclical sector because they offer us safe entry during down turn.

I invite all estimated valuePicker colleagues to join me and embark on this wonderful journey of big bull run in Shree Renuka which has just commenced.

Shree Renuka is right now resting on three strong pillars which form strong foundation which creats case for superior returns in medium to long term as under:

(1). Cyclicals: Timing is everything in cyclical sector. If we pick the stock at down turn of cycle and exit at up turn, it offers multi fold returns.

(2). Turn around: When company is turning the corner, it is available at throw away price due to debt laden position of company. History is full of such companies which passes through rough whether and come out with flying colours. With kind of dynamism Mr. Murukumbi has shown in establishing Shree Renuka, it is ripe for big turn around at this stage.

(3). Asset plays: Because of huge assets owned by company stock available at discounted price is as good as by asset at discounted rates when sector is in recession. Sugar sector is offering best opportunity because of consecutive 5 years of surplus in international sugar market.

Above three are criteria out of six categories identified by non other than Peter Lynch. The veteran who has coined the term Multi bagger.

Technical terms Sugar cycle has taken U turn at international level and new new bull run has started with bottom in place. Shree Renuka is only international sugar company from India who has managed to escape controls of states and Indian government to some extent. With rich experience of Wilmar group in trading of agro items lot of synergy has come in to existence.

While management is writing turn around story of Shree renuka, I am pleased to invite you all to share your valuable experience.

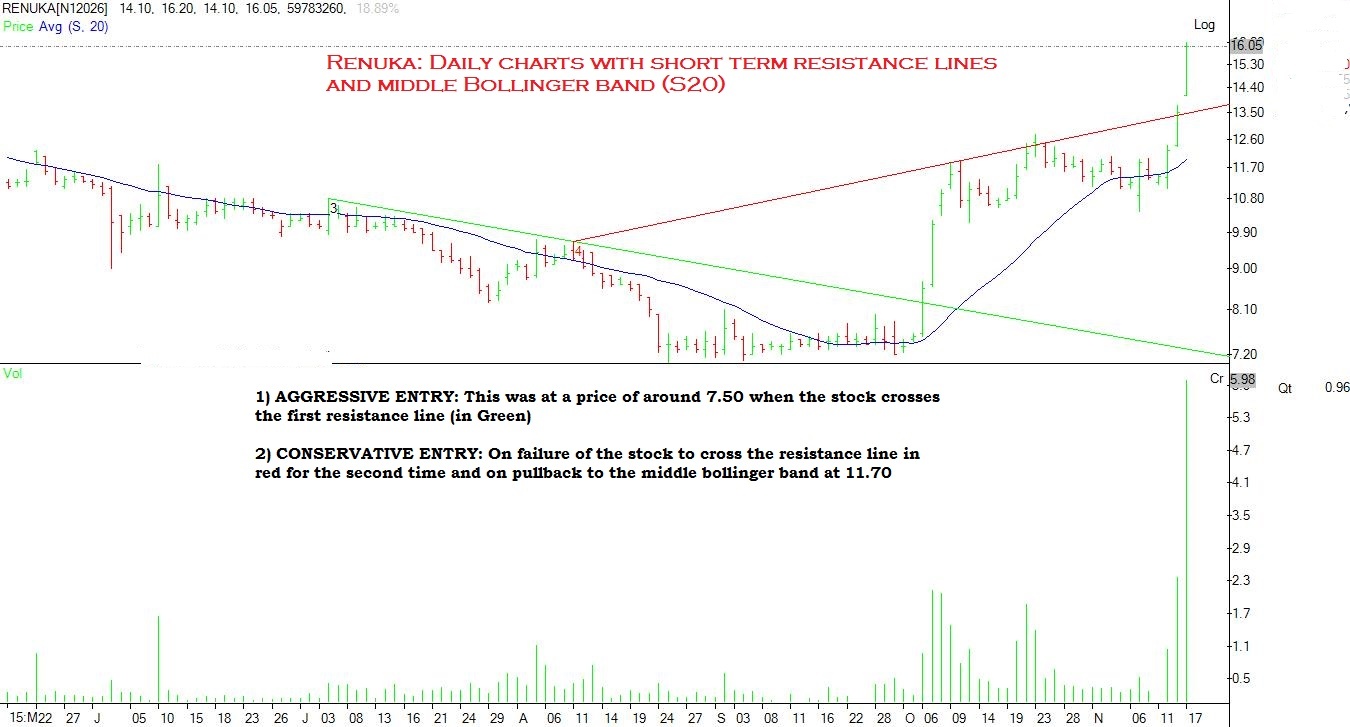

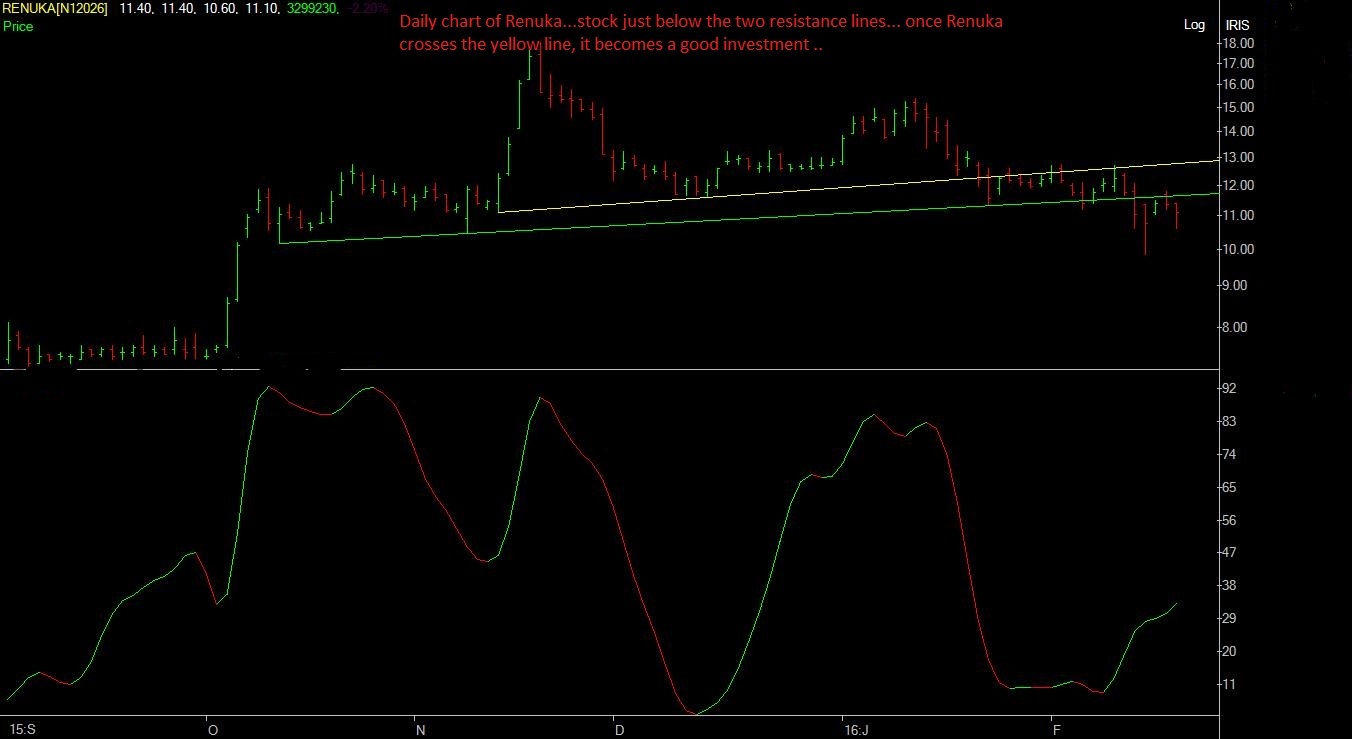

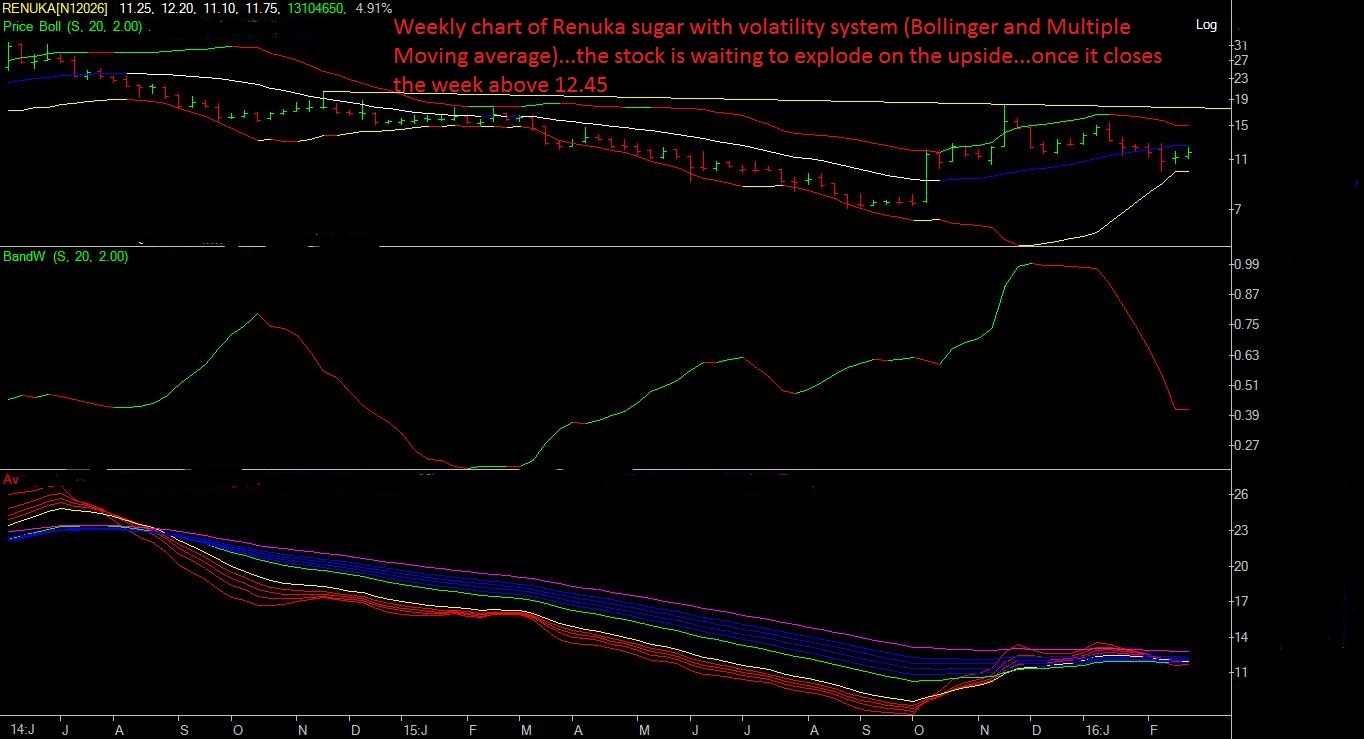

Disclosure: I am holding substantial quantity bought between 7.50 Rs. to 31 Rs.

Sugarbull.